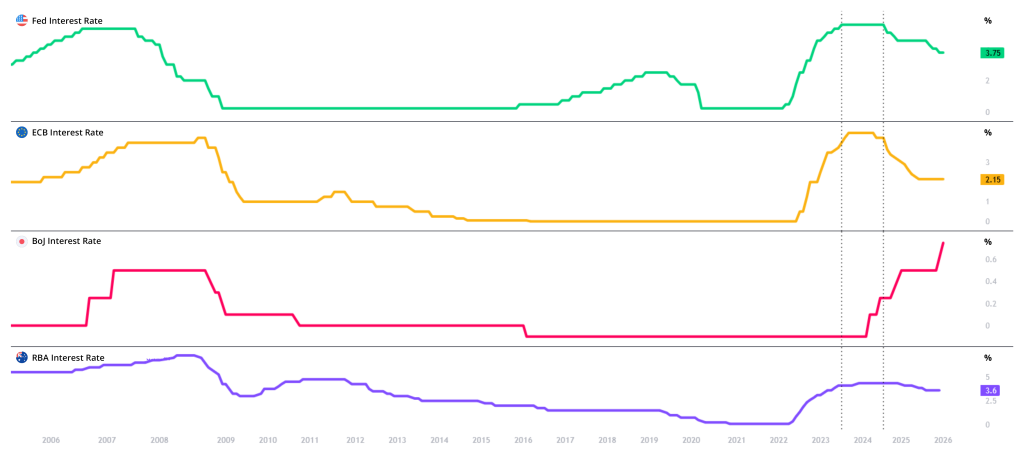

Monetary policy: Why are global central banks moving in different directions?

Four years ago, in 2022, many major world economies faced a similar problem and shared a similar solution. A “perfect storm” of macroeconomic events would see inflation rise to double figures in many world economies for the first time in almost 40 years, leading to a nearly universal decision to raise central bank interest rates to combat pricing pressures.

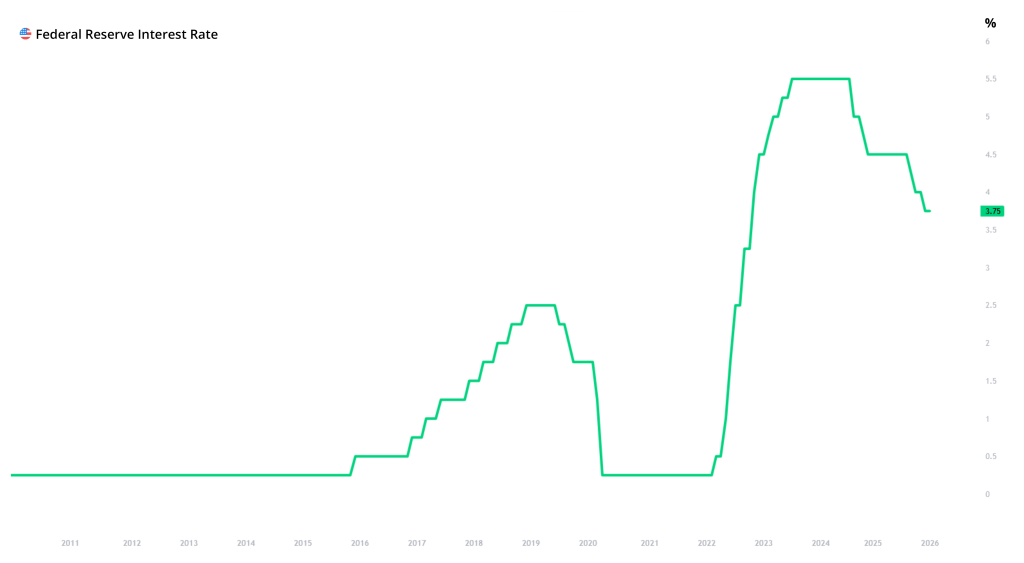

In the case of the Federal Reserve, policy rates would reach a peak of ~5.50%, a level last seen in the aftermath of the dot-com bubble, almost 25 years ago.

In 2026, however, monetary policy stances among central banks are not only noticeably less uniform but actively diverging, with different economies facing unique challenges, unlike years previous.

This is further amplified by the current conflict in the Middle East, with some major world economies more dependent on Middle Eastern crude exports than others, creating a mixed bag of inflationary pressures.

For traders, this divergence isn’t just a news headline. Instead, a dynamic that not only fans the flames of market volatility but also offers a unique macroeconomic angle for finding your next trading opportunity.

In this article, OANDA summarizes the increasingly different monetary policy stances of some major central banks and what this could mean for the average trader.

Key takeaways

- Unlike in previous years, where the focus was primarily to tame inflation, the turn of the year has seen central banks becoming increasingly divergent in monetary policy stance

- Bookmarked by the start of 2026, central banks worldwide are faced with unique economic challenges, with some more hawkish and others dovish

Federal Reserve: A very cautious easing

The most closely followed central bank of all is the Federal Reserve.

Entering 2026, the Federal Reserve has cut rates six times in its current easing cycle, with the target rate currently between 3.50% and 3.75%.

An important distinction, however, is that these six cuts have not been made consecutively. The Federal Reserve chose to maintain rates at 4.25% and 4.50% for most of 2025, adopting a “wait-and-see” approach, and has cut rates in only half of the last 12 decisions.

Its most recent decision, on Jan. 28, would see it continue this strategy, maintaining rates after December’s cut and broadly meeting market expectations.

In maintaining its infamous dual mandate, the Federal Reserve remains in a difficult position, with inflation proving somewhat sticky above the 2.0% target while monthly NFP job growth has slowed considerably to +50,000.

Naturally, the former would support a rate hike, while the latter would support a rate cut, putting the Fed in a “catch-22."

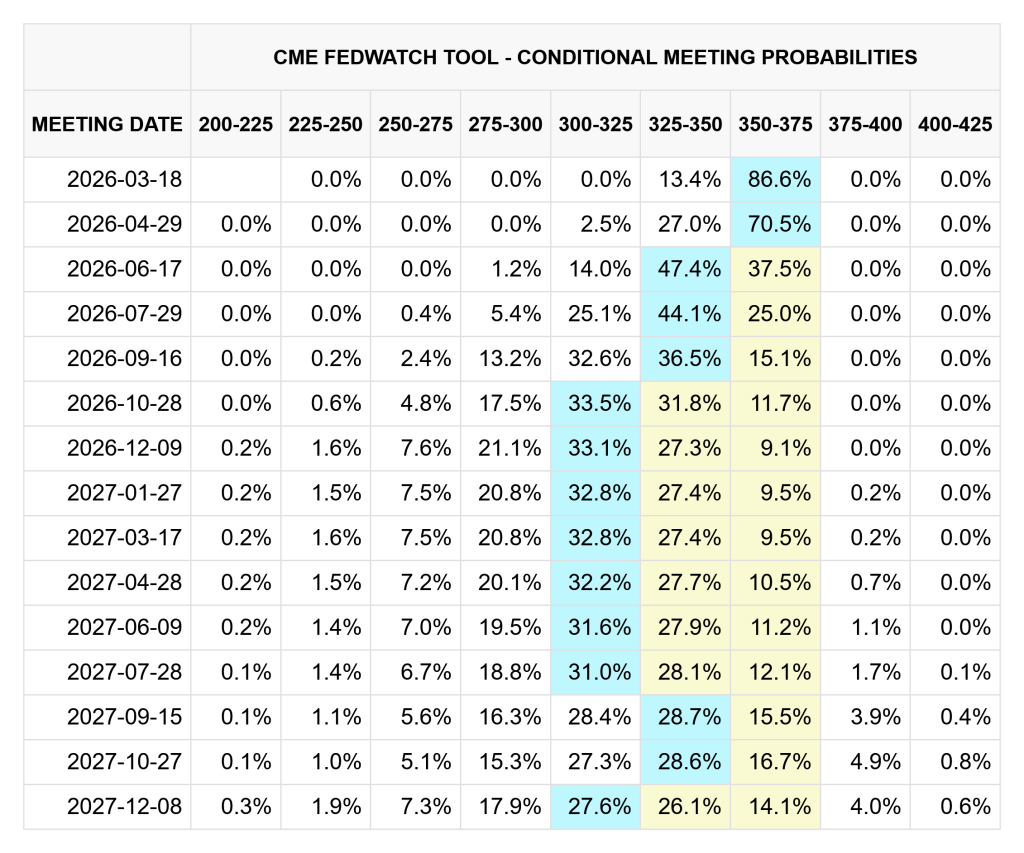

As for 2026, expectations for further Fed rate cuts vary depending on the source.

Not for the first time, markets are generally more optimistic than most policymakers, with the former expecting two 25-basis-point cuts in the remainder of 2026, met by a more conservative single 25-basis-point cut expected by most officials, taking into account recent commentary and current dot plot projections.

Federal Reserve: What you need to know

To conclude this overview, here are a few fundamental themes unique to the Federal Reserve in 2026:

Blurred lines between politics and policy: Since returning to office, Trump has made his preference for lower interest rates clear. While for much of 2025 these demands fell on deaf ears, growing tensions between Powell and Trump have recently led to a criminal investigation by the DoJ into alleged overspending on renovations to the Federal Reserve building.

Depending on your view, this is either a reasonable enquiry into the spending of U.S. tax dollars, or rather a form of political intimidation designed to punish Powell. While the Fed, by law, is intended to be free of any party leanings, recent developments are continuing to blur the lines, with an apparent increase in political instability threatening to undermine confidence in the dollar.

Who will succeed Powell?: To continue in a similar vein, the end of Jerome Powell’s term as Fed Chairman this year, and more importantly, who will replace him, is a significant unknown for the future monetary policy stance of the Federal Reserve.

Gifted the opportunity to install someone more aligned with his demands for interest rates as low as 1%, President Trump has officially nominated Kevin Warsh to succeed Jerome Powell when his term ends this May. While the shortlist previously centered on the “two Kevins and a Rick”—Warsh, Kevin Hassett, and Rick Rieder—the formal selection of Warsh has shifted the market's focus from speculation to confirmation.

When simplified, both Hassett and Rieder were seen as the more dovish candidates, while Warsh has typically been perceived as the most hawkish of the three. However, with the nomination sent to the Senate in early March, the "hawkish" label is being tested, with some suggesting that AI-driven productivity could pave the way for lower rates. For traders, the U.S. dollar now sits at a crossroads: it must balance Warsh’s reputation for a sensible, "sound money" stance with the political pressure for a return to low-interest rates

European Central Bank: Done and dusted

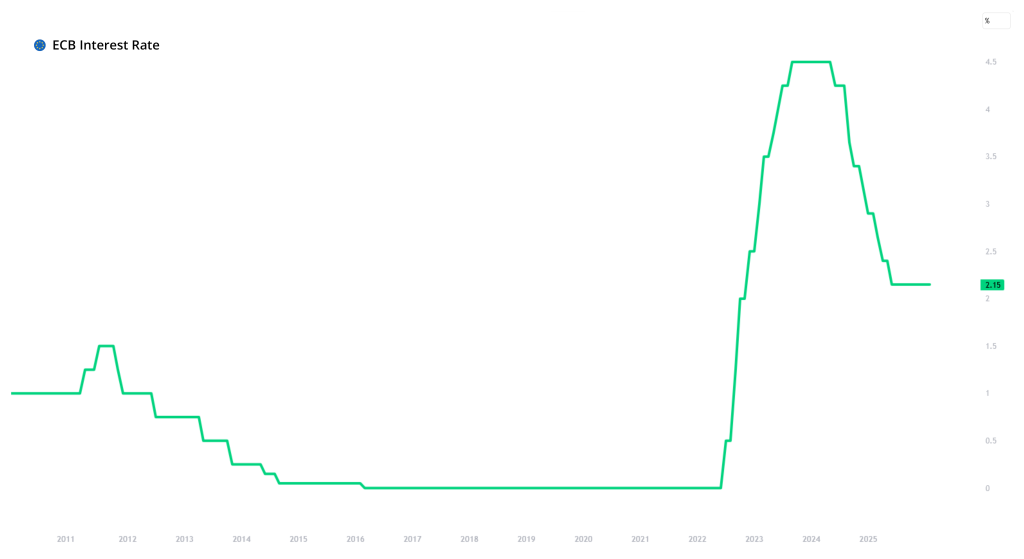

At the turn of the year, the European Central Bank boasts the most “normal” balance sheet amongst its peers, having better navigated inflation back toward the 2% target while, crucially, maintaining stable employment and economic growth.

The ECB currently offers a 2.00% deposit facility rate, unchanged since June 2025, and many see this as the “terminal rate” in the central bank’s easing cycle.

Naturally, this air of apparent fiscal stability in the Eurozone compared to other regions has benefitted the euro, which remains one of the best-performing currencies of 2025.

While this previously came at the envy of President Trump, who also demanded lower rates in the United States to curb government borrowing costs, there are some important distinctions between the EU and U.S. economies.

One of the first to begin cutting, the ECB made eight cuts over 12 months between June 2024 and June 2025, each by 25 basis points, except one, when rates were maintained.

With inflation falling consistently towards the 2.00% target, the ECB was able to cut rapidly when countries like Germany flirted with recession, stimulating economic growth and ultimately bringing rates down to 2.00%.

As for 2026, most predict that the ECB will maintain rates for the foreseeable future, which, when compared to the Federal Reserve, is one of the clearest examples of policy desynchronization.

European Central Bank: What you need to know

Here are some unique talking points for ECB monetary policy in 2026:

German ‘bazooka’ stimulus: Coined the “German bazooka,”, the recent announcement of German fiscal stimulus in infrastructure and defense is expected to offer some upside to EU economic growth early in 2026.

While already holding a relatively lax stance on monetary policy, additional economic growth from similar stimulus may give the ECB a further chance to remain passive, with rate cuts becoming entirely unnecessary.

Questions over EU exports: Compared to other world economies, the Eurozone’s economy is particularly dependent on the physical export of products, unlike others, which are more service-focused.

With the threat of U.S. tariffs recently renewed over Greenland, there could at least be a rationale for further rate cuts if trade relations sour considerably.

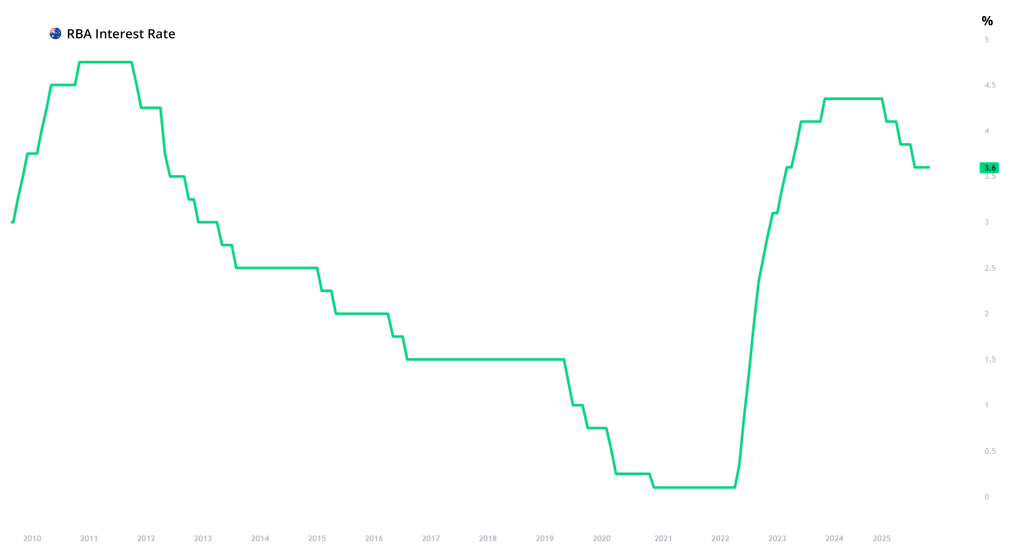

Reserve Bank of Australia: Reluctantly hawkish

Over 9,000 miles away from its European and American counterparts, it would seem that, recently, geographical distance isn’t the only factor separating the RBA from other central banks.

While the RBA currently offers a cash rate of 3.60%, comparable to the Federal Reserve, comparisons start and end here, with most expecting the RBA to raise rates at its upcoming meeting, with inflation continuing to rise well above the target of 2.00%.

While rates have remained steady in Australia since August, the RBA cut rates three times in 2025 to support an otherwise slowing domestic economy, ultimately lowering the cash rate from 4.35% to 3.60%.

While some will level policy error accusations at the RBA, believing that a decision to cut rates too early in 2025 must now be rectified with a “corrective” hike, if nothing else, it reminds markets that there are two sides to the coin when lowering rates.

Looking ahead, ASX interest rate futures suggest a 25-basis-point hike is ~70% likely at the RBA’s upcoming February meeting, with a surprise return to “higher for longer” policy now the general market consensus.

Reserve Bank of Australia: What you need to know

Here are a few talking points to conclude our overview of the RBA:

Energy costs in focus: While the Australian government previously had a rebate system for energy bills, that scheme has now ended, with energy prices surging 21.5% in 2025.

Since households are back to paying full-market rates for power, this would explain the uptick in headline inflation numbers, but not the core readings, which usually exclude volatile energy pricing.

Historically low unemployment: While inflation is becoming increasingly problematic, one feather in the cap of the Australian economy is the unemployment recently falling to 4.1%.

While this keeps wage growth strong, productivity estimates have yet to improve, meaning manufacturers and businesses are passing higher labor costs onto consumers, increasing inflation.

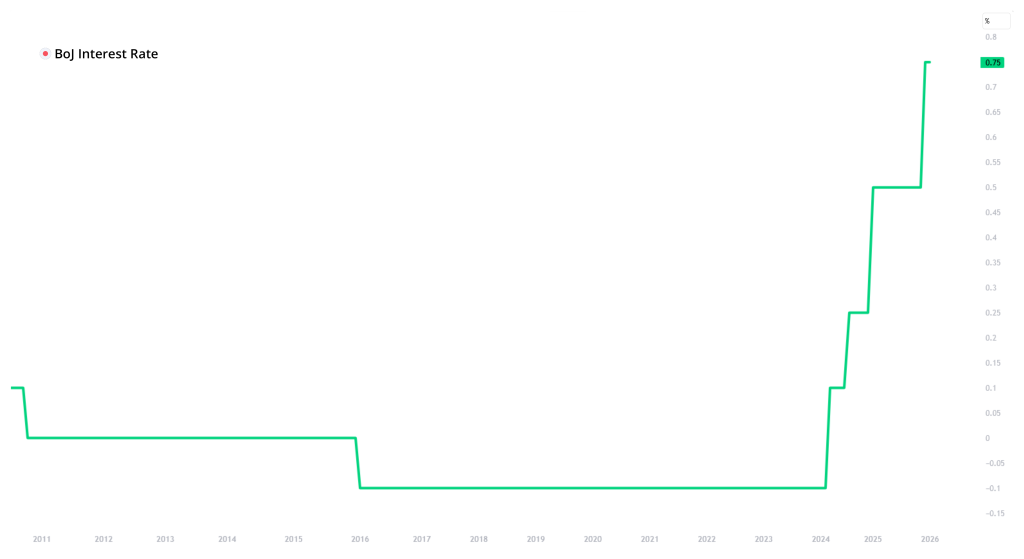

Bank of Japan: Dovish no more

Undergoing a transition away from the eternal dove of years past, the Bank of Japan is perhaps the most hawkish of major central banks globally, entering 2026 with an interest rate of 0.75%.

While, by some metrics, this is a historically low level of interest, the figure represents the highest policy rate set by the Bank of Japan since 1995, after it offered ultralow and even negative interest rates in the interim.

While inflation pressures are lessening in Japan, though artificially suppressed by government energy subsidies, a hawkish stance is also a means to dissuade further yen downside, with the Bank of Japan recently renewing its commitment to “defend” yen pricing.

Despite voting to pause in its January meeting, both Bank of Japan policymaker commentary and general market consensus would currently suggest that two, possibly three, interest rate hikes are on their way in 2026.

Bank of Japan: What you need to know

To round up this section on the Bank of Japan, here are a few unique macroeconomic themes:

Real rates: With a core inflation rate consistently above 2.00% but a policy rate of 0.75%, Governor Ueda has recently commented on the notion of real rates and how, with inflation factored in, interest rates on each yen are still negative.

This makes some headroom for further rate increases by the Bank of Japan, which has gone on record saying it has “no choice” but to raise rates closer to a “neutral” level.

Core inflation in focus: While inflation is cooling somewhat in Japan, the Bank of Japan remains fixated on core inflation rather than headline numbers, especially given the government's artificial suppression of energy prices.

Importantly, core inflation numbers are expected to remain above the 2.0% target in Japan until 2027, adding a further hawkish tilt to BoJ monetary policy for the foreseeable future.

Monetary policy desync: Wrap-up

Here is a summary of each central bank mentioned and see how they are becoming increasingly divergent:

- Federal Reserve: In a cautious easing cycle, with most currently expecting either one or two rate cuts in 2026

- ECB: Maintaining rates at 2.00%, with most currently expecting rates to remain unchanged in 2026

- RBA: Likely to perform a “corrective” hike in the upcoming decision, with most currently expecting rates to be maintained higher for 2026

- Bank of Japan: In a tightening cycle, with most currently expecting two or three interest rate hikes in 2026

Monetary policy desync: What does this mean for traders?

To conclude, here are a few examples of how this era of policy divergence could provide another layer for your fundamental analysis when looking for trading opportunities in 2026:

- Unwinding of the carry trade: For years, markets have borrowed yen cheaply to fund investments in other markets and buy other currencies. With the BoJ offering rock-bottom interest rates for the best part of a decade, this would all but guarantee a gradual slide in the yen’s value versus its peers. In 2026, however, things are different. With the Bank of Japan now more hawkish than at any time in recent memory and positioned for multiple rate hikes this year, this spells trouble for the infamous carry trade.

If nothing else, there could be some volatility from yen markets in 2026 as its role on the global FX stage continues to shift. - AUD yield play: Given the above-mentioned inflation in the Australian economy, a hawkish tilt from the RBA might attract those looking to optimize investment yields, offering higher interest rates than most currently. In a vacuum, higher interest rates would encourage markets to buy the Australian dollar, especially against currencies whose central banks are expected to either maintain rates lower or make further reductions.

- U.S. dollar unknowns: While, of recent, there is never a dull moment for U.S. dollar markets, 2026 is an important year for Federal Reserve monetary policy, which could affect the dollar in a multitude of ways. Having suffered a poor performance in 2025, the dollar’s role as “world currency” means that much of market volatility, for better or worse, originates from movements in the U.S. dollar.

Granted, the above are only three of many possible examples, but it would certainly seem that 2026 will be an interesting year for traders.

This story was produced by OANDA and reviewed and distributed by Stacker.