The complete guide to IEEPA tariff refunds

Recent legal developments have opened the door to significant tariff refunds under the International Emergency Economic Powers Act (IEEPA). For business owners, this presents both an opportunity and a compliance challenge. Importers should file protests promptly to protect their rights and eligibility for refunds during the administrative review cycle.

This guide from Polston Tax clarifies what the ruling means, who qualifies and how to act. You will find clear explanations, practical steps and key deadlines to help you navigate the refund process with confidence and accuracy.

Key Takeaways

- Up to $175 billion in refunds may be available to qualifying importers affected by now-unlawful IEEPA tariffs.

- Businesses must take proactive steps to identify eligibility and file claims within strict deadlines.

- Only certain importers, primarily the Importer of Record (IOR), meet the official eligibility criteria.

- The ruling applies only to IEEPA tariffs, not Section 232 or Section 301 duties.

What Are IEEPA Tariffs and Why Were They Ruled Unlawful?

On Feb. 20, 2026, the U.S. Supreme Court issued a decision to implement the Trump tariff refund bill.

IEEPA tariffs were imposed under the International Emergency Economic Powers Act, a law that allows the executive branch to regulate commerce during declared national emergencies. These tariffs were introduced as part of broader trade and foreign policy measures, often targeting goods tied to specific geopolitical concerns.

The legal challenge was whether using IEEPA to impose tariffs exceeded the authority granted by the statute. The Supreme Court ultimately determined that the tariffs weren’t implemented within the right legal framework. The ruling clarified that, while IEEPA grants broad powers, it doesn’t authorize tariff measures as applied in this case.

As a result, duties collected under these tariffs are now subject to refund, creating a pathway for affected businesses to recover funds.

In practice, these tariffs increased costs for U.S. importers across a wide range of industries. Businesses paid these duties at the time of import, often passing the costs through supply chains or absorbing them by reducing margins. Close to 60% of companies saw gross margin decrease due to these tariffs.

Determining Your Eligibility for a Refund

Before taking action, you must confirm whether your business meets the eligibility requirements. This process involves reviewing import records, understanding tariff classifications and distinguishing IEEPA duties from other trade measures.

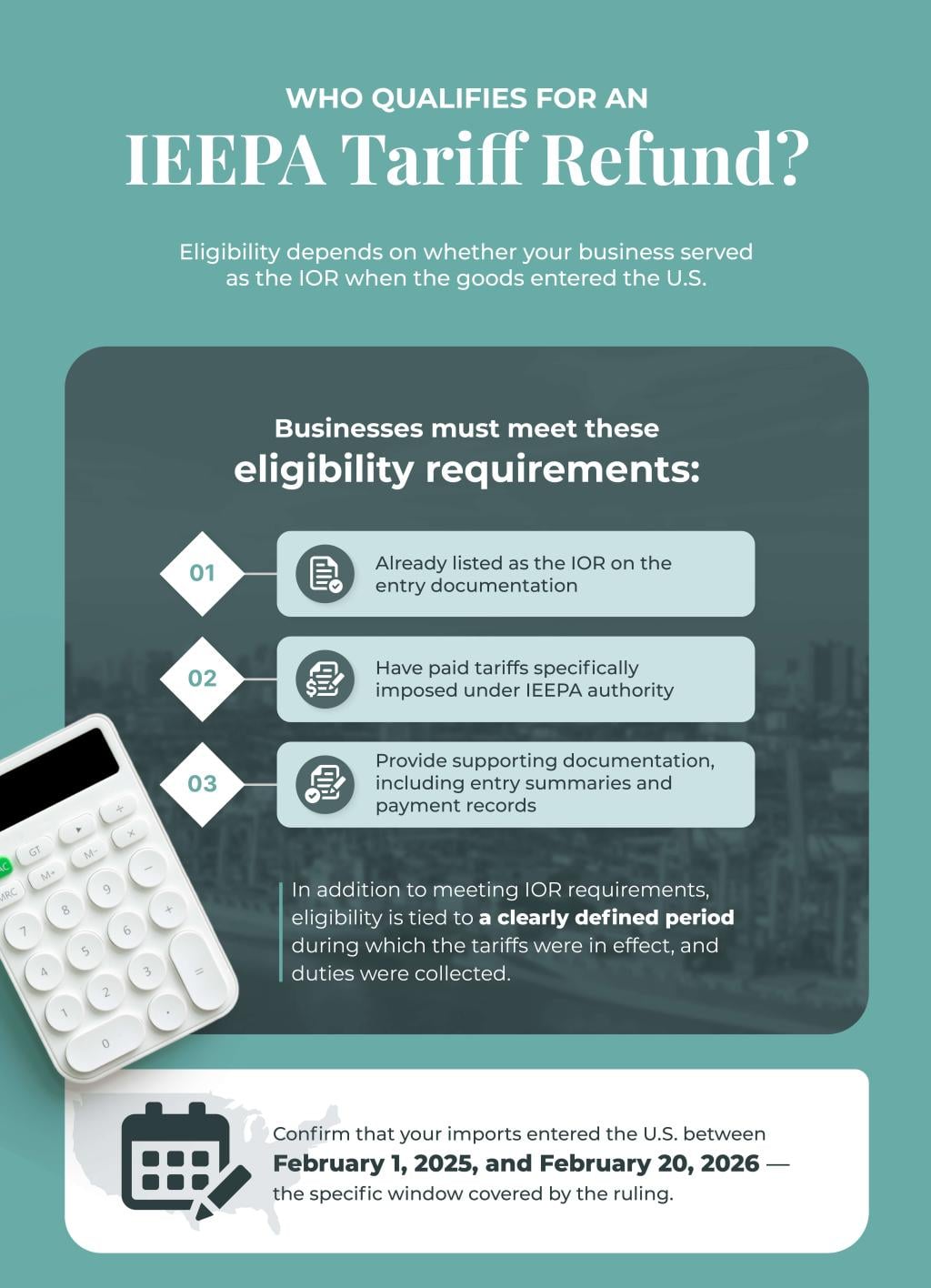

Who Qualifies for an IEEPA Tariff Refund?

Eligibility depends on whether your business served as the IOR when the goods entered the U.S. The IOR is the entity legally responsible for ensuring compliance with customs regulations and for paying applicable duties.

To qualify for a refund, businesses must meet these eligibility requirements:

- Already listed as the IOR on the entry documentation.

- Have paid tariffs specifically imposed under IEEPA authority.

- Provide supporting documentation, including entry summaries and payment records.

In some cases, third parties, such as customs brokers, facilitated the findings, but eligibility remains tied to the entity listed as the IOR. If your business indirectly bore the cost, such as through supplier pricing, it may not qualify unless it was the official importer.

In addition to meeting IOR requirements, eligibility is tied to a clearly defined period during which the tariffs were in effect, and duties were collected. Confirm that your imports entered the U.S. between Feb. 1, 2025, and Feb. 20, 2026 — the specific window covered by the ruling.

Identifying Affected Imports and HTS Codes

Determining which imports are eligible means using a detailed review of the Harmonized Tariff Schedule (HTS) codes. These codes classify imported goods and determine applicable duty rates.

To identify affected imports:

- Review the historical import data and entry summaries.

- Find the HTS codes associated with goods imported during the relevant period.

- Cross-reference those codes with lists of products subject to IEEPA tariffs.

The process may need you to coordinate between finance, procurement and compliance teams. It’s critical to classify each import accurately, as errors can delay or invalidate claims. If your business has high import volumes, you may benefit from automated data analysis tools or external expertise to ensure a complete and accurate review.

Beyond reviewing HTS codes, your business can strengthen its claims by reinforcing publicly available tariff lists and product classifications relevant to IEEPA enforcement.

Government and trade agencies release product categories that are impacted most frequently, which commonly include:

- Industrial machinery and mechanical components.

- Electrical equipment and consumer electronics.

- Raw materials and intermediate goods used in manufacturing.

- Certain chemical products and inputs.

- Selected finished goods tied to targeted trade measures.

Differentiating IEEPA Tariffs From Section 232 and 301 Tariffs

It’s essential to distinguish IEEPA tariffs from other trade measures — particularly Sections 232 and 301 tariffs:

- Section 232 tariffs are based on national security concerns and typically apply to materials such as aluminum and steel.

- Section 301 tariffs address unfair trade practices and are often associated with imports from specific countries, such as China.

Only tariffs imposed under IEEPA are eligible for these refunds. Section 232, Section 301 and Most-Favored Nation (MFN) tariffs are explicitly excluded from the refund process.

The Refund Recovery Paths

There are several potential pathways to recovering IEEPA tariff payments. Each option depends on the status of the original import entries and any prior actions taken.

Some businesses pursue administrative solutions through U.S. Customs and Border Protection (CBP), especially if entries stay open or within protest periods. This is the main avenue for refunds, using the new Consolidated Administration and Processing of Entries (CAPE) System in the Automated Commercial Environment (ACE) Portal, which went live on April 20, 2026. Others may need to file formal claims or initiate legal action through the Court of International Trade (CIT).

CBP’s CAPE Automated Refund System

Each import entry’s liquidation status is another important factor. Liquidation refers to the final consumption and duty assessment by U.S. Customs and Border Protection. Unliquidated entries or those within the allowable protest window typically offer the most direct path to recovery. In these cases, businesses can pursue administrative corrections or protests, which are more likely to result in a timely resolution.

This distinction highlights the importance of segmenting import data by liquidation status early in the process. Doing so lets companies prioritize claims with the highest recovery probability while developing strategies for more complex cases.

CBP has introduced a four-step CAPE framework to refund approximately $166 billion in duties to over 330,000 importers. In this initial phase, the CAPE system accepts submissions for entries marked as suspended, extended, or under review. However, CBP will only process refunds for unliquidated entries or those within the current 90-day voluntary reliquidation period. CBP plans to expand eligibility to liquidated entries in the future.

For validated entries, CBP will remove the corresponding HTS codes, recalculate duties, and move the entry through the standard liquidation process.

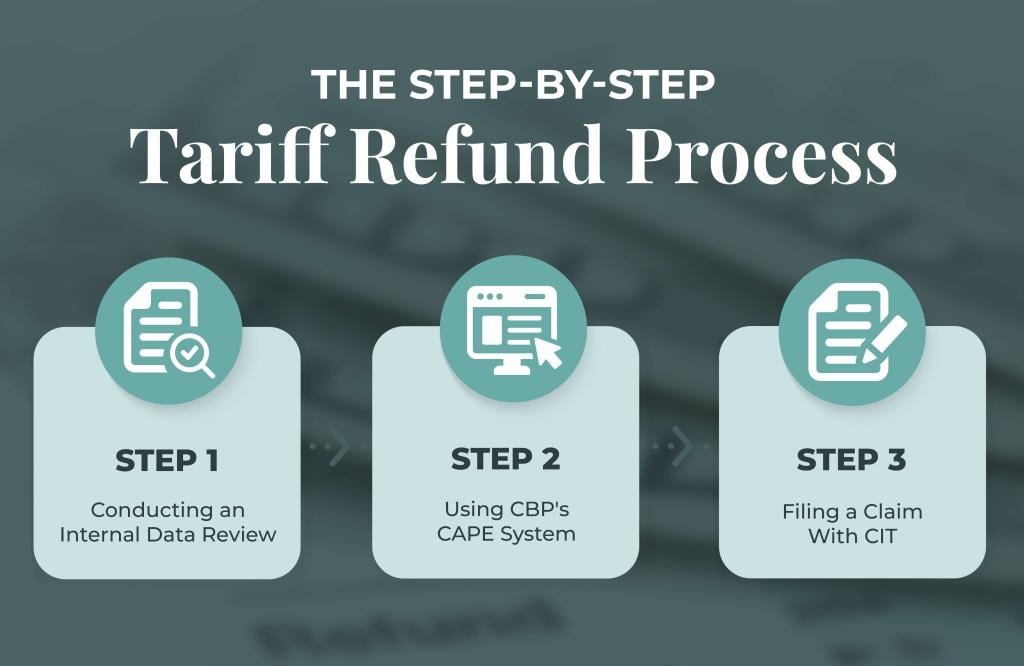

The Step-by-Step Tariff Refund Process

Claiming a refund requires careful coordination and attention to detail. It’s beneficial to use a tax professional to support you through the IRS or state taxing entity appeals process, as each step builds on the previous one, making thorough preparation crucial.

Step 1: Conducting an Internal Data Review

The first step is conducting an internal import data review. Note entry numbers, dates and the amount of tariffs paid. This process involves gathering all relevant documentation for import entries that were subject to IEEPA tariffs, including:

- Entry summaries on CBP Form 7501

- Commercial invoices

- Payment records for duties and fees

- HTS classifications used at the time of import

Analyze this data to identify entries subject to IEEPA tariffs. During this step, you may uncover discrepancies or classification issues that need to be addressed before you file a claim. For larger organizations, cross-functional collaboration is key to capturing all relevant imports.

Step 2: Using CBP’s CAPE System

CBP’s ACE system is the primary interface for filing refunds and post-summary corrections once you’ve collected the relevant paperwork. Through ACE, businesses can:

- Submit post-summary corrections for eligible entries.

- File protests for entries within the set time frame.

- Track the status of submitted claims.

Businesses unfamiliar with ACE may rely on customs brokers or internal compliance specialists to manage filings. Regardless of who submits the claim, the IOR remains responsible for its accuracy. To file through CAPE, your business should:

- Upload entry data and supporting documentation directly onto the platform.

- Validate classifications and duty amounts using system checks.

- Submit refund requests or corrections tied to specific entry numbers.

- Monitor claim progress through real-time status updates.

CAPE supports bulk submissions, which are useful for businesses managing large volumes of entries. Built-in validation tools help identify inconsistencies before submission, reducing the likelihood of delays.

Step 3: Filing a Claim With CIT

In some cases, administrative remedies aren’t enough. Businesses may need to file a claim with the CIT when:

- Administrative claim deadlines have passed.

- Previous protests were denied.

- Significant refund amounts justify legal action.

Filing with the CIT involves a more formal process, including legal pleadings and adherence to court procedures. While this route can extend timelines, it may be necessary to preserve the right to recover funds. With CIT claims, you’ll face additional statutory limits. These deadlines are often measured from the date of a denied protest or other triggering event. Missing these deadlines can permanently bar recovery, regardless of the claim’s merits.

The earliest deadline for commencing litigation is Feb. 3, 2027, which is two years from the date of the first IEEPA tariff payments.

Critical Timelines and Deadlines You Need to Know

It’s essential to act quickly. Refund opportunities are tied to strict deadlines, and missing them can mean missing out on recovering funds. Key timelines include:

- Protest filing deadlines are typically within 80 days of liquidation.

- Post-summary correction windows are generally limited to a set period after entry.

- Statutory deadlines for filing claims with the CIT.

- Potential government-established deadlines specific to IEEPA refund processes.

The statutes of limitations vary based on the procedural path. To manage this, businesses should map each entry against its applicable deadlines. A proactive approach ensures that no viable claims are lost due to timing constraints. Under 28 U.S.C. § 2636(i), you have a two-year statute of limitations for filing in the CIT under residual jurisdiction. Accrual dates start from the tariff payment date, which may include:

- Feb. 4, 2027, for fentanyl IEEPA tariffs.

- March 4, 2027, for Canada and Mexico IEEPA tariffs.

- April 5, 2027, for reciprocal tariffs.

- Aug. 6, 2027, for Brazil IEEPA tariffs.

- Aug.27, 2027, for India IEEPA tariffs.

Strategically Managing Your Refund

Securing a refund is only part of the opportunity. Managing the financial impact requires careful planning.

You should evaluate how the recovery will affect your business’s current and prior reporting periods. Key tax considerations include:

- Whether refunds are considered taxable income in the year received.

- The need to amend previous tax returns if deductions were previously claimed for tariff expenses.

- The impact on the cost of goods sold and inventory valuation.

- State and local tax treatment, which can differ from federal rules.

- Potential implications for transfer pricing and intercompany transactions.

Reinvestment strategy also plays a key role in maximizing the value of your recovered funds. You may consider allocating capital toward supply chain diversification, technology upgrades or operational expansion.

Maintaining strong trade compliance practices is equally important. This includes regularly reviewing tariff classifications, monitoring regulatory changes and documenting import processes. Strengthened compliance reduces future risk and positions the business to respond quickly to similar opportunities. This process includes:

- Mapping and auditing entries.

- Managing any government contracts.

- Maintaining meticulous records.

- Monitoring future tariffs.

A disciplined approach ensures that refunds are not only recovered but also used to support long-term growth and stability.

Moving Forward With Clarity and Confidence

IEEPA tariff refunds are a good opportunity for eligible importers. The Supreme Court’s decision has opened the door to recovering substantial funds, but success depends on timely and informed action.

By moving quickly, understanding eligibility, identifying affected imports and following the right recovery pathways, your business can position itself to claim what it’s owed. The process demands diligence, but the potential rewards justify this effort.

This story was produced by Polston Tax and reviewed and distributed by Stacker.