3 ways to plan for a satisfying and successful retirement

3 ways to plan for a satisfying and successful retirement

Retirement planning today means more than simply leaving your full-time job. It means achieving the financial freedom to pursue your passions and purpose—whether part-time work, teaching, consulting, volunteering, etc. How will you spend your time when your career comes to a close?

It's essential to take the time to consider exactly what you want from your retirement. What does it look like for you? Do you want a more "traditional" retirement, or do you have other plans in mind? Beyond that, how do you expect to see those plans through?

Wealth Enhancement Group has three tips for successfully reimagining your retirement.

1. Time your retirement transition

For years, retirement has been about simply reaching an age. You work until you turn 65, and then you retire. This antiquated mentality can put you into retirement before or after you're ready. Instead of adhering to old traditions, start by thinking about when you'd like to transition into retirement.

Maybe you like your job or your line of work and are quick to quit. If so, try to "go AWOL" instead. Regarding retirement, AWOL stands for "Achieving a Work-Optional Lifestyle." By "going AWOL," you can take the reins and determine how and when you transition away from working. Retirement nowadays means different things to different people, so having the ability to continue working if you want, with the flexibility to finish and fully retire when you're ready, can help you make the retirement transition at an optimal time.

How to retire on your terms

Timing your retirement transition will put you on track to having a happy retirement. Here, we've highlighted three key principles to focus on as you consider how to retire on your terms:

- Aim for Voluntary Retirement: Being encouraged to retire before you're ready can lower your satisfaction. Adequate retirement planning means defining when you want to finish working, even if that's later than others expect you to.

- Don't Focus on a Number: If you adopt the idea that you need a specific dollar amount in your retirement accounts to be able to retire, you may end up doing so much later than you actually could. By defining your goals for retirement, you can avoid the pitfall of staying at your job for too long and instead spend time doing what brings you joy.

- Lower Your Stress with Accurate Risk Balances: It can be tempting to check your retirement accounts often to see if you're "on track," which can lead to unnecessary stress in times of market volatility. By structuring your portfolio to reflect your risk tolerance and your time horizon, you can rest easy knowing that your investments are working as best as they can.

Learn the fundamentals of Social Security

Social Security will no doubt play a huge part in your retirement plans. It's a major milestone in your retirement, so make sure you plan for when you want to start receiving this benefit and how it will be used as part of your retirement income strategy.

Remember: Timing is everything when it comes to Social Security. You can start taking your benefit any time between the ages of 62 and 70, but how old you are when you start drawing Social Security will permanently affect how much you receive. It's not a decision that should be taken lightly, so plan thoughtfully.

2. Plan your tax strategy

We all know the old adage: "Nothing is certain except death and taxes." When you're working and earning, your tax burden might not be top of mind. But when you're retired, your tax liability can suddenly significantly affect your overall finances. That's why it's so important to plan your tax strategy while you're planning for retirement.

The true purpose of a solid tax strategy isn't simply to minimize your tax burden every year—it's to maximize your long-term wealth. While this certainly can include reducing your taxes, it's more about paying taxes thoughtfully, allowing you to unlock benefits in the long run. One of the primary ways to set yourself up for tax success is through tax diversification.

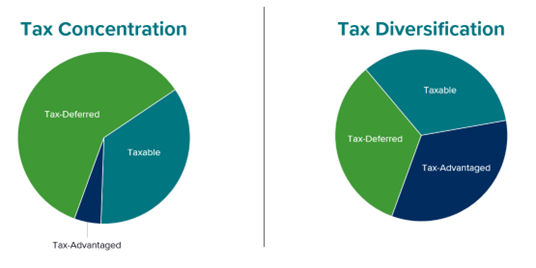

Tax diversification for retirement

You've heard of investment diversification, where you try to minimize investment risk by spreading your investments through various vehicles. Well, tax diversification works in much the same way.

Different accounts are taxed differently, so spreading your assets across accounts with other tax treatments can significantly impact your retirement taxes. The three different tax treatments are:

- Taxable Accounts: The earnings and realized gains from these accounts are fully taxable at year-end. However, they are liquid and convenient, giving you access to your money when you need it with fewer distribution restrictions. These are your bank accounts or brokerage accounts.

- Tax-Deferred Accounts: With these accounts, you don't pay taxes on the contributions, earnings grow tax-deferred, and taxes are only paid once distributions begin. Because they put off your tax burden until you take distributions, these are popular retirement accounts like 401(k)s, 403(b)s, and IRAs.

- Tax-Advantaged Accounts: With tax-advantaged accounts, you pay taxes on the contributions, but then they grow tax-free, and no tax is due when you start taking distributions—as long as certain conditions are met. This makes them powerful tools come retirement time. These are your Roth accounts like Roth IRAs or Roth 401(k)s.

While taxes are inevitable, they certainly don't have to stop you from enjoying your retirement and doing what you love. By planning out your tax strategy before retirement, you can maximize your long-term wealth and rest easy knowing you can access and enjoy your money when you want it.

3. Invest in your health like it's your wealth

Having enough money to sustain your lifestyle is a foundational aspect of retirement. Still, by narrowly defining wealth as "money," we miss out on a critical part of living a fulfilled life. Increasingly, we are finding that retirees who emphasize health in their retirement lead happier, longer lives, benefiting from this alternative form of "wealth."

Physical activity is a great way to stay healthy and in shape. Low-impact sports like pickleball are rising in popularity, and for those who don't care for sports but still want to stay active, going out for regular walks or swims are great ways to age gracefully.

Additionally, finding purpose in retirement can be a great way to stay sharp mentally. During your working life, it's entirely possible you found purpose in your work. However, once you make the retirement transition, that source of purpose goes away. The new challenge is to find something to do to get you up in the morning, stay engaged, and keep you moving. That purpose could be spending time with your family, volunteering in your community, or any other motive that defines you for the next period of your life.

Planning for long-term care

While eating healthy and staying active are two primary ways to maintain your health into retirement, the reality—and costs—of long-term care (LTC) looms on the horizon for many retirees during their financial planning process. The costs associated with long-term care are already high, and they're only increasing.

Thinking about the dollars and cents of LTC is an important place to start, but planning for LTC is about more than just having enough money to pay for it. You need to know what will happen and/or what you'll do if your health declines and you can no longer perform daily tasks on your own. It's a good idea to do this while you're still healthy because it might be too late if you wait until something happens.

This story was produced by Wealth Enhancement Group and reviewed and distributed by Stacker Media.