What auto loan rate can you qualify for based on your credit score?

What auto loan rate can you qualify for based on your credit score?

Auto lenders consider a variety of factors when determining your loan interest rate, including your credit score.

In the past year, interest rates have risen across the board for consumers, with borrowers who have better credit scores generally seeing the highest increases. While interest rates are expected to remain relatively high for some time, it's still possible to obtain a low rate if you have good or excellent credit. Experian's quarterly State of the Automotive Finance Market Report takes a look at the average auto loan interest rate paid by borrowers whose scores are in various credit score ranges.

Here's what to expect.

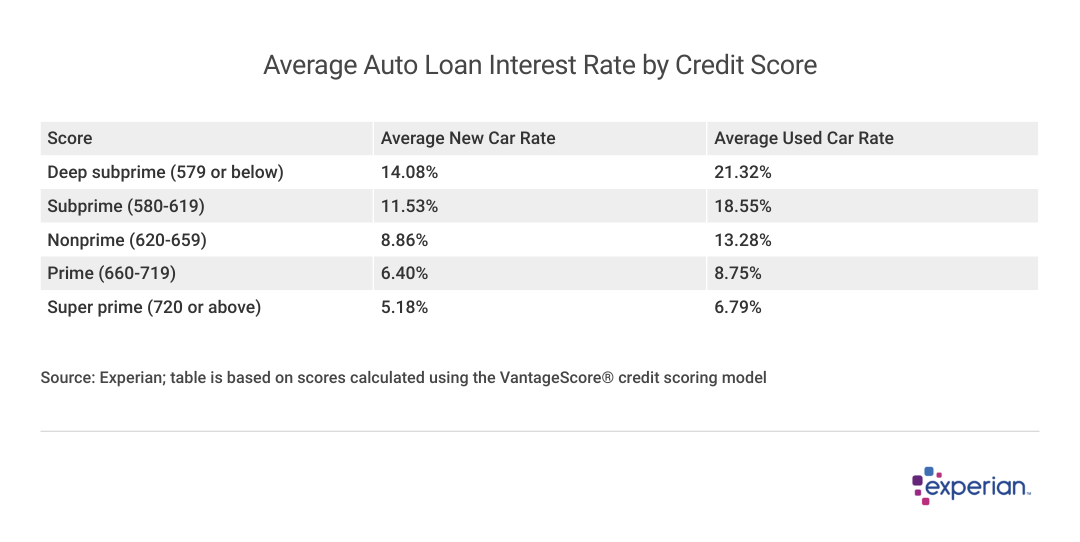

The average car loan interest rate can depend on credit score

As of the first quarter of 2023, borrowers with the highest credit scores were, on average, nabbing interest rates just above 5% on new cars. Interest rates on used cars were higher, with the highest-score consumers paying an average rate of 6.79%. Here's what you can expect from auto loan rates for new and used cars.

Your interest rate can also vary if you finance a vehicle purchased through a franchise dealer versus an independent dealer. In general, franchise dealers can get you a slightly lower rate with in-house financing, also known as captive financing.

How do auto loan interest rates work?

Auto loan interest rates are determined through risk-based pricing. If a lender determines you're more at risk of defaulting on your loan because of your credit score and other factors, you'll typically be charged a higher interest rate to compensate for that risk.

Factors that can impact your auto loan interest rate include the following:

Credit score and history

Even if your credit score is relatively high, you may still end up with a higher interest rate if there are negative items on your credit report, such as missed payments, collection accounts, repossessions, and bankruptcy.

Loan term

The longer your repayment term, the more risk it carries for the lender—both that you might default on your payments and that market interest rates may increase, making your loan less profitable than new loans.

You may be able to score a lower interest rate by going with a shorter repayment term. Just remember that shortening your loan term will also increase your monthly payments.

Down payment

Putting more money down on your vehicle purchase reduces how much you need to borrow, thereby decreasing the risk associated with your loan. As a result, a larger down payment may result in a lower interest rate.

New vs. used vehicle

Auto manufacturers provide many incentives for car buyers to purchase new vehicles, including lower interest rates through their financing companies. Other lenders, including banks and credit unions, may also lower their rates to compete. In contrast, if you're buying a used car, there's no incentive for lenders to offer lower rates, which results in higher rates on average.

Income and Debt

Lenders will consider your debt-to-income ratio (DTI), or how much of your gross monthly income goes toward debt payments. A high DTI may be a sign that you can't take on any more debt without putting stress on your budget and may result in a higher interest rate.

The lender

Each lender has its own criteria for determining auto loan interest rates and may have differing starting and maximum rates.

Whatever auto loan interest rate you qualify for, it'll be represented in the form of an annual percentage rate (APR). Your APR will affect your monthly payment amount as well as how much the loan will cost you over the life of the loan. Due to a process called amortization, you'll pay more interest at the beginning of the loan term than at the end.

How to improve your credit score

Your best bet for securing a lower interest rate is to increase your credit score. Depending on your situation, though, this process can take several months or possibly even years. If you can't wait, taking these and other steps can still help you.

For example, you may be able to refinance at a lower rate in the future, or you can score a lower rate on your next auto loan. Either way, here are some ways you can build your credit right now:

- Review your credit report and credit score to see where you stand and which areas of your file to address.

- Catch up on past-due payments to avoid further damage to your score.

- Pay down your credit card balances to reduce your credit utilization rate.

- Limit new credit applications to keep hard inquiries from having a compounding effect on your credit score.

How and where to get a lower auto loan interest rate

Here are some steps you can follow to maximize your interest savings on your next auto loan:

- Increase your credit score. Improving your credit score is one of the best ways to score a lower auto loan interest rate. You can do that by checking your credit score and credit report to get an idea of which areas you need to address. Common ways to improve your credit score include paying down credit card debt and making sure any past-due accounts are brought current.

- Shop around. One of the best ways to get a lower rate on your auto loan is to compare rate offers from multiple lenders. It's a good practice to apply for preapproval and get rates from at least three to five lenders to get a good idea of what you're likely to qualify for.

- Apply with a cosigner. If you don't have time to improve your credit, applying with a creditworthy cosigner may improve your chances of scoring favorable terms. The lender will consider both credit profiles to determine the loan's risk and your interest rate.

- Make a larger down payment. Again, putting more money down reduces how much you owe and the loan's risk to the lender. If you can afford it, consider making a larger down payment to save money with a lower rate.

- Opt for a shorter repayment period. A shorter repayment term will result in a higher monthly payment. But if you can afford it, it could help you qualify for a lower rate on your loan and reduce your overall interest costs.

If you don't have time to take some of these steps, you can continue your efforts after the vehicle purchase and potentially refinance the loan with better terms at a later date.

Where to get the best auto loan rate

There are a few different places you can get an auto loan, giving you more options to compare and ensure you get the best rate available.

- Dealerships: If you want to minimize the amount of time you spend on your loan, consider dealer-arranged financing. You'll fill out a credit application at the dealership, and the dealer will submit it to multiple lenders and give you the best rate. That said, the dealer may mark up the interest rate and take the difference as compensation. Some dealers offer buy here, pay here financing arrangements, but the costs can be prohibitively expensive.

- Banks: Traditional banks can be a good place to start if you have an account with one. However, they typically don't offer the lowest interest rates.

- Credit unions: Credit unions often offer low interest rates compared to other channels, but you'll likely need to join the credit union and open a checking account to get approved. Depending on the institution, the membership requirements may not be easy to meet.

- Online lenders: Online lenders can also offer lower interest rates compared to banks and dealerships, primarily because they don't have the overhead costs associated with physical branches.

Maintain good credit for future auto purchases

While improving your credit for your next car purchase can save you money in the short term, maintaining good or excellent credit can provide even more savings in the long run, both on future auto purchases and other financing options.

Make it a goal to monitor your credit regularly to keep an eye on your credit score and the different factors that influence it. Keeping track of your credit can also help you spot potential fraud when it happens, so you can address it quickly to prevent damage to your credit score.

This story was produced by Experian and reviewed and distributed by Stacker Media.