Best and worst metro areas for first-time homebuyers in 2024

This story was produced by Creditnews and reviewed and distributed by Stacker Media.

Best and worst metro areas for first-time homebuyers in 2024

The past few years have been one of the worst periods for first-time homebuyers in America's history.

Record home prices, chronically low inventory, 22-year-high mortgage rates, and bidding wars with cash- and equity-flush buyers have locked many younger buyers out of the housing market.

According to the National Association of Realtors (NAR), first-time homebuyers made up just 32% of all transactions last year—the fourth-lowest share seen in more than 40 years.

While would-be homeowners bide their time, Creditnews Research looked at America's 50 largest metro areas to uncover housing markets that are still attractive for first-time buyers.

Our ranking shows how easy it is for residents in each metro area to take out a mortgage for a starter home—defined as homes with a resale value within the 5th to 35th percentile range.

Primary factors in our scoring model include mortgage affordability, market access, and bargaining power. We also looked at macro indicators, such as employment growth and livability.

Combined, the weighted scoring model provides a holistic snapshot of America's largest metro areas that offer first-time buyers the best bang for their buck.

Some of the results may surprise you.

Best metro areas for first-time buyers

Based on Creditnews Research's scoring model, the top metro areas for first-time buyers are:

- Pittsburgh: America's steel town is an excellent place for first-time homebuyers because it offers the best affordability for a starter home. No other metro area in our ranking offers a lower mortgage payment relative to income. Pittsburgh also ranks second in terms of listing price cuts—giving buyers strong bargaining power when house hunting. Pittsburgh's labor market isn't exactly booming (it ranks 31st for employment growth), but its job growth is still positive. In this remote work age, the Pittsburgh metro area, made up of five counties, can be an attractive place to live, even for families who aren't employed in local manufacturing.

- Austin-Round Rock: Austin has experienced a population explosion in recent years, making homes at the higher end of the spectrum hard to afford for first-time buyers. But those shopping for starter homes can still find a decent value. The Austin metro area, which includes five counties, ranks first for market access—with its home listings staying on the market the longest. Austin is also a top-10 city for employment growth and is one of the most livable cities in America when it comes to amenities, culture, and healthcare. The trade-off is mortgage affordability (29th). Families in Austin have a much higher income than the national average, but starter homes are priced at $331,565—bringing the average mortgage payment to a hefty $2,259 a month.

- San Antonio-New Braunfels: Roughly 80 miles from the state capital, the San Antonio-New Braunfels metro area is the third most affordable place for first-time homebuyers. And, San Antonio ranks second in market access, suggesting much lower competition among buyers than the national average. It's also a top-10 area for employment and livability but doesn't rank as highly as Austin in either category. It does, however, boast much better mortgage affordability and bargaining power than Austin, ranking 6th and 4th among other metro areas, respectively.

- Birmingham-Hoover: Alabama's largest metro area, consisting of seven counties, has seen its population steadily decline over the decades, but still offers first-time buyers a little bit of everything: mortgage affordability (6th), bargaining power (4th), and employment growth (5th). Over the past year, employment in the area has increased by 3%, making it one of the fastest-growing labor markets in the country.

- Jacksonville: Wrapping up our top 5 ranking is metro Jacksonville, which includes four counties and is the 4th largest metropolitan area in Florida. Jacksonville makes the list thanks to its strong market access (4th) and good livability (12th). What makes Jacksonville a major standout on this list is its labor market. After registering a whopping 3.8% increase over the past year it ranks first in employment growth. The only caveats to Jacksonville are mortgage affordability (28th) and bargaining power (32nd), which rank middle of the pack. Still, starter home prices are highly affordable compared to other major metro areas.

Pittsburgh: Steel town becomes boom town?

While Pittsburgh doesn't get as much spotlight as Austin and other Sun Belt cities, the steel town punches above its weight in giving the best bang for the buck for first-time homebuyers.

What makes Pittsburgh such an attractive place for first-time buyers is the affordability of its starter homes, which typically go for $107,912—the lowest among other metro areas in our ranking.

Even at the current mortgage rates, a mortgage for such a home, including fees and insurance, would come to around $850 a month.

That translates to just 14% of the median monthly household income in Pittsburgh, meaning many middle-class households can easily afford two starter homes.

Pittsburgh is also one of the few metropolitan areas where the average household can afford a median-priced home.

As such, the Pittsburgh metro ranks #1 in our mortgage affordability ranking.

Perhaps more surprising is the fact that Pittsburgh's unemployment rate is well below the national average. Its cost of living is also lower than the U.S. average.

Even investors have recognized the real estate potential in the steel town.

In 2021, nearly 25% of homes sold in the city were to investors or corporations—up from 15.5% in 2010, according to the local nonprofit Pittsburgh Community Reinvestment Group.

Unlike other investor-infested housing markets, however, Pittsburgh continues to offer the best value among the top 50 metro areas.

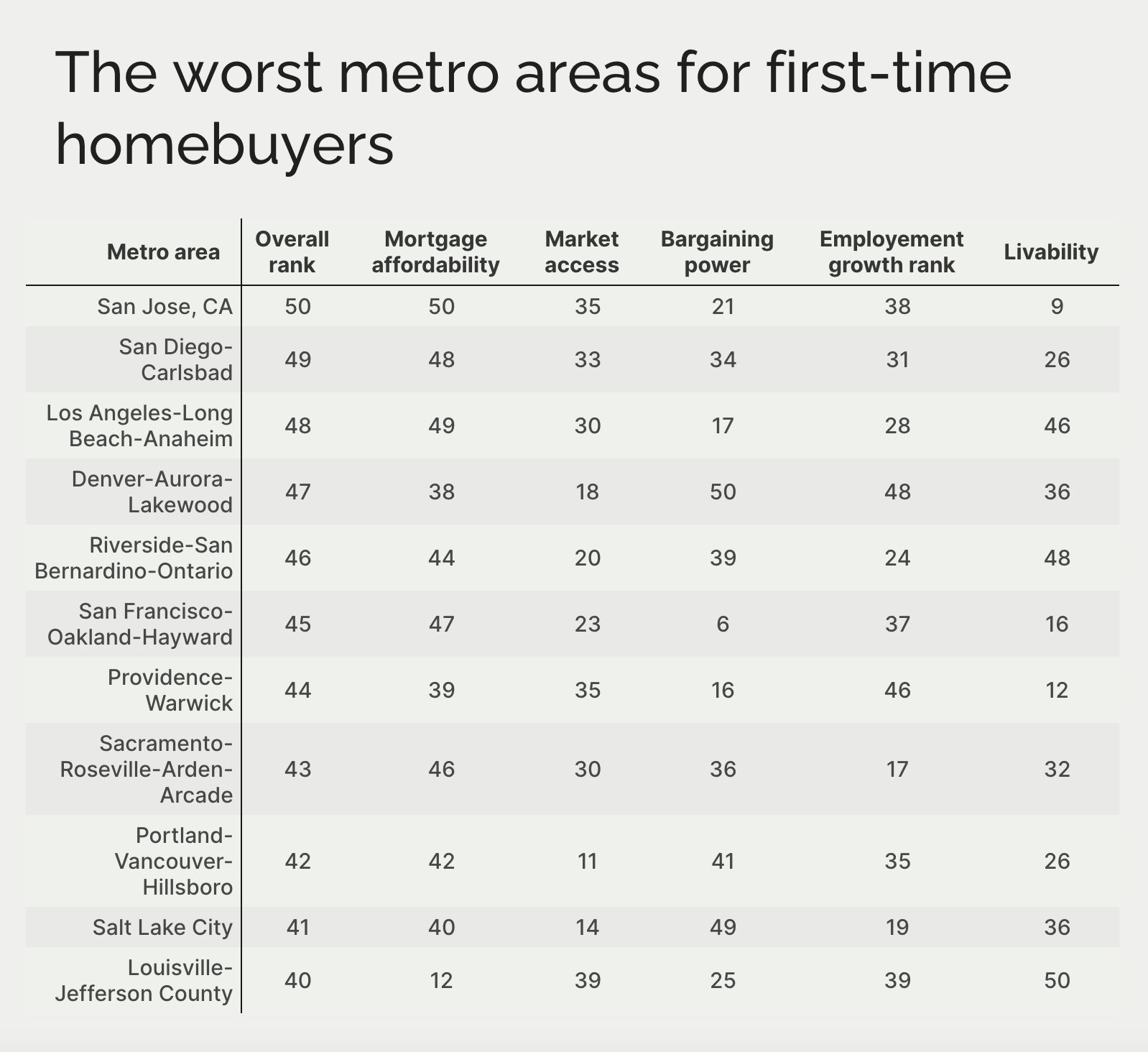

Worst metro areas for first-time buyers

Not surprisingly, California dominates the bottom of the rankings because of its lack of mortgage affordability, relatively weak market access, and diminished bargaining power.

The bottom five metro areas in our ranking are:

46. Riverside-San Bernardino-Ontario: Riverside's close proximity to Los Angeles has made it an attractive destination for Californians. Despite being a growing city with lots of amenities, the third largest metro area in California, which includes Riverside and San Bernardino counties, ranks 48th for livability due to its high cost of living. Mortgage affordability for a starter home is also among the worst (44th), mainly because of elevated housing costs. Riverside residents also lack bargaining power—the metro ranks 39th in that category.

47. Denver-Aurora-Lakewood: The mile-high city ranks dead last for bargaining power—meaning residents there shouldn't expect price reductions when shopping for a starter home in this six-county metro area. Mortgage affordability is also among the lowest (38th), mostly because of elevated housing costs. Denver ranks 48th for jobs, becoming one of only a small handful of major cities to register negative employment growth.

48. Los Angeles-Long Beach-Anaheim: With an average starter home price of $645,196, Los Angeles, the most populous metropolitan area in the country, is one of the worst cities for first-time homebuyers. Elevated housing costs have pushed down mortgage affordability—the city ranks 49th in this category. Los Angeles also ranks poorly for livability (46th) due to a high cost of living, crime, and poor access to health care.

49. San Diego-Carlsbad: For first-time buyers, the San Diego metro, which encompasses all of San Diego County, is very similar to Los Angeles. The city has an average home price of $651,891 and poor mortgage affordability (48th). San Diego has a much higher livability score (26th) but ranks worse than Los Angeles for market access and bargaining power. There just aren't a lot of housing options for first-time buyers, and the prospects aren't looking up in the near term.

50. San Jose-Sunnyvale-Santa Clara: At the very bottom of our ranking is San Jose, which is an hour's drive south of San Francisco. What makes San Jose so prohibitive is its lack of mortgage affordability (50th), with starter home prices coming in at a whopping $965,068—even higher than Los Angeles. That's more than six times higher than the annual median household income in that area. A lack of market access (35th) and poor employment growth (38th) round out the reasons first-time buyers might want to (or have to) steer clear.

Methodology

To determine the best housing markets for first-time homebuyers, Creditnews Research analyzed America's 50 largest Census Metropolitan Areas (CMAs) by population using a weighted sum scoring model, including four criteria.

Mortgage affordability (40%)

To assess mortgage affordability, Creditnews Research estimated the minimum gross household income first-time buyers need to qualify for a mortgage on a starter home in that metro area, defined as a median-priced home in the sample of home sales falling in the 5th to 35th percentile range for December 2023. Home prices were smoothed and seasonally-adjusted.

The minimum income threshold was calculated using a rule of thumb that mortgage costs, including fees and insurance, shouldn't exceed 28% of a household's gross income. The model assumes a 10% down payment and a 30-year fixed-rate mortgage of 6.5%—the consensus 30-year fixed-rate mortgage rate prediction for year-end 2024.

That threshold was then compared to the median household income for 2022 in each metropolitan area, which was sourced from the Census Bureau. The smaller the gap between median income and the minimum income needed for a starter home, the higher the mortgage affordability score.

2022 is the latest normalized data available on median household income in each metropolitan area from the Census Bureau.

Market access (15%)

Market access in each metro area was determined by calculating a median number of days all homes listed or updated on Zillow in December 2023 stayed on the market after first being posted for sale. The longer the median lead closing time, the higher the market access score.

Bargaining power (15%)

To determine the bargaining power of first-time buyers, Creditnews Research calculated median price cuts on listings before closing in each metro area expressed as a percentage of the median starter home price in December 2023.

Employment growth (20%)

Year-over-year employment growth in each metro area as of November 2023.

Livability (10%)

For the most universal and normalized livability benchmark, Creditnews Research relied on widely-recognized Areavibes.com's Livability index, which factors in amenities, commute, cost of living, crime, employment, health, housing, and schools.

Metro sample selection

Creditnews Research focused its analysis on the top 50 metro areas by population because first-time homebuyers are more likely to move for work, and typically seek out larger cities for employment.

While there may be smaller cities that offer cheaper housing, larger metropolitan areas are less likely to offer the blend of employment opportunities, labor market tightness, and housing stock.

Sources

- Census Bureau Labor Force Statistics (November 2023)

- Areavibes.com Livability Scores

- Census Bureau Household Income Statistics (2022)

- National Association of Realtors

- Zillow Median Days to Pending data set (December 2023)

- Zillow Home Value Index data set (December 2023)

- Zillow Median Price Cut data set (December 2023)