Is 'buy now, pay later' replacing store credit cards in shoppers' wallets?

Is 'buy now, pay later' replacing store credit cards in shoppers' wallets?

U.S. consumers were carrying more than $125 billion in store credit card balances as of June 2023, according to Experian data. About half of consumers in the U.S. (49%) have at least one store card in their wallet, and most of those (63%) carry a balance on their store card(s) from month to month.

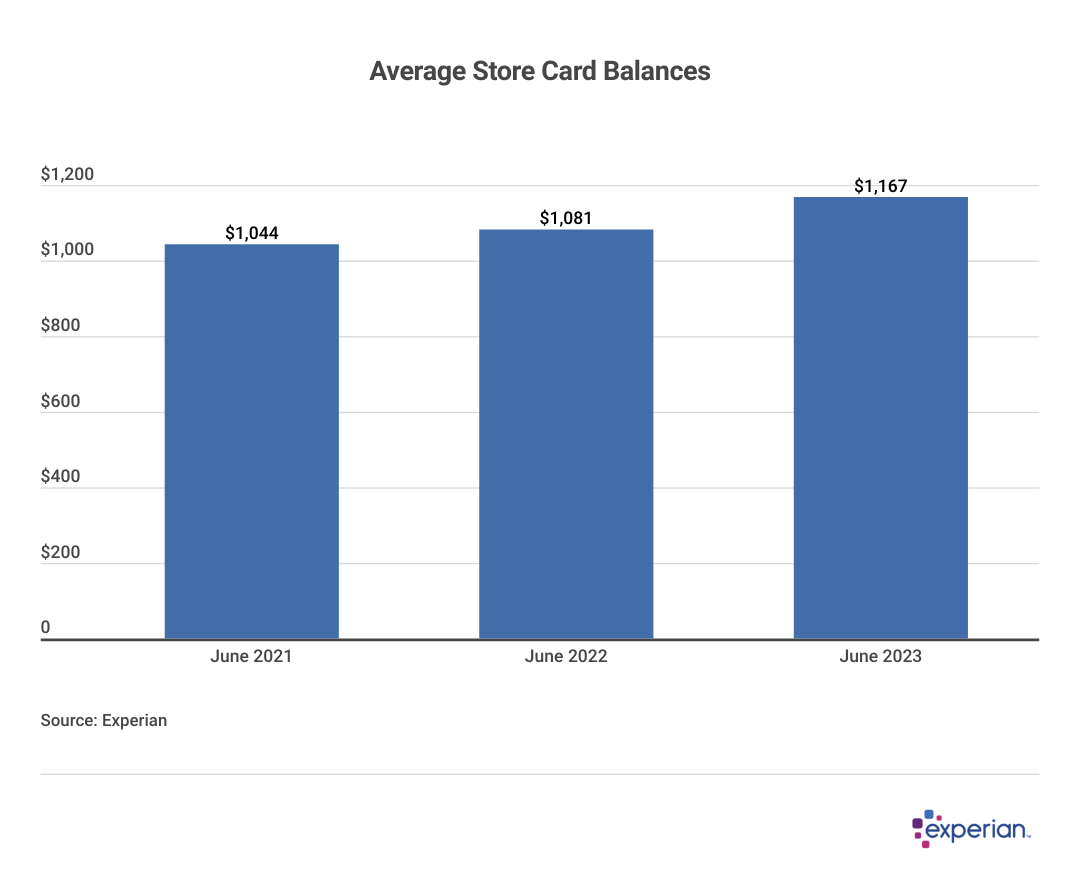

The average balance among all store cardholders with a non-zero balance is $1,167 as of June 2023. Even if only half of those balances are accruing interest, it still burns a hole worth at least $15 billion in those consumers' pockets annually.

As store cards are one of the most expensive ways consumers carry revolving credit, and with APRs increasing across the board, are there better ways to make those retail purchases? For a growing number of consumers, "buy now, pay later" financing presents an appealing alternative. In this analysis, Experian looks at how consumers' use of retail credit cards has changed as well as the rising tide of buy now, pay later balances.

Retail cards for mid-range purchases

Store credit cards can be the most expensive credit cards in a consumer's wallet. And although not all of that balance is necessarily subject to interest charges, retail cards sport some of the highest annual percentage rates on the market. Many have APRs of 27.99%—nearly 6 percentage points higher than the average credit card interest rate, according to Federal Reserve data.

Consumers often sign up for these store cards at the checkout counter to take advantage of interest-free financing promotions. Depending on the item being purchased, the store may offer you 0% financing for six, 12, or 18 months to pay off the refrigerator or power washer you buy. However, if you miss a payment or have a balance remaining after the 0% financing period expires, you could retroactively owe interest from the original date of purchase.

Is buy now, pay later replacing the store card for purchases?

Buy now, pay later plans offer similar—though not exact—terms as 0% financing offers made by large retailers through their store credit cards. These financing plans are often available for instant approval at the point of sale (the buy now part), and consumers are typically asked to pay later in four or fewer installments within three months.

Terms and conditions around the products purchased using buy now, pay later plans aren't parallel to purchases made with store or credit cards—something that needs to be considered if you need to return or exchange a purchase.

Nonetheless, the types of purchases consumers make with buy now, pay later plans are similar to those offered by retail cards for big box stores for purchasing their appliances and other durable goods. Most purchases made with buy now, pay later range in cost from $100 to $500, according to Experian data.

So-called "closed loop" store credit cards—those meant to be used exclusively within the confines of traditional department stores and home improvement stores—are now competing most directly with buy now, pay later, even at these stores' checkout registers. (For those playing at home, Amazon also has an Amazon-only store card for purchases on their site.) And for their part, retailers are embracing the new way for consumers to make purchases, even though their name isn't on buy now, pay later plans like they are on branded credit cards.

Buy now, pay later and credit scores

Buy now, pay later financing is increasingly popular, and forecasts suggest the amount consumers spend using buy now, pay later will triple in size over the next two to three years. Although not a perfect substitution for store card spending, buy now, pay later plans are likely to supplant some store card spending more than traditional bank-issued credit cards.

And buy now, pay later plans aren't only used by those without credit cards: Some consumers prefer that mid-sized purchases be front-of-mind and paid down, even though they have plenty of credit available on either a store card or credit card.

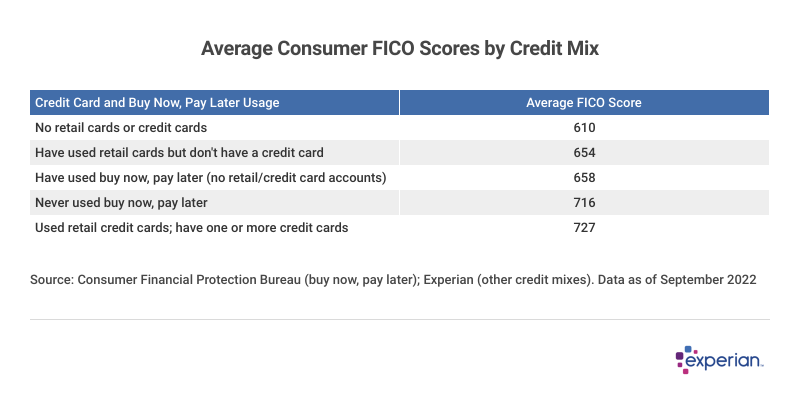

Buy now, pay later plans usually don't rely on traditional credit scores to determine a consumer's creditworthiness; they rely on what's broadly referred to as alternative data. That said, most buy now, pay later consumers have a credit score, one that's similar to those with retail store cards.

As far as which type of spending that growth will supplant, the most obvious choice seems to be revolving store card users, at least based upon similarity of FICO scores.

Those consumers using retail cards, and paying interest on those transactions, will quite possibly also qualify for a buy now, pay later plan for larger purchases that they may be otherwise reluctant to add to a revolving balance.

But consumers thinking about larger transactions, even though they already have credit cards with sufficient available credit, may also prefer buy now, pay later plans for similar reasons. They may not want to increase their credit utilization, which could reduce their FICO scores. Nor do they necessarily want to pay additional interest if an interest-free solution is possible for a big-ticket item.

Consumer psychology in action

But finally, much of the behavior surrounding a consumer's preference for buy now, pay later may have more to do with psychology than accounting. Many consumers seem to prefer paying off one buy now, pay later purchase at a time instead of managing balances on a store card or credit card.

A recent industry survey by PYMNTS found that users—by a wide margin—consider buy now, pay later more of a budgeting tool than a type of credit. Many common repayment terms for some buy now, pay later plans are biweekly, which coincides with many consumers' paycheck frequency. So, for many, buy now, pay later is thought of more as a cash flow management tool, as opposed to simply another way to leverage credit to make purchases.

Methodology: The analysis results provided are based on an Experian-created statistically relevant aggregate sampling of our consumer credit database that may include use of the FICO Score 8 version. Different sampling parameters may generate different findings compared with other similar analysis. Analyzed credit data did not contain personal identification information. Metro areas group counties and cities into specific geographic areas for population censuses and compilations of related statistical data.

This story was produced by Experian and reviewed and distributed by Stacker Media.