Average student loan debt increased in first half of 2024 in Florida

Average student loan debt increased in first half of 2024 in Florida

Despite repayments on federal student loans resuming late last year, much is still up in the air with student loan debt. Some loans have been forgiven, and more than a few borrowers have received incomplete, contradictory or confusing information about their loans.

Experian compiled data on student loan debt in Florida, as well as the nation at-large, to see how residents of the state are faring. Student loan balance data is Experian data unless otherwise noted.

Most generations in the U.S. are still managing student loan balances averaging more than $40,000. Generation X, the eldest of whom turn 60 next year, owe the most on their student loans, on average.

There's wider variance among the states for student loan balances than for other types of consumer debt, including auto loans and credit card debt. In most states, average student loan balances range from $25,000 to $45,000. One obvious outlier is Washington, D.C., where the average student loan balance topping $57,000 is notable.

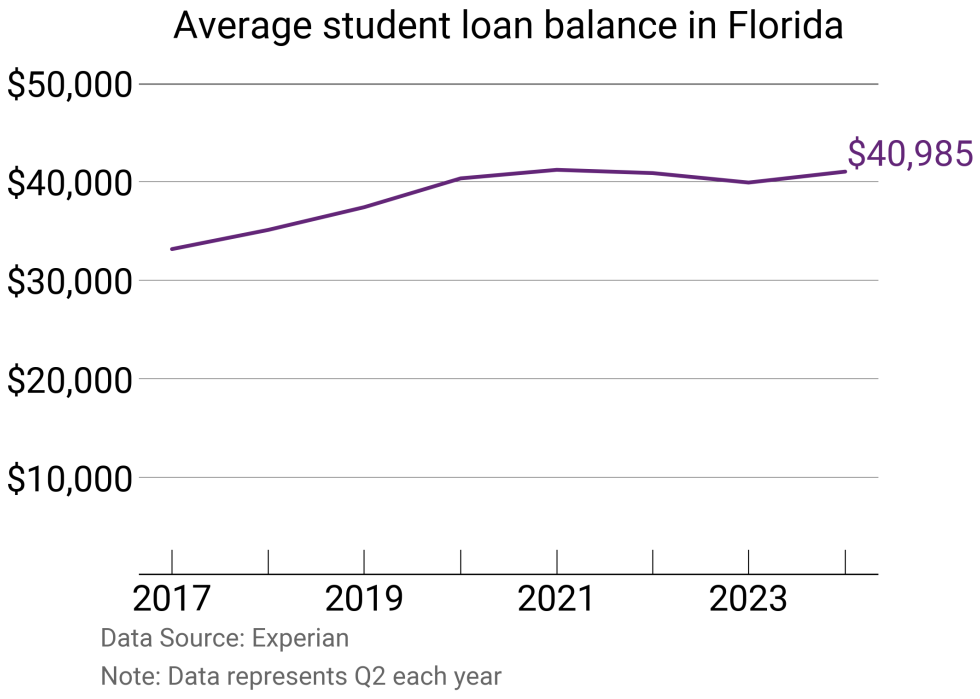

Average student loan balance in Florida

In the first half of 2024 the average student loan balance in Florida grew $3,111 from the end of 2023, reaching $40,985. Florida has the 9th highest average loan balance among all states and $2,102 higher than the national average of $38,883.

States with the highest average student loan balance

#1. Washington, D.C.: $57,927

#2. Maryland: $45,434

#3. Georgia: $43,005

#4. New York: $42,058

#5. California: $41,991

States with the lowest average student loan balance

#1. North Dakota: $31,040

#2. Iowa: $31,829

#3. South Dakota: $32,112

#4. Wyoming: $32,232

#5. Nebraska: $33,506

Student Loan Forgiveness Plans Span More Than 4 Million Borrowers, Saving Them $160 Billion

According to the Department of Education, nearly $160 billion of student loan relief has been provided to student loan borrowers. This is largely from cancellations of federal student loans, but is also based on re-implementations of income-driven repayment plans. The largest slice of relief—forgiving $62.8 billion in loans to those deemed eligible though their public service—has amounted to an average of $71,000 of loan forgiveness for those borrowers.

But there are also other ways that federal-led student loan relief plans have chipped away at student loans, including providing $14 billion in forgiveness to more than a half-million borrowers with permanent disability, and canceling $29 billion of loans for 1.6 million borrowers through court settlements.

In most cases, borrowers had been paying their loans for years prior to the cancellations of the remaining balances by the federal government.

For Current Students, College Costs Level Off, but Are Still an Increasing Burden

Considering that nearly everything else costs more than a few years ago, it may be a surprise that college tuition costs have actually leveled off in the past few years, barely budging since 2020. Adjusted for inflation, one general measure of college costs have begun to decline, according to data from The College Board. There's still a huge sticker price for higher education though.

However, in part due to everything else surrounding tuition increasing in price—like room and board as well as borrowing costs for student loans—it may not seem much of a bargain. (For their part, colleges and universities are managing financial issues of their own, in no small part stemming from demographic shifts leading to declining enrollments.)

Larger Financial Hurdles for Student Loan Borrowers

Despite income-based repayment plans becoming more commonplace among borrowers, many still face greater financial challenges than those without monthly student loan payments.

In general, those with student loan balances carry greater financial burdens elsewhere. While auto loan balances are similar for both consumers, those with student loan balances have much larger average credit card balances than those who don't have student loan debt. They also have larger monthly payments to service all their debts versus those without student loan bills.

Those Still in College Will Be Subject to Higher Rates on Student Loans

The high cost of borrowing has now reached students. It wasn't unexpected: Interest rates for federal student loans (direct loans) have long been based on the auction prices for long-term government notes sold by the U.S. Treasury in May of each year. This year, as yields of those 10-year notes were at 15-year highs, so, too, will federal student loan costs be for the 2024-25 academic year.

Beginning July 1, undergraduate students with direct loans are borrowing at a 6.53% rate.

Those undergraduates won't need to start repaying loans immediately, but when they do eventually leave academia, they'll likely be paying much more in interest (versus principal) than others who have federal loans with interest rates of less than 5%.