This story was produced by Experian and reviewed and distributed by Stacker Media.

State of retail cards and buy now, pay later in 2024

Much was noteworthy about higher interest rates for everything consumers financed in 2023. But one figure that got less notice was the interest rates of store credit cards, a type of credit card that remains a department store staple.

In 2023, typical interest rates on some retail credit cards climbed above 30%—rates previously reserved for delinquent cardholders and those with poor credit. These store card rate hikes don't appear temporary, either, regardless of monetary policy decisions the Federal Reserve makes in the coming months.

In this analysis, Experian looks at both retail cards and their new counterpart: buy now, pay later. In many cases, these payment methods serve similar markets and provide an alternative to traditional credit card debt that looms large on the minds of today's consumers.

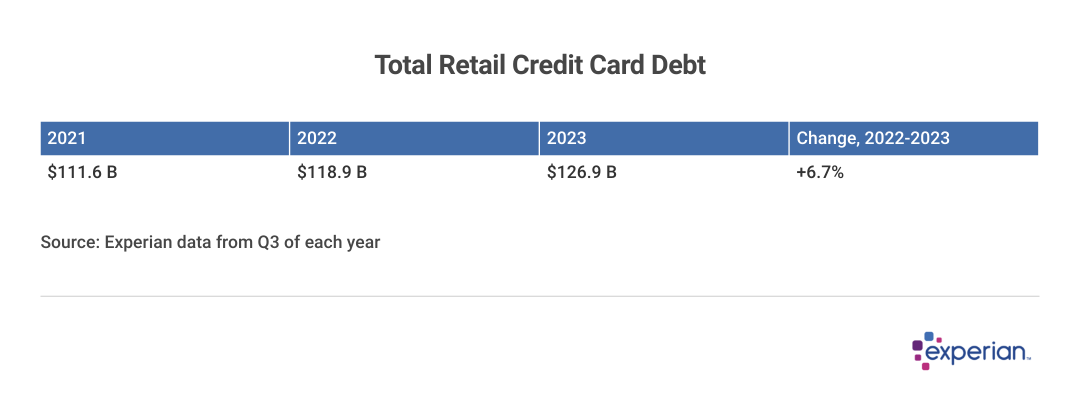

Total Retail Credit Card Debt Increased by 6.7%

While inflation had begun to moderate in 2023, balances on store credit cards remained elevated from the previous year. Despite there being fewer retail credit card accounts than in 2022, the average balances of those remaining accounts grew an average of 6.7% by the end of the third quarter (Q3) of 2023, from $118.9 billion to $126.9 billion.

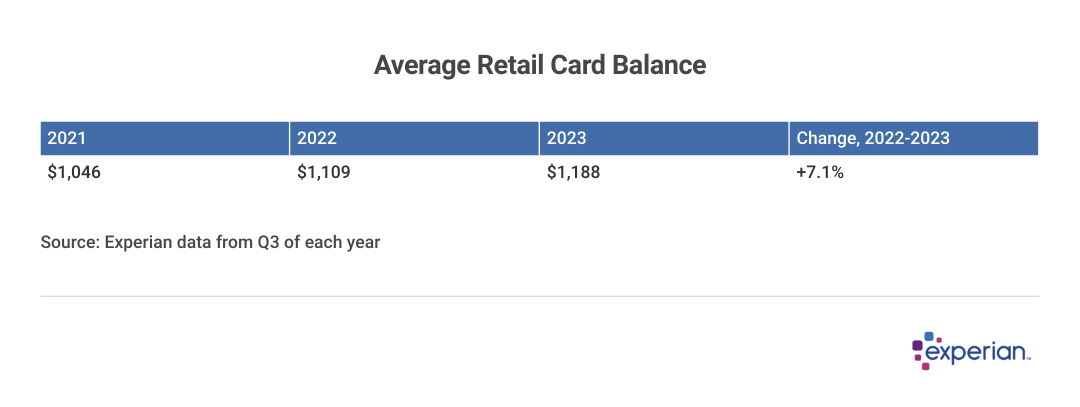

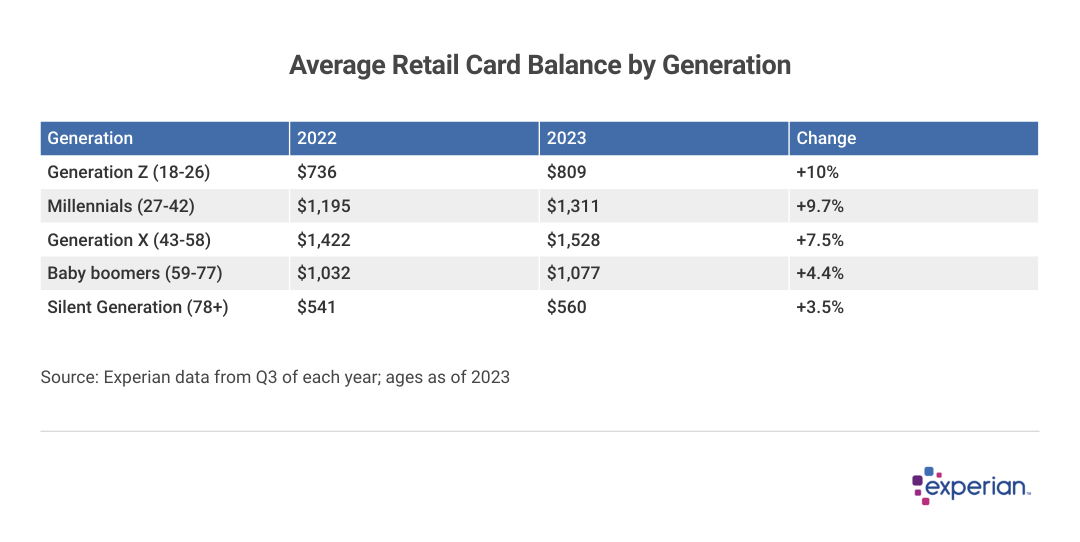

Balance Growth Percentage Surpassed Overall Debt Increase

Average retail card balances grew by a similar amount last year, increasing by 7.1% to $1,188 as of Q3 2023.

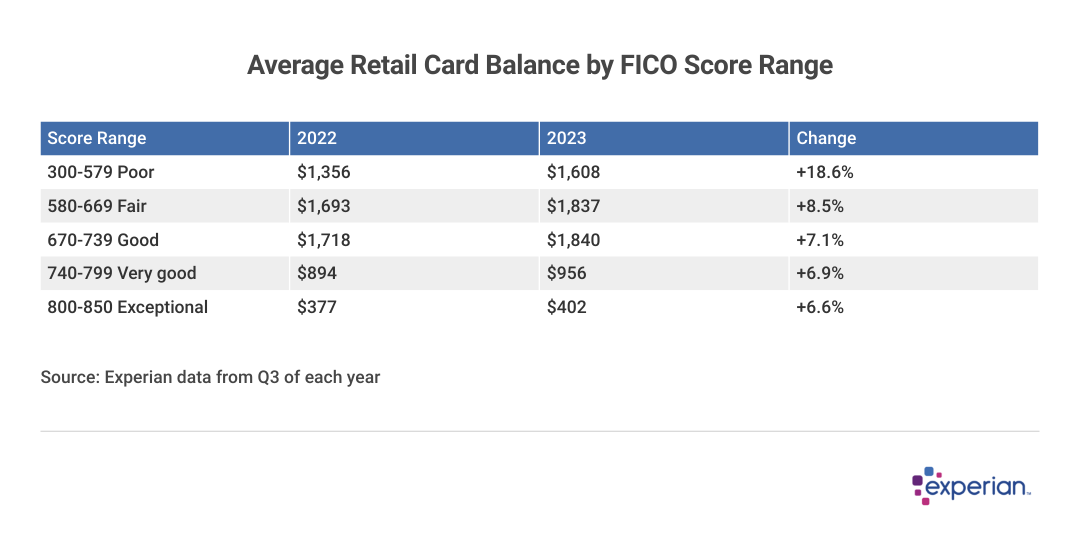

Those With Poor Credit Scores Growing Their Balances the Fastest

Those with fair and especially poor credit bore the brunt of retail card balance increases, in no small part due to higher interest rates on cards that already sport above-average APRs. A $1,600 retail card balance with a 30% APR paid off over the course of a year will cost that consumer about $270 in interest charges, regardless of credit score.

Consumers with lower credit scores are more likely to use store credit cards than general purpose credit cards. But unlike consumers with higher credit scores, they may not be as able to transfer their retail card debts to lower-cost financing, like personal loans or 0% intro APR balance transfer offers.

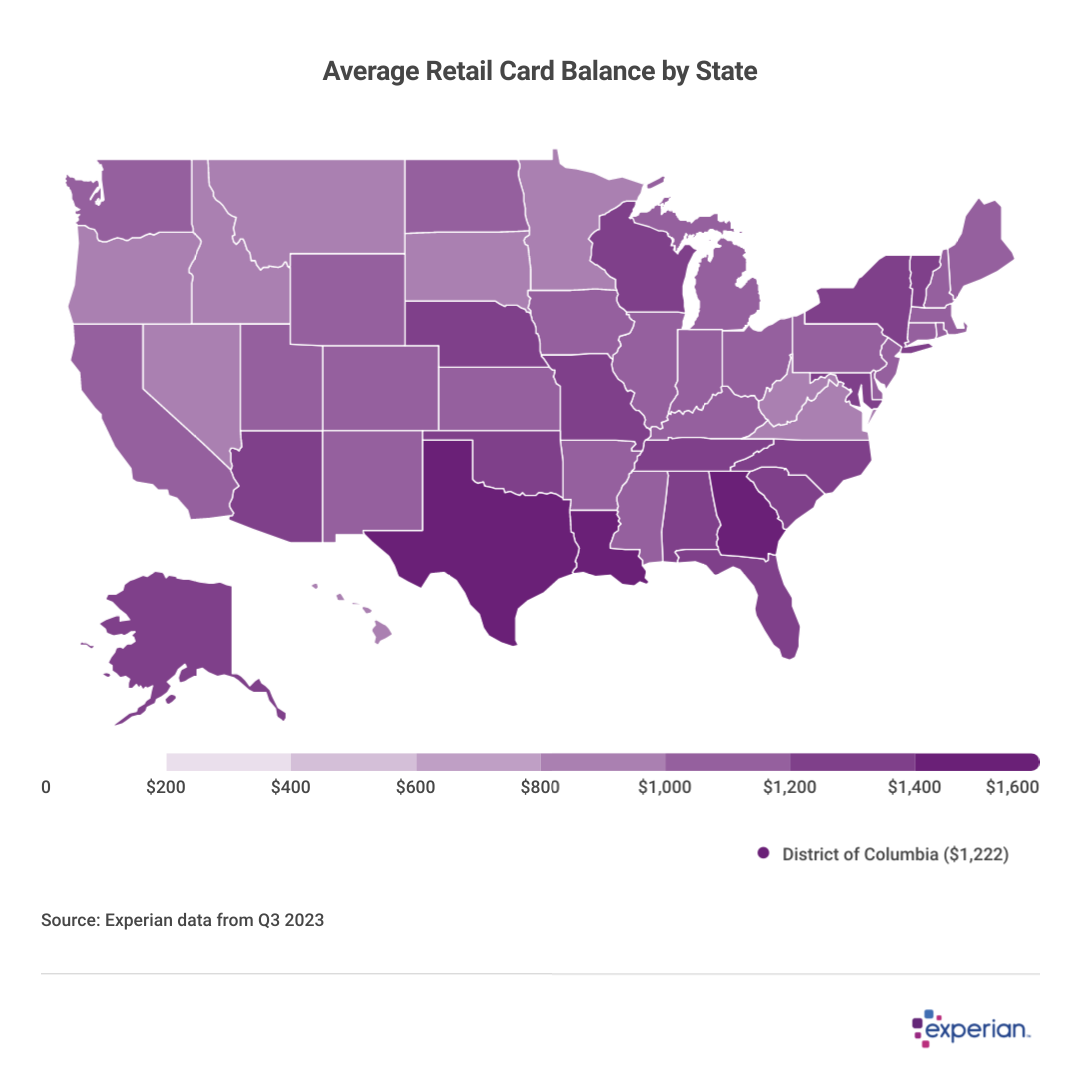

Average Retail Card Balances Rose Nationwide

The average retail card balance increased across all states and Washington, D.C., with Texas having the highest average balance and relatively retail-light Hawaii having the lowest. Even in states where average balance growth was moderate, the annual increase was at least 4%.

States From Coast to Coast See Balances Go Up

States with generally greater economic growth tend to see the greatest jumps in balances. Illinois, Massachusetts, Montana, Oregon, Virginia and Washington state all saw balances increase by more than 10% in 2023.

Younger Generations Add to Their Retail Card Balances, Despite Buy Now, Pay Later

Balances on store cards increased the most among the younger generations in 2023, although Generation X still carries the largest balance of any generation by a wide margin. Despite growing more slowly, Generation X leads this debt category—just as they do for credit cards, mortgages and most other types of consumer credit—with an average balance of $1,528.

More Consumers Consider Buy Now, Pay Later an Option

With consumers already experiencing interest rate jumps in other purchases in their lives, it is no wonder many are increasingly gravitating toward more convenient and cost-effective forms of financing when they're available—even if they aren't always big-ticket purchases. (The average buy now, pay later loan size was only $135 according to a 2022 buy now, pay later study by the Consumer Financial Protection Bureau.)

As the Federal Reserve Bank of Boston notes in a recent detailed report on buy now, pay later financing, they're gaining wider traction among consumers over the past couple years.

- Wider consumer recognition: Most consumers (77%) have heard of buy now, pay later plans, and more than half remember being offered it as a choice of payment in the past month. Roughly half of consumers (53%) knew what buy now, pay later plans were in 2021.

- Wide range of users, but flourishing among high earners: Buy now, pay later plans are most popular among consumers earning $75,000 to $100,000 annually, according to the Boston study. In addition, at least 1 in 10 consumers with annual incomes under $75,000, including those making under $25,000 annually, used buy now, pay later in the past month—suggesting a wide breadth of adoption.

- Consumers with higher FICO Scores gravitate to buy now, pay later: Although you may not need a credit score to qualify for a buy now, pay later offer, most consumers using these plans already have a credit score. In general, those with lower FICO Scores use buy now, pay later plans more frequently than other consumers. At least 20% of consumers with a FICO Score of 649 or lower used buy now, pay later plans in the past month, versus 9.3% overall. However, users in all credit score bands—even exceptional ones above 799, use buy now, pay later to some degree.

- Big-ticket purchases are more common: Although buy now, pay later plans are often associated with smaller impulsive buys, big-ticket items are one reason buy now, pay later plans are growing. Bigger-ticket buy now, pay later purchases—those costing more than $1,000—are now frequent. Among spending categories financed with buy now, pay later, home furnishings and appliances were by far the most common purchase, according to Pymnts Intelligence data, with vacation packages and airfares also common uses for big-ticket buy now, pay later plans.

- Popular among the cash-crunched: Although buy now, pay later users have similar levels of credit card debt as those who don't use this payment method, they have much lower balances in their checking accounts, the Federal Reserve Bank of Boston data shows. This provides further evidence that buy now, pay later plans are used by some consumers as a cash flow management tool, particularly by those whose incomes fluctuate from month to month, such as those of many gig economy workers.

Retail Card Spending Is Much More Modest Than Other Credit Card Spending

The relative size of their total debt and average balances shows the smaller role store credit cards are playing in today's economy. The $127 billion in retail card balances is about one-eighth the size of outstanding credit card debt.

Estimates suggest that buy now, pay later plans are even smaller. Consumers collectively carry about $15 billion in buy now, pay later debt (as measured by the amount in loans of the top three lenders in the industry outstanding at any one time), according to Fisher Investments.

However, within that smaller space, buy now, pay later is growing in popularity among consumers, particularly younger ones. Meanwhile, an increase in retail card balances, boosted by even higher-than-usual retail credit card APRs, shouldn't be construed as evidence that retail card popularity is on the upswing.