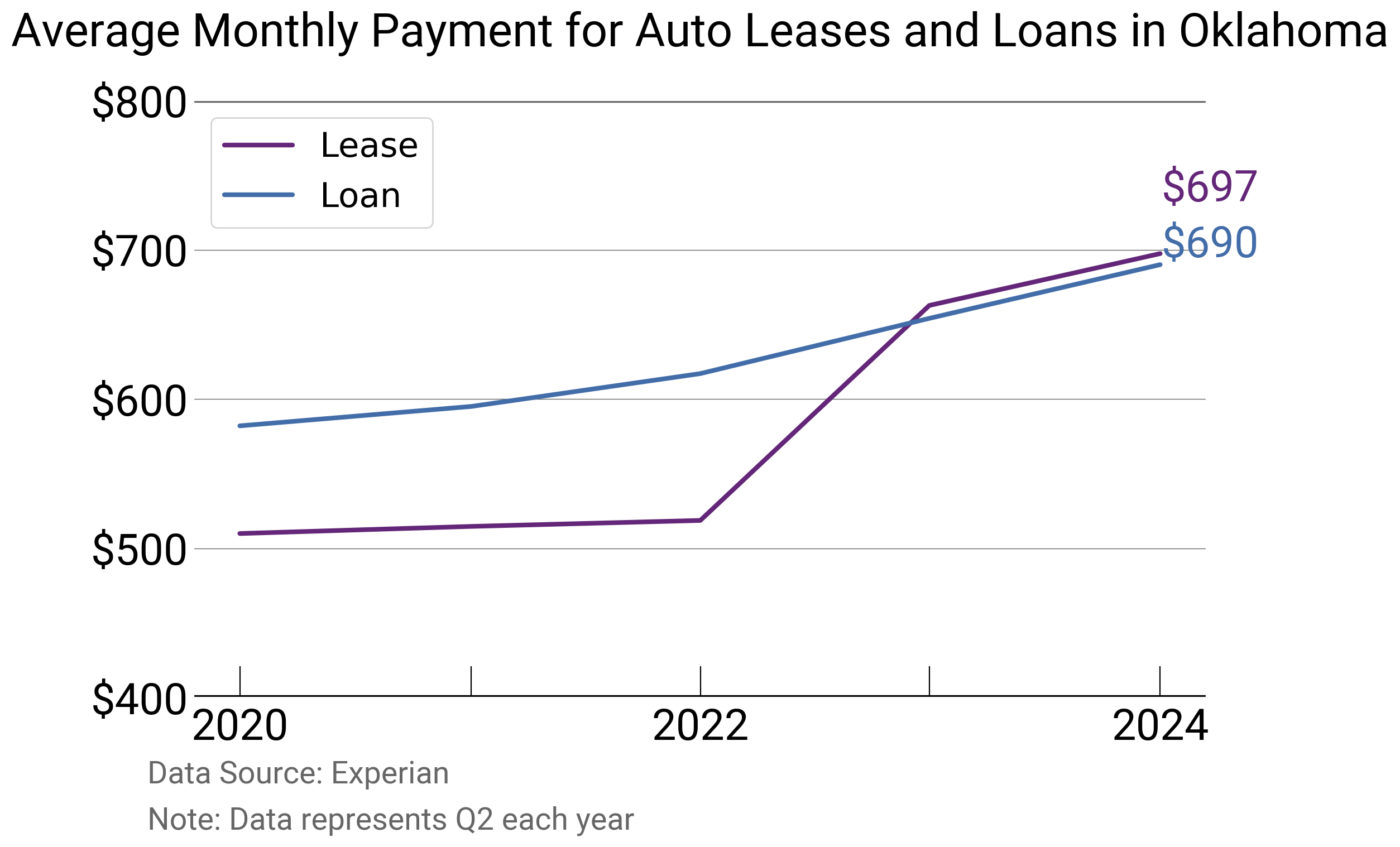

Average auto lease payments are increasing in Oklahoma

Average auto lease payments are increasing in Oklahoma

While the majority of drivers still finance their vehicle with a loan, a share of drivers in the U.S. choose to lease. Leasing can have a few advantages over buying, such as more manageable payments and warranty coverage, but some of the advantages afforded to drivers who prefer leasing to buying are disappearing in 2024.

According to national Experian data from the second quarter (Q2) of 2024, the average auto lease payment was $638—lower than the average monthly auto loan payment of $655. The difference between average lease payments and average auto loan payments has narrowed from a $54 in 2022 to a mere $17 in 2024.

Contrary to the broader national trend, however, lease payments in Oklahoma are more expensive than loan payments. Oklahoma is one of only 13 states and Washington, D.C., with a higher average lease payment than loan payment.

In Q2 2024, about 8% of all financed vehicles on the road were leased versus 92% of vehicles that were financed with a loan. However, the share of those who lease versus buy has fallen by one-third since 2020, when 12% of auto financed rides were leases.

Drivers who choose to lease a car are often motivated to buy a lower monthly payment for a leased vehicle versus its loan-financed equivalent—most three-year lease payments are lower than four-year, five-year and even longer auto loan payments.

However, the payment advantage of leasing a vehicle has diminished or disappeared entirely when compared to purchasing a car in 2024. In Oklahoma, a lease costs $7 more than an auto loan.

In this report, we'll look into anonymized and aggregated Experian data to provide an overview of the current lease market, recent trends and whether there will be more leasing or less in 2025 and beyond.

Average auto lease payment increasing in Oklahoma

The average auto lease payment in Oklahoma grew $35 from June 2023 to June 2024, reaching $697. Oklahoma has the 7th highest average auto lease payment among all states and $59 higher than the national average of $638.

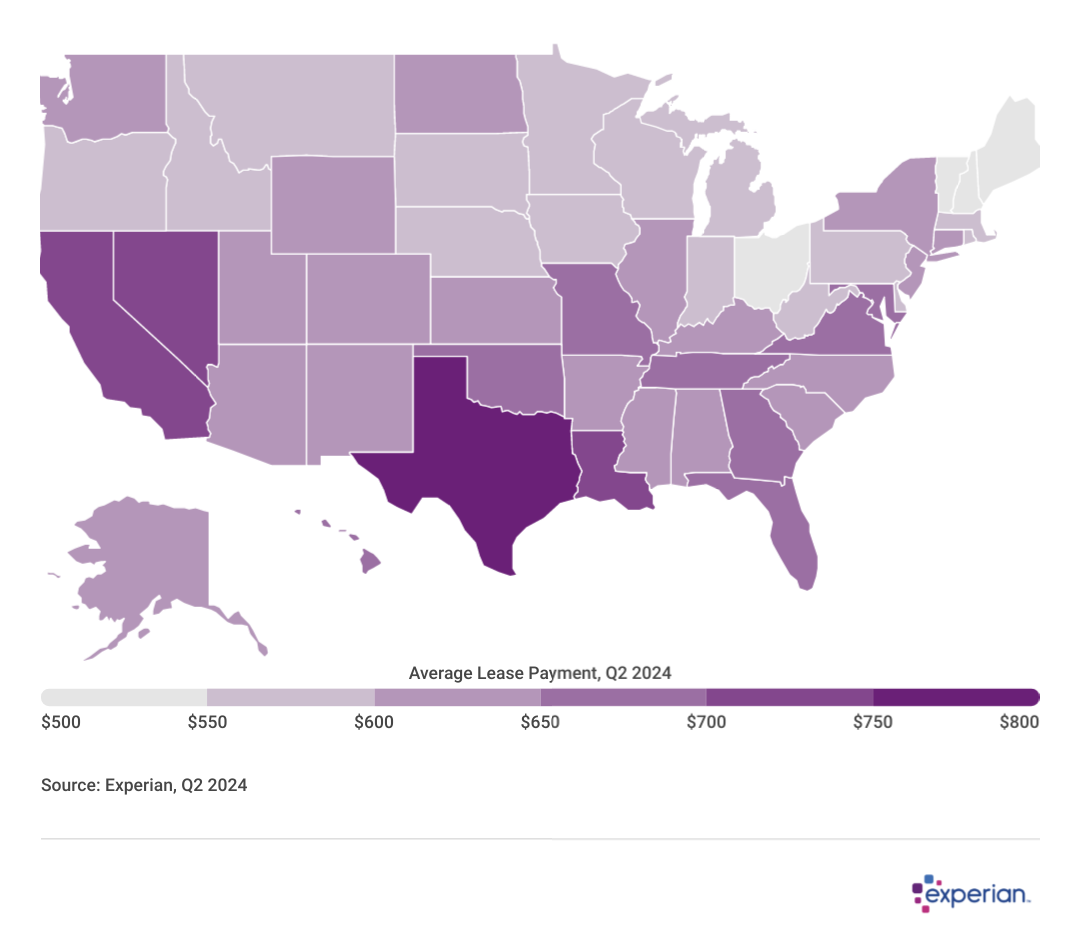

States with the highest average auto lease payment

#1. Texas: $761

#2. Washington, D.C.: $739

#3. California: $734

#4. Louisiana: $714

#5. Nevada: $708

States with the lowest average auto lease payment

#1. New Hampshire: $529

#2. Maine: $532

#3. Vermont: $542

#4. Ohio: $545

#5. Michigan: $553

Similar to lease payments, average auto loan payments also grew in Oklahoma by $36 to $690. Oklahoma has the 9th highest average auto lease payment among all states and $35 higher than the national average of $655.

States with the highest average auto loan payment

#1. Texas: $777

#2. New Mexico: $728

#3. Louisiana: $726

#4. Wyoming: $723

#5. Arkansas: $699

States with the lowest average auto loan payment

#1. Rhode Island: $549

#2. Michigan: $562

#3. Massachusetts: $571

#4. Connecticut: $580

#5. Oregon: $583

Leasing Among the States: Hot Spots and Their Explanations

While not exactly a crazy quilt of states with wildly disparate leasing payment averages, there are some hot spots and cold spots for monthly lease payments.

Cold Spots

Beginning with the cold spots, New England generally sees the smallest average monthly lease payments. New Hampshire ($529), Maine ($532) and Vermont ($542) are ranked first, second and third among the states with lowest average lease payments.

Let's break those averages down a bit, keeping in mind creditworthiness is among the factors that determine a consumer's lease price in the first place. As of June 2024, the average credit score of consumers in Vermont was 737, in New Hampshire 736 and in Maine 731. All averages are well above the national average of 715, which put more drivers in a position to lease with lower monthly payments.

It could also be that lessees in these states prefer less expensive models than lessees in other states, which would also result in lower payments. For example, modestly priced Subarus are overrepresented in these New England fleets.

Hot Spots

Now for the hot. That includes California and Texas—but mostly Texas.

Both states have near-average credit scores, which make sense as the two states represent a large percentage of the U.S. population. However, the average monthly lease payment in Texas is $761, considerably higher than the average of $734 for lessees in runner-up California. Following are neighbors of each respective state—Louisiana ($714) and Nevada ($708).

One possible explanation for higher monthly lease payments in Texas may be how taxes on leased vehicles are collected. Texas, and some other states, collect the full sales tax amount of the vehicle from the lessee. Although this tax is spread across the monthly payments of a lease, it still makes the lease payment even higher than in states that don't collect sales tax on the entire cost of the vehicle during the leased period.

But taxes only partially explain the No. 1 Texas ranking: Illinois, another state with upfront sales tax collection, has average monthly lease payments more than $100 less, at $648. As with New England, vehicle preferences likely play a role in monthly payments for leases in Texas. Full-sized trucks, such as the Ford F-150 and the Ram 1500, dominate the most popular vehicles list in the state, with many 2025 model trims exceeding $50,000 MSRP.

Drivers Who Lease Have Solid Credit Scores on Average

When looking at average credit scores of drivers with a lease payment, one aspect that jumps out is that average credit scores among that group are consistently higher than those who finance with a loan.

While the gap has tightened over the years, the average FICO Score of a lessee in 2024 is 728—still significantly higher than the average credit score for those with auto loans. However, that 728 average has remained nearly unchanged since 2016. Meanwhile, the average score of those with car loans have improved at a rate similar to that of the national average.

One possible explanation behind the consistent higher-score profile of lessees is that many auto dealers require a minimum credit score to qualify for a lease. While that minimum may vary by dealer and location, it's typically somewhere below the current national average of 726 among lessees.

New and Old Drawbacks to Leasing

Leasing has advantages and disadvantages. Usually, leasing a car results in two immediate benefits for the lessee: a briefer commitment with a new vehicle over buying a new car (nearly all leases are for new vehicles), and a somewhat lower payment than they would pay for a similar purchased vehicle. However, the window on lower monthly payments appears to be closing compared with auto loans, and already has in some states, reducing that previously built-in advantage.

But the most obvious disadvantage is one that's always existed: Leased vehicles aren't building any equity. After three years—the typical lease arrangement in the U.S.—the lessee has nothing to show for their monthly lease payment. The dealer may offer the lessee the option of purchasing the leased vehicle (which has significantly depreciated in value), but, possibly more likely, lessees repeat the leasing process, and never really feel the somewhat fleeting bliss of the last car payment.