Retail supply chains brace for a redefined 2026 as tariffs, technology gaps, and nearshoring upend old models

A new survey of 250 retail supply chain leaders reveals a sector undergoing one of the fastest strategic shifts in decades. Between rising tariffs, geopolitical pressures, and surging consumer expectations, organizations are being forced to rebuild their logistics networks for resilience rather than speed. The study, commissioned by WSI | Kase and conducted by TrendCandy, highlights an industry rethinking everything from supplier geography to warehouse placement heading into 2026.

According to the report, Retail Supply Chain Moves That Will Define 2026, many retailers are accelerating their nearshoring and regionalization efforts. The motivation is not just cost pressure, but a heightened need for control, stability, and agility.

To mitigate risk, 77% of supply chain leaders have already shifted sourcing away from China toward tariff-neutral countries, and 87% are increasing buffer inventory to hedge against volatility. These moves signal a decisive break from pre-COVID-19 pandemic supply chain models built around global consolidation and just-in-time fulfillment.

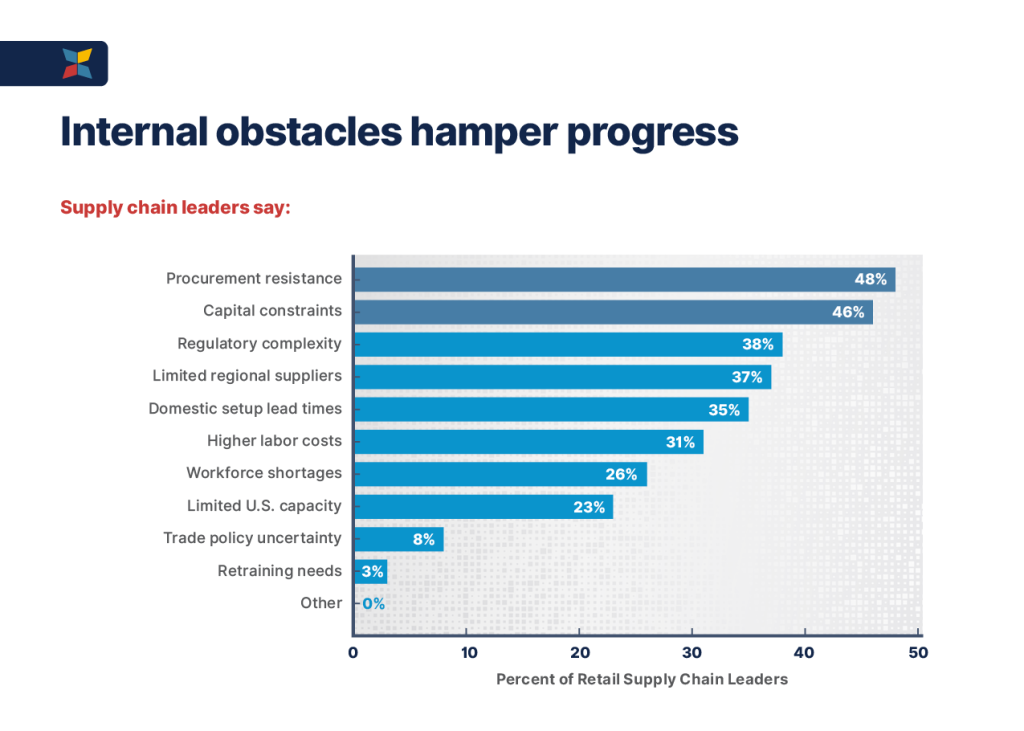

While global trade volatility continues to reshape strategies, the survey shows that internal challenges, such as capital constraints, technology misalignment, and organizational inertia, may prove equally disruptive in the year ahead.

“Retail supply chains are being reshaped in real time,” the report’s authors note. “Leaders are no longer treating nearshoring or diversification as experimental; they’re becoming strategic imperatives.”

A sector under pressure: Tariffs accelerate change

Three-quarters of retail supply chain leaders say tariff turbulence is redefining their 2026 strategies, prompting a widespread pivot toward regionalization and supplier diversification. Ninety-three percent are now prioritizing diversification within Asia to reduce tariff exposure, and many are replacing single-country dependency with layered sourcing networks that blend domestic, nearshore, and diversified sourcing models.

The loss of Section 321 de minimis exemptions is also creating upheaval, raising landed costs for small parcels and pushing brands to revisit cross-border ecommerce strategies and fulfillment models.

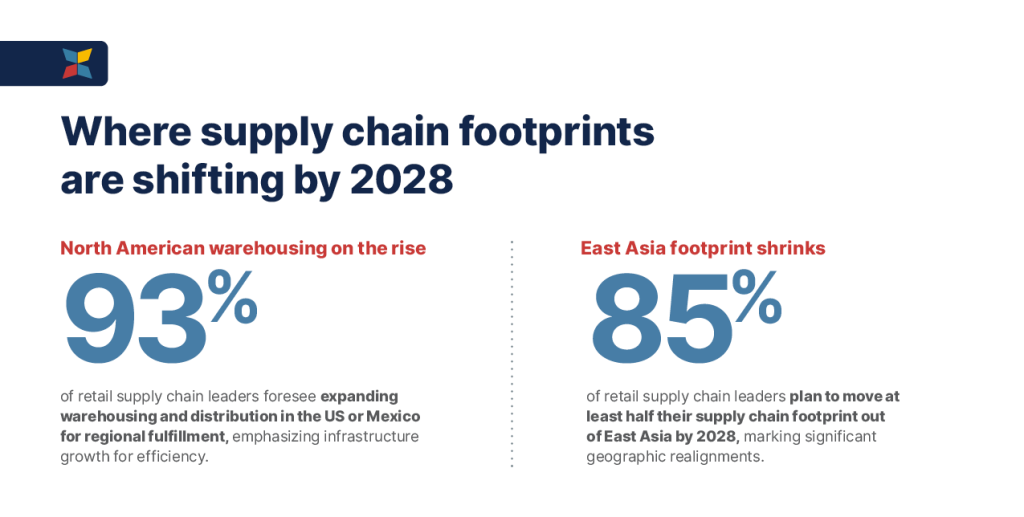

Nearshoring momentum builds, but readiness lags

While interest in nearshoring has surged, only a small share of leaders say their networks are fully equipped for regional fulfillment. The momentum is geared toward North American and hemispheric supply networks: 87% of leaders say they are planning nearshoring pilots in Mexico or Central America within the next 24 months, signaling that regional experimentation is already underway. Even so, few describe themselves as fully ready for a regional model due to infrastructure constraints, internal resistance, and limited capital.

Top motivations for nearshoring and reshoring include faster delivery, greater quality control, and improved customer trust; all signals that retailers see proximity as key to long-term resilience. But execution maturity has not yet caught up with strategic intent.

Technology misalignment is becoming a critical vulnerability

Even as more of the supply chain invests in technology, logistics ecosystems remain fragmented. The survey shows 84% of retail supply chain leaders struggle to align IT infrastructure for multinode fulfillment, bringing attention to how difficult it is to connect OMS, WMS, TMS, and carrier systems in a real-time, data-driven environment.

Visibility is now emerging as a top concern: 88% say transparency into supply chain changes is essential to strengthening customer loyalty, highlighting a widening gap between the experience consumers expect and the systems retailers rely on.

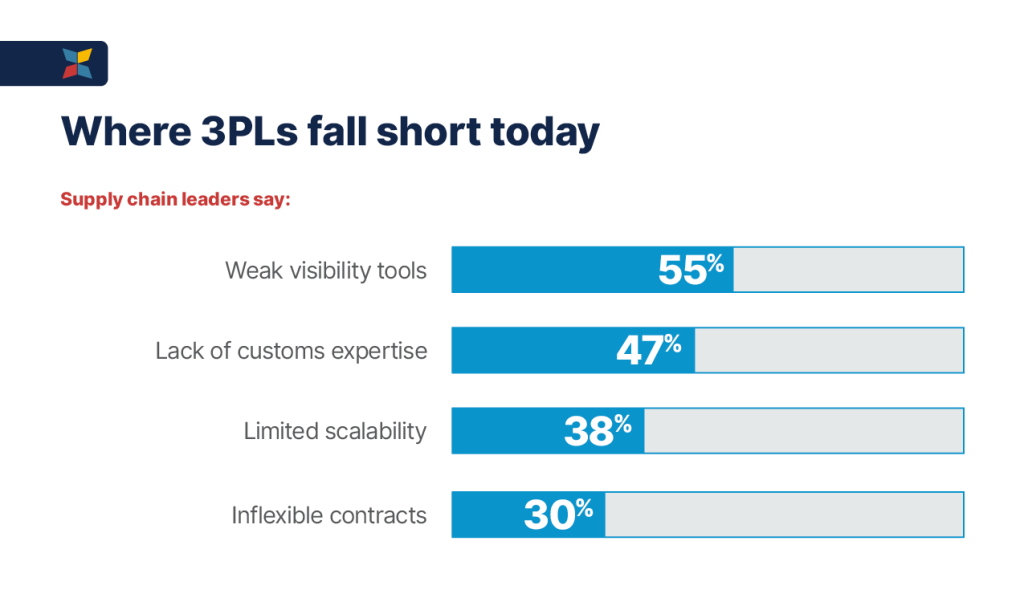

Brands seek more from their 3PLs as partnerships enter a redefinition phase

The survey reveals a sector on the verge of major partner realignment. Eighty-four percent of leaders expect to restructure their 3PL partnerships by 2026, even though only 58% feel confident their current providers can support required strategy shifts.

As retailers accelerate nearshoring and regional fulfillment efforts, the next two years are emerging as a decisive transition period, one where logistics providers will be reevaluated based on adaptability, regional capability, and technology integration.

Infrastructure expansion is underway, but investment hurdles slow progress

Retailers overwhelmingly prioritize North American warehousing, regional distribution, and flexible multinode networks. However, many note that capital constraints and procurement delays are stalling urgently needed expansions.

Though goals are clear, execution is uneven, especially for brands attempting to move from global to hybrid or nearshore-regional sourcing models.

Operational reliability emerges as the new benchmark for success

Although growth remains important, retailers say operational reliability is now the defining metric for success in 2026. Supply chain leaders are focusing on:

- On-time delivery

- Perfect order fulfillment

- Inventory accuracy

- Real-time visibility

Many also admit they lack detailed contingency plans for tariff shocks, supplier failures, or transportation disruptions, introducing operational fragility during a high-risk planning cycle.

A defining year ahead

The key takeaway from the 2026 outlook: The businesses best positioned for next year will be those that invest early, modernize infrastructure, prioritize transparency, and partner with logistics providers capable of scaling across regions.

As tariff landscapes shift, fulfillment costs rise, and consumer expectations tighten, the report concludes that retail’s next era will be defined not by speed, but by resilience, visibility, and control.

This story was produced by Kase and reviewed and distributed by Stacker.