With rising debt comes rising costs: The rise of global yields

Despite central banks influencing the direction of long-term yields, they are, for the most part, market-sensitive, OANDA reports. Even during the Trump Administration’s push for rapid Federal Reserve rate cuts, long-term rates remained stubbornly high, which kept borrowing costs elevated for consumers.

Key takeaways:

- Since 2020, bond yields have surged amid historic volatility — the once “safe” market now drives global risk sentiment.

- Years of Quantitative Easing (QE) and cheap money inflated growth but stored fiscal risks that are now unwinding through higher yields.

- The post-COVID-19 inflation spike and relentless government spending broke the old norm — yields stay high even as inflation cools.

- Long-term yields continue to climb amid strong economies, tariff risks, and loose fiscal policy, despite expected rate cuts.

- With a low appetite for government obligations, investors are shifting to metals, crypto, and other inflation-resistant assets, which creates high volatility for currency markets.

An unusual government bond market

Since 2020, the bond market, traditionally seen as the safest and most liquid market, has experienced unprecedented dynamics. This, in turn, creates an unforeseen environment for government yields (at least compared to recent times).

Many factors are responsible: Quantitative Easing (QE) from the post-Great Financial Crisis (2007-2009) and COVID-19 period, the consequent tightening from central banks, and governments' spending habits.

From 2008 to 2021, low inflation and a somewhat sluggish global economy required easy monetary conditions to stimulate job creation and every other positive aspect that a more efficient labor force creates (including the quintessential credit creation). This translates to a need for lower yields across the entire interest-rate curve, which in turn entices lower mortgage rates for consumers.

Why is inflation linked to yields?

Inflation is closely tied to government bond yields; with slowing inflation, longer-run yields have been held between 0% (or even negative) and 2% for most economies throughout that same period.

This phenomenon, combined with central banks buying their own governmental bonds (aka the QE) — which pushed the yields down further — allowed governments to subsidize companies and programs to boost the economy, using what is commonly called "cheap money creation."

One could debate that it brought broadly negative consequences, but without it, the COVID-19 era would have led to a decade-long recovery process and a much bigger economic crisis.

However, as the economy quickly recovered from the COVID-19 crisis, inflation rose sharply (close to 10% year-over-year) in the U.S., Canada, Europe, and worldwide.

This caused bond yields to shoot higher, correlating with rising inflation expectations and forcing central banks to hike interest rates aggressively from 2022 to 2023.

So, what is the current situation?

In an ideal world, government spending would slow as fast as economic recovery is completed.

However, a too-indebted global economy has become addicted to borrowing, and governments are having a tough time slowing down their hunger for debt.

That forces high-spending governments to spend even more to finance their increasing debts — much like an individual taking on a second, higher-interest mortgage simply to cover payments on the first.

Throughout the entire first half of 2025, President Trump complained, often daily, about the higher interest costs of the U.S. government. He lobbied Federal Reserve Chair Powell to lower rates to reduce these costs — but doing so in a high-inflation, tariff environment could have greatly raised longer-run inflation expectations.

With decreasing inflation, government yields should traditionally be heading down — but after 20 years of extremely low yields, this correlation is inverting.

With a sufficient explanation of the situation, here are a few charts that paint the current picture.

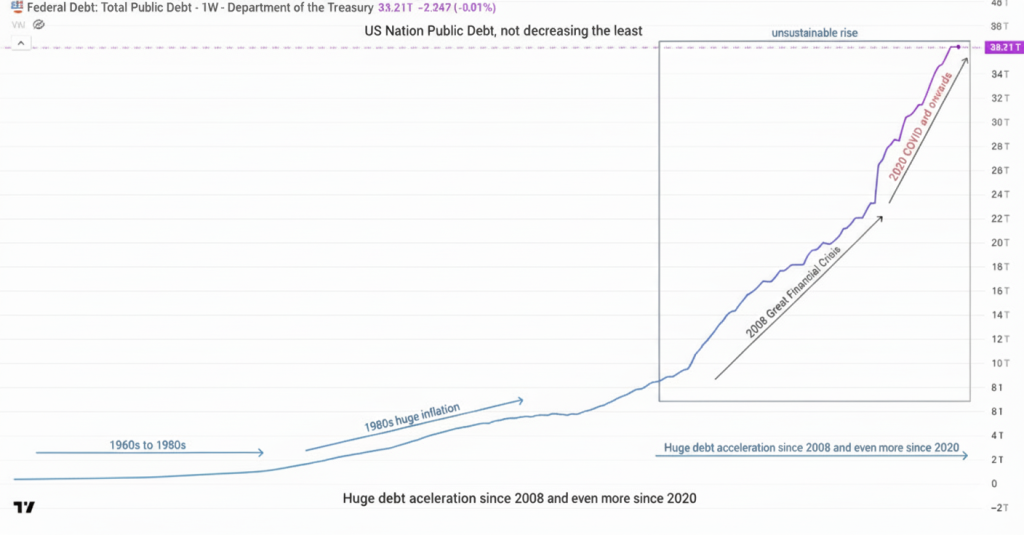

1. U.S. government debt since 1960

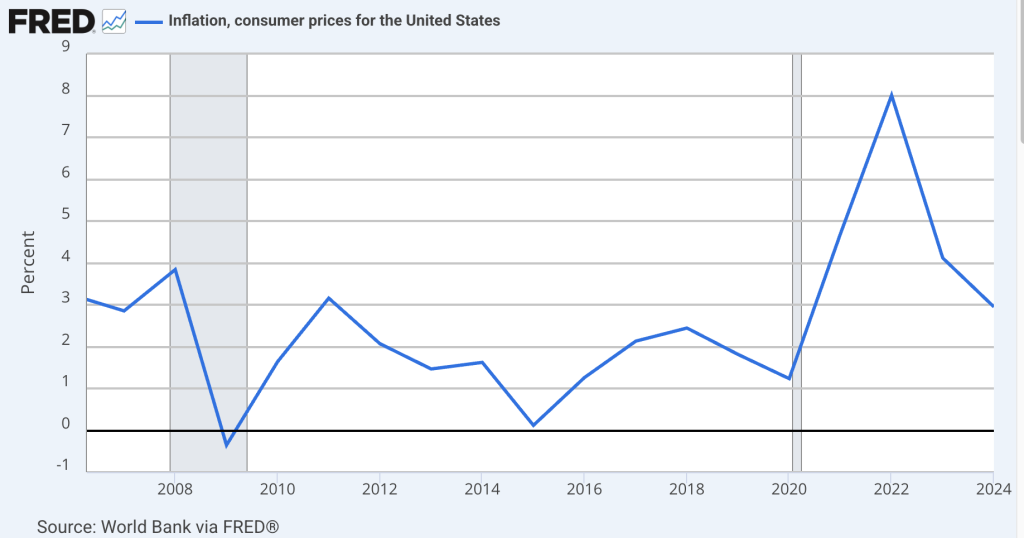

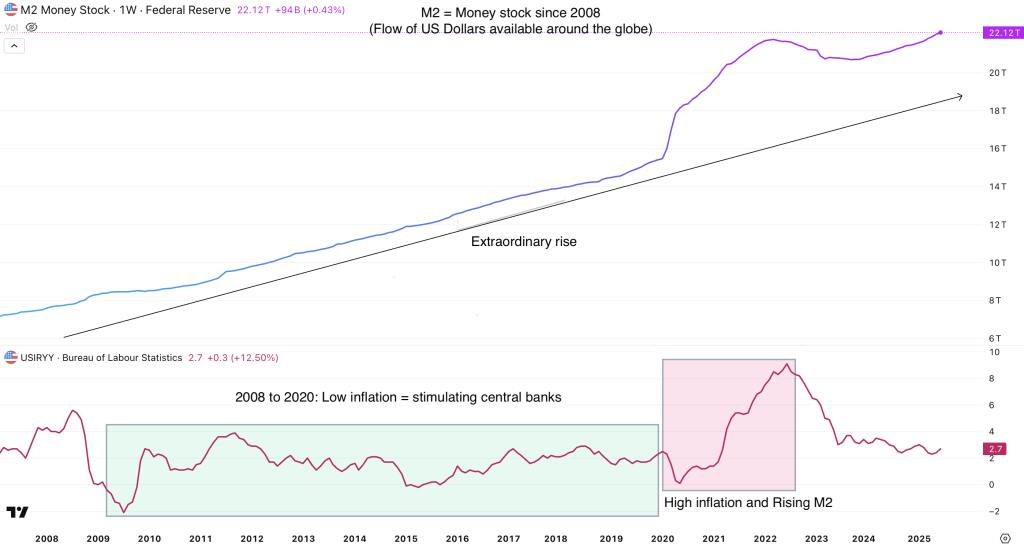

2. U.S. inflation and global money creation (M2) since 2008

To understand the chart above, it’s important to note that money creation makes M2 rise, which props up inflation (more money for the same amount of goods = price of goods rises).

When governments spend, they print money (or create more), which drives inflation.

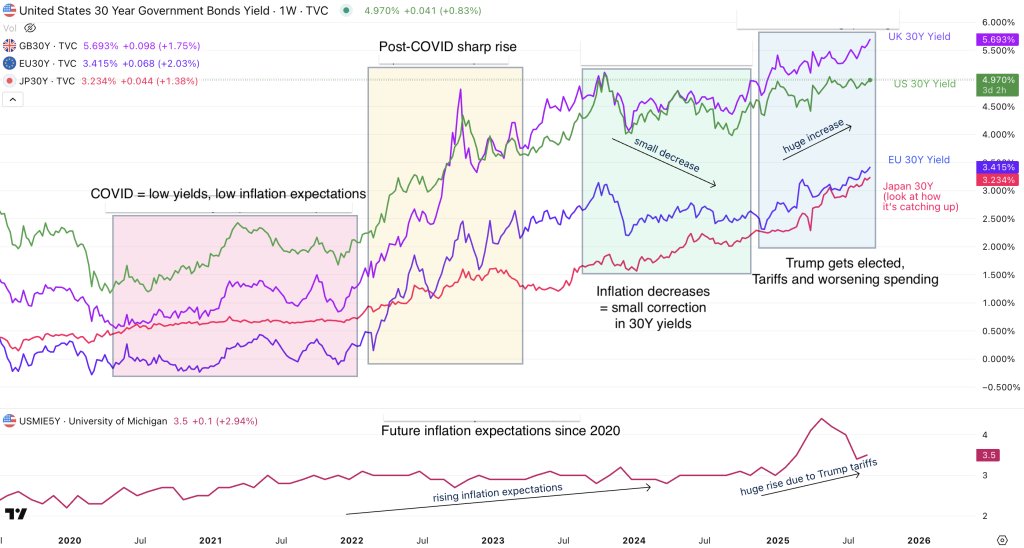

3. Long-run bond yields (30Y) from 2020 to 2025 (U.S., Europe, Japan, and U.K.) and long-run inflation expectations

The Federal Reserve and other central banks are cutting their interest rates and 30Y yields are shooting higher, but why?

So, why is inflation heading lower, but government bond yields are rising?

The reason is simple: Short-term interest rates move with central banks' main rate expectations, and this is closely linked to immediate inflation (like headline CPI, for example).

However, 10Y yields and onwards (which are the base of all consumer mortgages) are more influenced by future (long-run) inflation expectations, future costs of government debt and credit creation (heavier credit = higher yields).

These go up from looser fiscal policies (like the Big, Beautiful Bill from the Trump Administration), government turmoil like in the United Kingdom or France, and a decreasing investor confidence.

A higher credit risk demands higher compensation.

These three components are trending higher, hence, government bond yields are rising, with the latest case in the U.K., with pressure spreading to higher yields in the U.S. and even in Japan — where the 30-year yield recently reached multi-decade highs.

Why are central bankers and governments so scared of tariffs?

Also, tariffs increase inflation, which pushes yields higher.

Independent central banks (particularly the Federal Reserve, which manages the flow of the U.S. dollar, the global reserve currency) are more than essential to preserve the value of money, which helps to reduce inflation further and maintains the value of everyone's precious fiat money. Potentially, governments slowing down their spending would be helpful in this situation.

All of these dynamics contribute sharply to diversification towards metals, cryptocurrencies, and other asset classes that have seen spectacular rallies in 2025.

How does this affect currency markets?

Isolated moves in yields, particularly sudden rises, tend to harm currency demand.

One of the most concrete examples of this effect is the Liz Truss mini-budget catastrophe in the United Kingdom in 2022.

Markets did not welcome a proposal for additional tax cuts while the British government was expected to reduce its deficit. Maintaining high borrowings and lowering income (through taxes) is not optimal for a government's balance sheet and usually leads to higher yields and a lower currency.

A government spending uncertainty directly decreases the demand for its currency.

However, when most government yields rise at the same time, participants try to look for alternatives in countries with tight fiscal policies and a strong reputation:

In 2025, the Swiss franc was particularly sought due to a more stable yield curve and low inflation, leading to 14-year lows in USD/CHF and all-time highs against the Japanese yen.

Government yields’ historic volatility since 2020 reflects a structural breakdown. Years of QE and spending addiction created cheap money conditions, but post-COVID-19 inflation and persistent government spending are keeping yields elevated despite cooling goods prices. Governments are trapped borrowing at higher costs while political pressure threatens central bank independence, fueling diversification into equities, metals, and crypto.

This entire cycle created the conditions of the market as we know it today.

This article is for general information purposes only, not to be considered a recommendation or financial advice. Past performance is not indicative of future results. It is not investment advice or a solution to buy or sell instruments.

Opinions are the authors; not necessarily those of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors.

OANDA CORPORATION IS A MEMBER OF NFA AND IS SUBJECT TO NFA'S REGULATORY OVERSIGHT AND EXAMINATIONS. HOWEVER, YOU SHOULD BE AWARE THAT NFA DOES NOT HAVE REGULATORY OVERSIGHT AUTHORITY OVER UNDERLYING OR SPOT VIRTUAL CURRENCY PRODUCTS OR TRANSACTIONS OR VIRTUAL CURRENCY EXCHANGES, CUSTODIANS OR MARKETS.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. OANDA Corporation is not party to any transactions in digital assets and does not custody digital assets on your behalf. All digital asset transactions occur on the Paxos Trust Company exchange. Any positions in digital assets are custodied solely with Paxos and held in an account in your name outside of OANDA Corporation. Digital assets held with Paxos are not protected by SIPC. Paxos is not an NFA member and is not subject to the NFA’s regulatory oversight and examinations.

Leveraged trading in foreign currency contracts or other off-exchange products on margin carries a high level of risk and is not suitable for everyone. We advise you to carefully consider whether trading is appropriate for you in light of your personal circumstances. You may lose more than you invest. We recommend that you seek independent financial advice and ensure you fully understand the risks involved before trading. Trading through an online platform carries additional risks. Losses can exceed deposits.

This story was produced by OANDA and reviewed and distributed by Stacker.