Average personal savings of Americans

This story was produced by MoneyGeek and reviewed and distributed by Stacker Media.

Average personal savings of Americans

The average savings account balance in the United States was $62,410 in 2022, while the median balance was only $8,000. The average and median balances vary depending on age, with older generations having more savings. Individuals under 35 had an average savings of $20,535 and a median balance of $5,400. Those 55 and older save an average of $85,200, with median balances of at least $8,000.

Keep in mind that the average can be heavily skewed by a small percentage of households with large balances. Median, on the other hand, provides a more realistic representation of household savings.

These figures are based on the Federal Reserve's 2022 Survey of Consumer Finances (SCF), the most recent data available. The report, released every three years, tracks the status of U.S. transaction accounts (bank accounts). MoneyGeek explores this savings data by income level, demographic, educational attainment and more.

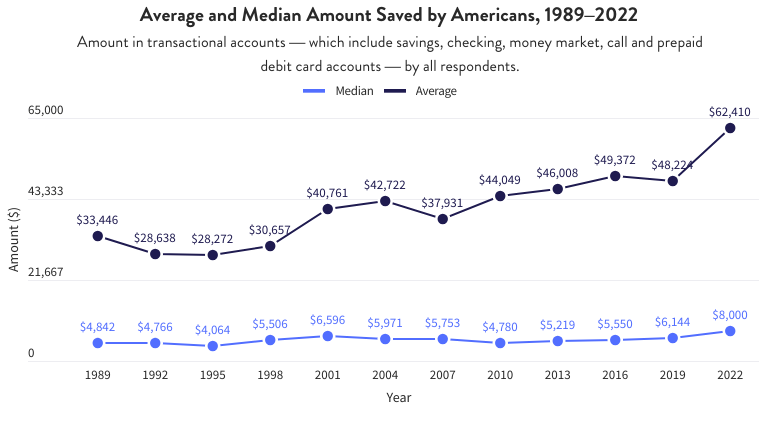

Average American savings over time

The average American household had transaction accounts worth $41,600 in 2022, while the median balance was $8,000 — both 30% higher than their respective 2019 figures.

The average U.S. savings account balance has changed over time. The latest value is significantly higher than the average recorded in 1989. Meanwhile, the median amount Americans kept in transaction accounts has been consistently rising since 2010. Overall, the 2022 figure was the highest recorded median since 1989.

These figures reflect a disparity in terms of savings. Despite the high average, the median remained in the four digits. This suggests that more Americans only have four-digit amounts in their savings accounts.

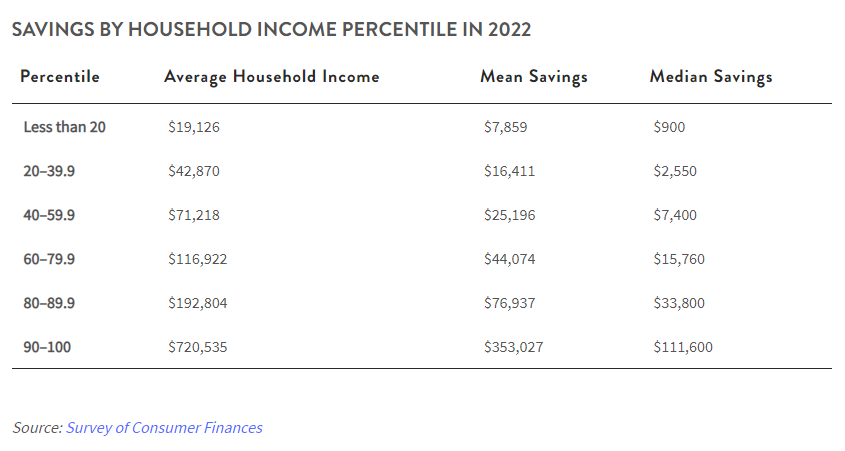

Savings by Household Income

Household income has a significant impact on savings. Higher income levels typically increase savings based on the average and median balances. People living on lower incomes generally have further to go in building a substantial savings account.

The table below shows a direct correlation between household income and savings. For instance, the median savings of those earning an average of $19,126 in 2022 was only $900. Meanwhile, those earning an average of $720,534 had a median savings of $111,600, over 120 times higher.

Despite changes in values, the trend has been consistent throughout the years. The highest-earning households, or those in the upper 10%, have always had the most savings.

On the other hand, the personal savings rate has been declining since 2021. After a peak in 2020, it decreased in 2021 and 2022 as the country faced high inflation. Into 2024, personal savings have yet to return to levels observed before the pandemic.

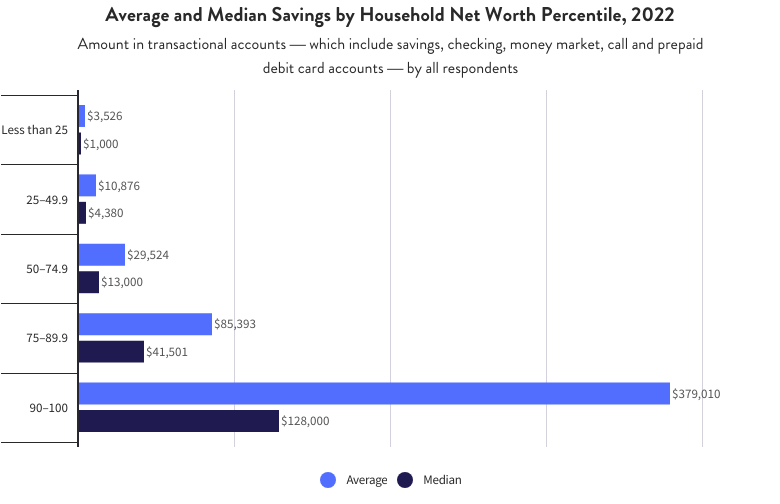

Savings by Net Worth

Households with higher net worth also tend to have more savings. Data showed that the average and median transaction account balances increased along with net worth. Net worth indicates the total value of a person's finances. It's calculated by subtracting liabilities (what you owe) from all assets (what you own). The rise in household income helps increase net worth. The same can be said when it comes to savings.

Based on the latest data, families with higher net worth accumulated higher savings. Those who fell under the 90-100 percentile had a median balance of $128,000 and an average of $379,010 in savings. Meanwhile, households in the under 25 percentile category only had a median savings of $1,000 and an average balance of $3,526.

From 1989 to 2022, American households with lower net worth percentiles typically had fewer savings than those with higher net worth percentiles.

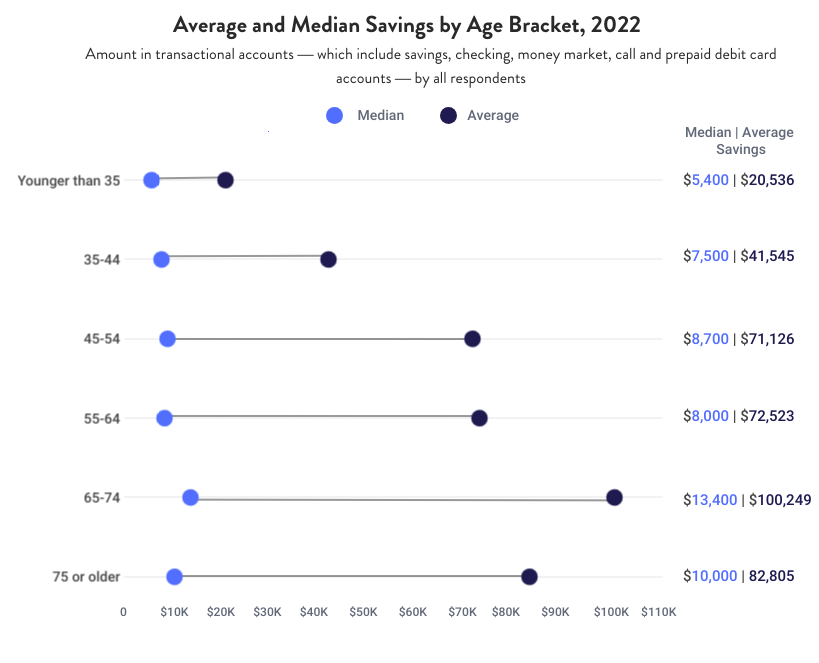

Average American savings by age

Generally, households with older individuals have higher savings account balances than younger families. In 2022, individuals aged 65 to 74 had the highest average savings at $100,249, while individuals younger than 35 had the lowest at $20,536.

Survey data supports the idea that older generations are likely to have higher account balances, with a few exceptions. Households with 45- to 54-year-olds had higher median savings than those with 55- to 64-year-olds. For average savings, individuals aged 65 to 74 saved more than those 75 years old and older.

With more professional experience, older individuals generally earn more and save more. Having more time to build their finances puts older individuals in a more secure position to save. Younger individuals, however, may still be burdened with expenses like student loan debt.

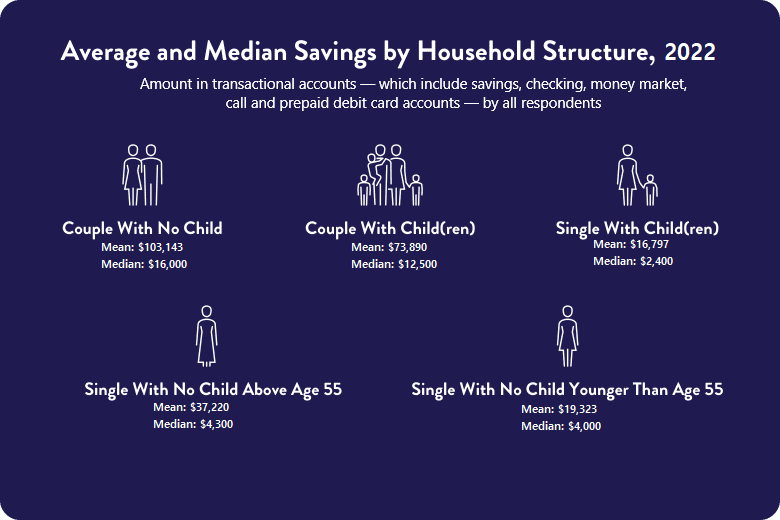

Savings by household structure

Family structure changes household savings. Couples with no children have the highest average savings at $103,143, while single parents with children have the lowest average savings at $16,797. Generally, single-parent households save less than couples. With two people sharing financial responsibilities, couples typically have more income and support to save.

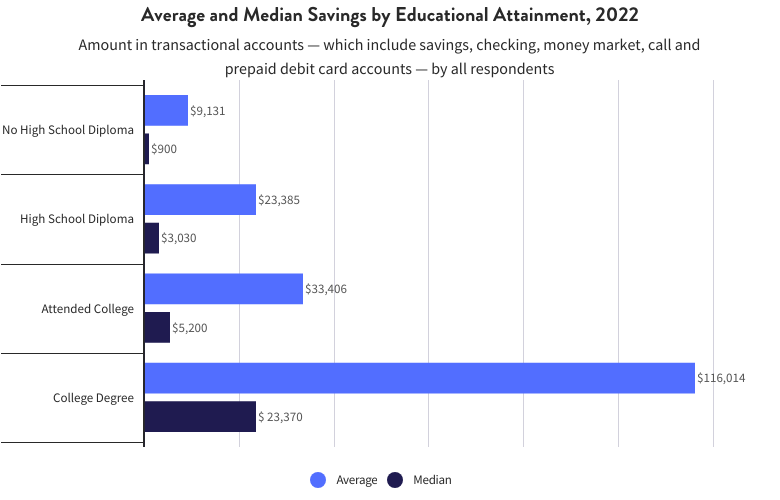

Savings by Educational Attainment

Educational attainment can influence a person's livelihood, including their skillset, opportunities and earnings. For instance, according to the U.S. Bureau of Labor Statistics, the median weekly earnings of individuals with a Bachelor's degree is $1,493; those with less than a high school diploma have a median weekly income of $708.

Differences in savings are also observed between varying levels of education. Based on household averages, a household with at least one individual who holds a Bachelor's degree has $116,014 in transactional accounts. The average family with no high school diploma has only $9,131 in savings. Median saving is also significantly higher for households with college graduates ($23,370) than those with no high school diploma ($900).

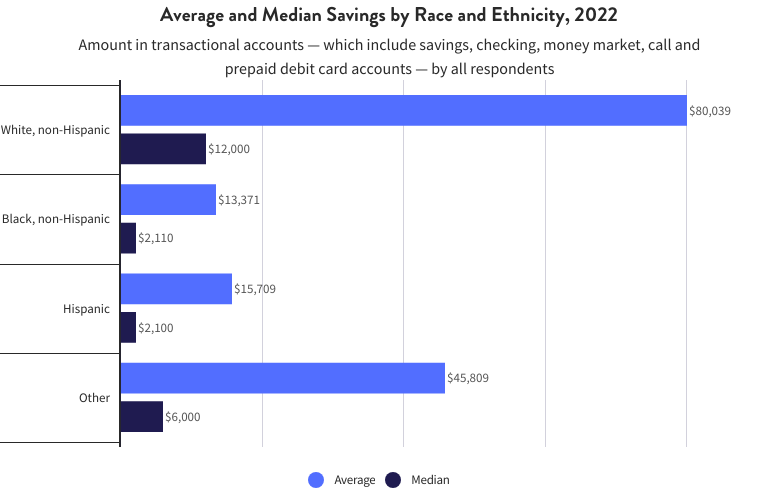

Savings by Race and Ethnicity

Across race and ethnicity, non-Hispanic white Americans generally have the most savings, holding an average of $80,039. In comparison, non-Hispanic Black Americans and Hispanics have average savings of $13,370 and $15,709, respectively. Regarding median figures, non-Hispanic white Americans also have the highest median savings ($12,000). Hispanic Americans have the lowest median ($2,100).

Several factors can influence the difference in savings from household to household — primarily income and wealth. According to the Federal Reserve Bank of St. Louis, on average, white families possess approximately $958,000 more wealth than Black families and about $1,011,000 more than Hispanic families.

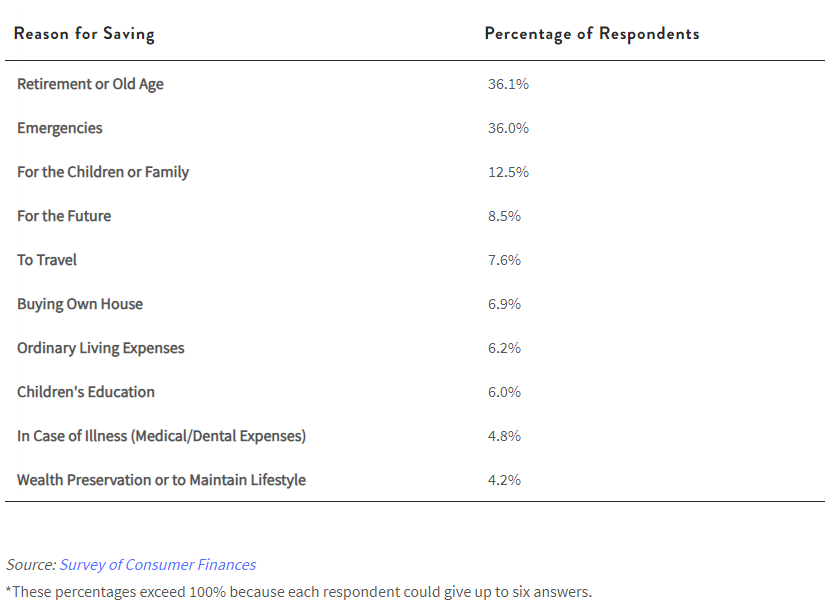

Top Reasons for Saving

There are many advantages to saving money. For many Americans, it's a way to ensure a financial safety net during emergencies. Others save to prepare for retirement. Ultimately, it depends on your priorities and needs.

Here are the top 10 reasons why Americans are saving money, as reported in the Federal Reserve's survey.

Average Savings of Americans FAQ

MoneyGeek answers the most commonly asked questions about savings accounts to help you better understand the different factors affecting the average savings account balances in the U.S.

What is the average savings account balance in the U.S.?

On average, U.S. households saved $62,410 in 2022. The median balance, on the other hand, was $8,000. This means that despite the high average, most families had four-digit savings (rather than five).

How do income and net worth affect savings?

Generally, people with higher incomes and net worth have more savings. Households that belong to the 90–100 percentile net worth and those earning an average of $720,534 have the highest savings.

What generation saves the most amount?

Older adults tend to have higher savings than younger generations. Based on average balances, individuals aged 65 to 74 had the highest average savings in 2022. Those who were younger than 35 had the lowest average balance.

How does having kids or a life partner impact savings?

The Federal Reserve's survey results show that couples with no children had the highest median savings account balance, while single-parent households with children recorded the lowest median. The added financial responsibility of having children can affect an individual's ability to save.

What are the top reasons why Americans save money?

There are various reasons why Americans save money. Two of the most common reasons are retirement and emergencies.

Related Content

Managing your finances can be challenging, especially as you juggle your responsibilities. Below are some online resources you can explore to become more financially prepared for the future.

- Best Budgeting Tools and Savings Apps: Check out the different tools and resources to help you budget your money and save more. This guide also lists some of the best budgeting tools and apps.

- Financial Literacy Handbook: Expand your knowledge about your finances. Learn about different financial concepts and terms.

- Guide to Budgeting: Start your journey to smart money management.

- Saving for Retirement: Find out how you can start preparing for retirement.

- Ways to Reduce Monthly Spending: Get tips on how to reduce your spending and grow your savings.