This story originally appeared on Giving Assistant and was produced and distributed in partnership with Stacker Studio.

What to know about buy now, pay later programs

Small-dollar loans have never been as widespread nor as accessible to consumers as they are today—but with the convenience comes risk. With that in mind, Giving Assistant cited news reports and expert information to compile a list of five important things to know about “buy now, pay later” programs.

BNPL services have boomed in popularity since the start of the COVID-19 pandemic. A March 2021 study by The Motley Fool found 56% percent of Americans had used BNPL programs, an 18% increase from when it performed a similar study in July 2020. The adoption of these programs was most dramatic among college-aged individuals and seniors. The largest portion of those who used BNPL services said they did so to purchase something outside of their budget, and about half used BNPL to purchase electronics.

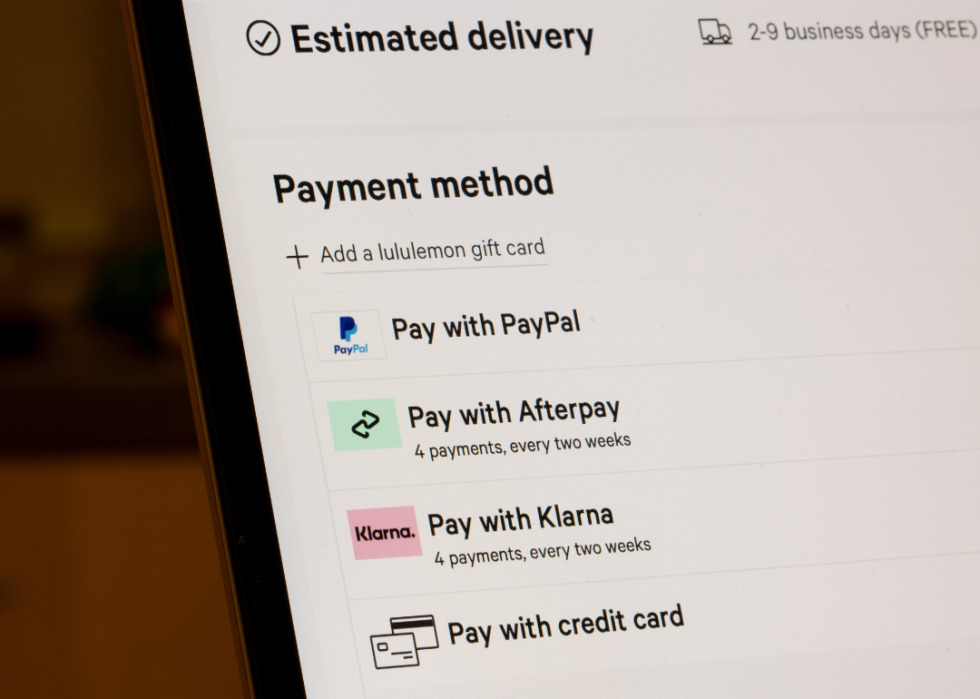

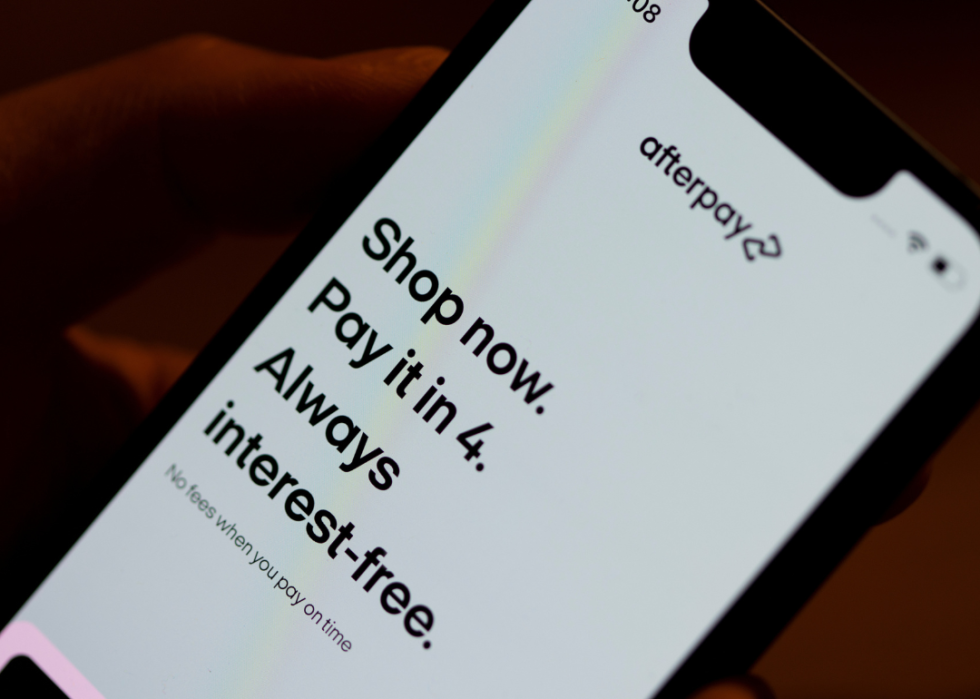

Also known as “flexible payments” or “point-of-sale loans,” the most popular buy now, pay later platforms allow the consumer to pay for a product over a term of six months or a year—and sometimes even longer, depending on the size of the purchase. At their root, these services quench our thirst for instant gratification, giving consumers the product they want now, financed in monthly, interest-free installments they can pay later. But this emerging field of consumer lending doesn’t come without its pitfalls.

Thirty-one percent of BNPL users said they have made a late payment or incurred a late fee, and 36% of respondents said they are at least somewhat likely to make a late payment within the next year, according to research from The Motley Fool. Klarna, Afterpay, Affirm, PayPal, and Zip are among the companies dominating the BNPL space. Apple, the newest entrant, also plans to fund loans extended to customers by itself rather than rely on a bank.

Keep reading for five essential things you should know about BNPL programs.

BNPL replaced a very similar system: layaway

Why let that brand-new Instant Pot continue to sit on your wishlist when you could take it home today, cook dinner with it tonight, and pay for it in smaller installments over the next three months?

That’s been the psychology driving hordes of retailers to drop their layaway programs in recent years in favor of BNPL options. At the end of 2021, Walmart ditched its layaway option and partnered with Affirm, allowing customers to purchase their items over three, six, or 12 months.

Today, millions of retailers have followed suit in accepting BNPL—Amazon, Target, GameStop, Peloton, and Macy’s, among them. You can even finance a burrito from Chipotle.

They don’t affect your credit score… yet

Since their inception, the major credit bureaus have largely ignored BNPL programs. This means financing your purchases with a service like Afterpay and missing payments hasn’t hurt your credit score. Conversely, making timely payments hasn’t helped, either.

But that’s likely changing soon. Experian, TransUnion, and Equifax intend to begin contributing BNPL data to credit reports.

Due to how many younger people use the loans, the move to include BNPL data in determining credit scores could be “the biggest financial inclusion opportunity in at least a generation,” said Liz Pagel, senior vice president of TransUnion’s consumer lending division.

Popular among millennials and Gen Z

Above all else, BNPL adoption in recent years has piqued the financial world’s interest most because younger Americans are using it more than other forms of credit, like credit cards.

Credit bureau TransUnion found that one-third of BNPL users were between the ages of 18 and 30. That stands in stark contrast to credit card usage among the same group, which make up about 17% of credit users, according to the bureau.

Rather than having a set credit limit like credit cards, BNPL users are technically approved for individual loans with each transaction they finance. The loans are largely frictionless. They can be initiated with a few taps on your smartphone or clicks of a mouse. The big companies offering BNPL loans have debuted browser plug-ins and mobile apps that integrate the financing into your devices. Apple’s integration will take things a step even further—offering BNPL financing for any purchase made with Apple Pay.

It’s a largely unregulated industry

BNPL services are becoming controversial as adoption spikes among retailers and more consumers take out these microloans.

Nearly all the leading BNPL platforms have poor customer reviews through the Better Business Bureau. Most complaints deal with poor refund processes and hard-to-reach customer service departments.

Critics of BNPL as a service argue that most consumers use the loans to finance purchases they should be paying in cash. They also argue that the fees these platforms charge retailers drive up the cost of goods and services. Having multiple payment schedules across many purchases can also overcomplicate budgeting.

The Consumer Financial Protection Bureau announced an investigation into the largest BNPL companies at the end of 2021. It’s concerned with the levels of debt consumers may be taking on. At least one BNPL company, Klarna, has said in public statement that it welcomes “proportionate” regulation.

They make money from the retailer—and from late fees

BNPL platforms make money through fees paid by their retail partners, which is how they offer consumers loans with no interest.

Retailers pony up fees to integrate with the BNPL platforms assuming that it will incentivize more spending at their stores. Those fees are usually between 2% to 8% per transaction, according to the Los Angeles Times.

And while BNPL providers don’t charge interest, they do charge late fees, which accrue when a consumer misses a scheduled payment. Afterpay, for example, charges a late fee equal to the lesser of either $8 or 25% of the purchase price.

Affirm, on the other hand, doesn’t charge late fees but discloses that making late payments can hurt your chances of getting another loan through the company and can even potentially affect your credit score, according to CNBC. That means shoppers could end up paying higher interest rates on other financing decisions down the line.