How do no preset spending limit credit cards work, and who qualifies?

A no-limit credit card refers to a card with no preset spending limit. These cards offer flexibility by letting your spending power adjust based on factors like income, credit history, and payment behavior.

Unlike traditional credit cards with fixed caps, a no-limit card’s available credit changes over time. While they can make large purchases easier, they also carry risks if your cash flow is inconsistent. Below, Ramp delves deeper into the benefits and drawbacks of these credit cards, their various types, the qualifications for approval, and more.

Note: The cashback percentages, limits, fees, and other figures mentioned in this article are for illustrative purposes only. They do not represent guaranteed or expected rates. Actual terms, credit limits, rewards, and approval criteria vary by card issuer and may change at any time. Readers should verify current details directly with each issuer before applying.

What is a no-limit credit card?

A no-limit credit card doesn’t have a fixed spending cap. Instead, your limit adjusts from month to month based on your credit score, income, and payment history. Consistent spending and on-time payments can increase your limit, while missed payments, lower profitability, or reduced income may shrink it.

The term “no-limit” is also sometimes used to describe cards with exceptionally high limits, such as invitation-only black cards that require steep fees and strong financial profiles.

Types of no-limit credit cards

No-limit cards fall into a few main categories:

- Charge cards: Charge cards don’t have preset limits, but you must pay the full balance each month. Your spending power shifts based on income, credit history, and payment behavior.

- Credit cards with no preset spending limit: These let you carry a balance, unlike charge cards, but your available limit still changes with your payment history, cash flow, and overall credit profile.

- Invitation-only black cards: Often seen as status symbols, these cards come with very high spending power and steep fees. The best-known example is the American Express Centurion Card, which charges a $10,000 initiation fee and a $5,000 annual fee.

How do no-limit credit cards work?

No-limit credit cards don’t have a fixed cap; your spending power changes over time based on how the issuer evaluates your profile. Common factors include:

- Income and cash flow: Higher revenue usually allows more flexibility.

- Credit score and history: Strong credit signals responsible usage and may unlock higher limits.

- Payment history: On-time payments can increase your spending power, while late payments may reduce it.

- Recent usage: Large charges or rapid spending changes can temporarily tighten your limit.

Having no preset limit doesn’t mean you can spend without restrictions. Your available credit adapts to your financial situation. Some cards require payment in full each month (charge cards), while others let you carry a balance.

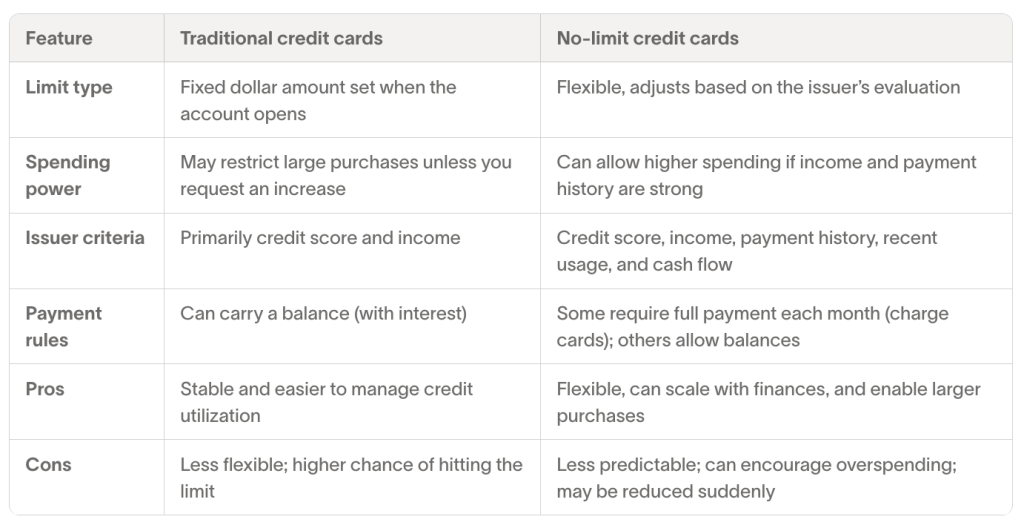

No preset spending limit vs traditional credit limit

Here are the key differences between a traditional credit card and a card without a credit limit:

Pros and cons of no-limit credit cards

No-limit credit cards can offer more flexibility than traditional cards, but they also carry unique risks.

Pros

- Flexibility to make large purchases without rigid limits.

- Potential for higher limits with a strong payment history.

- Protection against rising operational costs.

- Rewards on large purchases, such as cashback, points, or miles.

Cons

- Some cards require payment in full each month; others charge high interest if you carry a balance.

- Variable, undisclosed limits that may change from month to month.

- Higher risk of overspending without a fixed cap.

- Complex fees and often higher annual costs than regular cards.

Who should consider a no-limit credit card?

No-limit credit cards work best for businesses with high or seasonal expenses, especially if you need the flexibility to cover large purchases or frequent business travel. They’re a good fit if you have steady cash flow, disciplined financial habits, and want access to premium rewards tied to higher spending.

They’re less suitable if cash flow is tight, budgeting is a challenge, or you tend to carry balances. Many of these cards require payment in full each month or charge higher fees, which can make them risky if your finances aren’t stable.

How to qualify for a no-limit credit card

Qualifying for a no-limit credit card requires stronger credentials than a standard business credit card. Issuers usually expect excellent personal credit (a FICO Score of 700+), steady business revenue, and a history of paying vendors and creditors on time. They may also weigh your company’s operating history, profitability, and available cash reserves.

To improve your chances, maintain consistent revenue and keep clear financial records that demonstrate cash flow stability. Paying vendors, lenders, and credit accounts on time builds a solid business credit profile. Separating business and personal expenses also strengthens your credibility with issuers.

This story was produced by Ramp and reviewed and distributed by Stacker.