The cost of waiting to talk about senior care

For many families, senior care planning is something they intend to discuss “one day.” Meaningful planning involves thinking through long-term care goals, understanding financial considerations, and having a series of open, ongoing conversations with loved ones. Yet when life feels stable enough, or a parent seems mostly independent, bringing up long-term care can feel uncomfortable or premature, and it’s easy to delay discussions.

Some families avoid the topic altogether until a crisis occurs. Parents may hide a dementia diagnosis from loved ones for years, believing they can continue providing care at home. Families living far from aging parents may notice small changes during visits that may not reveal the full picture. Without a plan in place, the result can be years of stress and difficult decisions.

While early planning doesn’t eliminate every challenge, it does give families room to compare options and make choices that truly support a loved one’s well-being. By understanding the financial implications of waiting to plan for senior care — and the opportunities that come with preparing sooner — families can approach care decisions deliberately instead of reactively. And when the unexpected happens, that preparation can make the difference between a manageable transition and a costly crisis.

Key insights

- Family expectations about senior care are often unrealistic — especially regarding timing and costs.

- Delaying long-term care planning can be risky, often resulting in higher costs, fewer options to choose from, and increased stress for the whole family.

- Start talking about finances and care options early to avoid surprises and help ensure a senior’s resources align with their goals.

- Invite your aging loved one to share what matters most to them. Simple, respectful questions paired with support from siblings, a neutral third party, and community resources can open the door to productive conversations.

Senior care planning: Expectations vs. reality

Expectations about when a loved one will need care and how much that care will cost don’t usually match reality. This mismatch often results in rushed decisions and added financial and emotional stress.

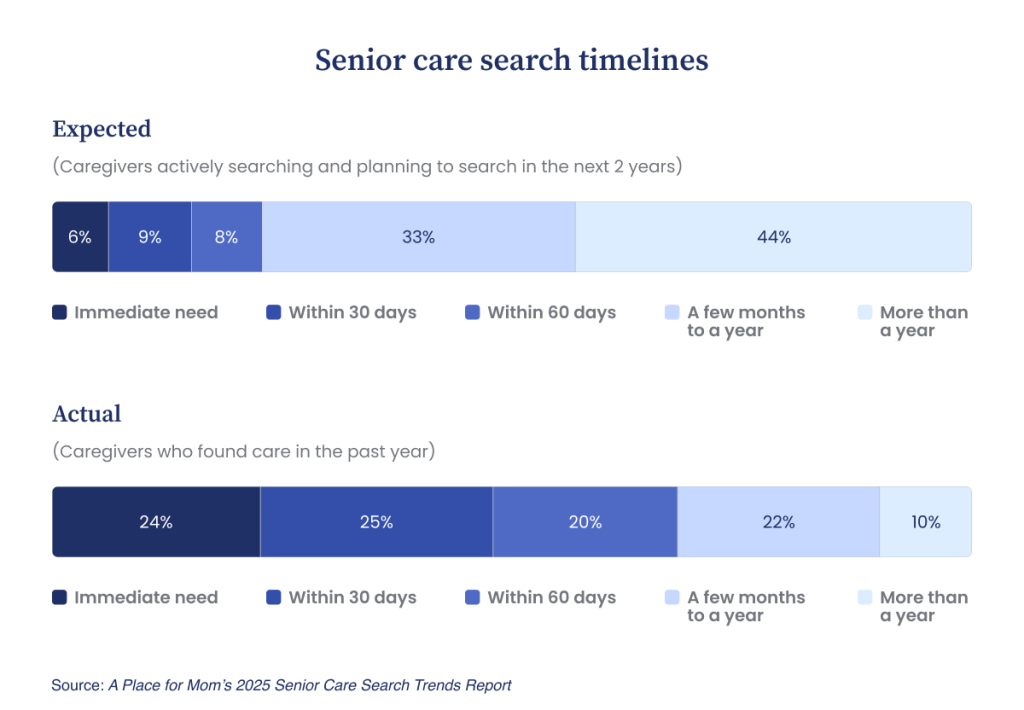

How long families think they have vs. reality

According to A Place for Mom’s 2025 Senior Care Search Trends Report, more than three-quarters (77%) of family caregivers who haven’t begun their search (or are just starting) assume they’ll have anywhere from a few months to more than a year before they need to find professional care. In reality, 69% of caregivers end up hiring in-home care or moving a loved one to a senior living community within 60 days.

Like so many caregivers, families often scramble to find solutions after a fall or health crisis reveals the extent of a loved one’s decline. Some move aging parents into their homes, partly because they haven’t had time to launch a search for professional care.

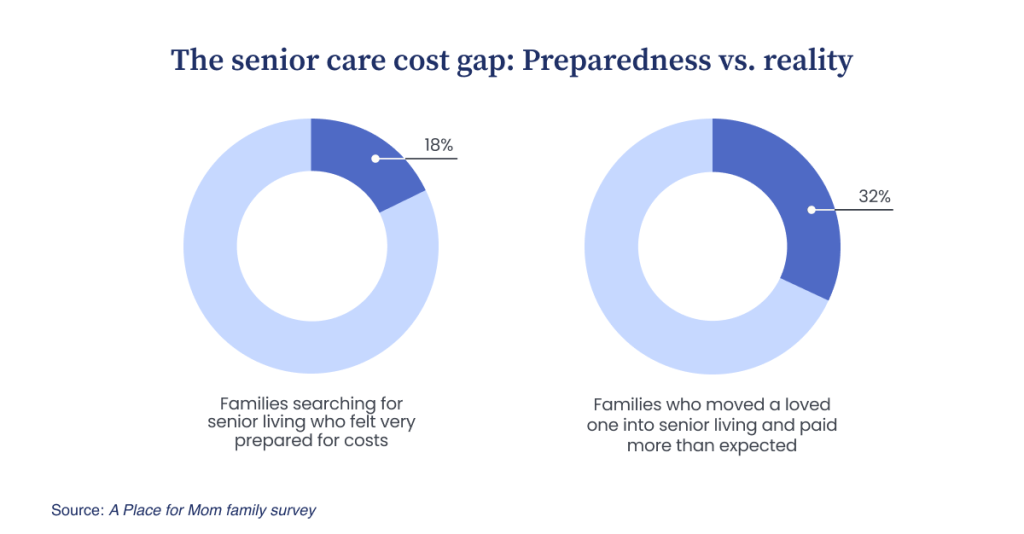

What families expect to pay vs. actual costs

A survey conducted by A Place for Mom found that only 18% of people seeking help with senior living felt they had a good understanding of the costs, and nearly one-third of respondents whose loved one moved into a senior living community said the cost of care was higher than expected.

Just as families misjudge the length of time before their loved one needs care, many also underestimate the cost of professional senior care. This gap may exist, in part, because many families begin their search during a crisis, leaving little time to understand fees, pricing structures, and the financial implications of different care settings.

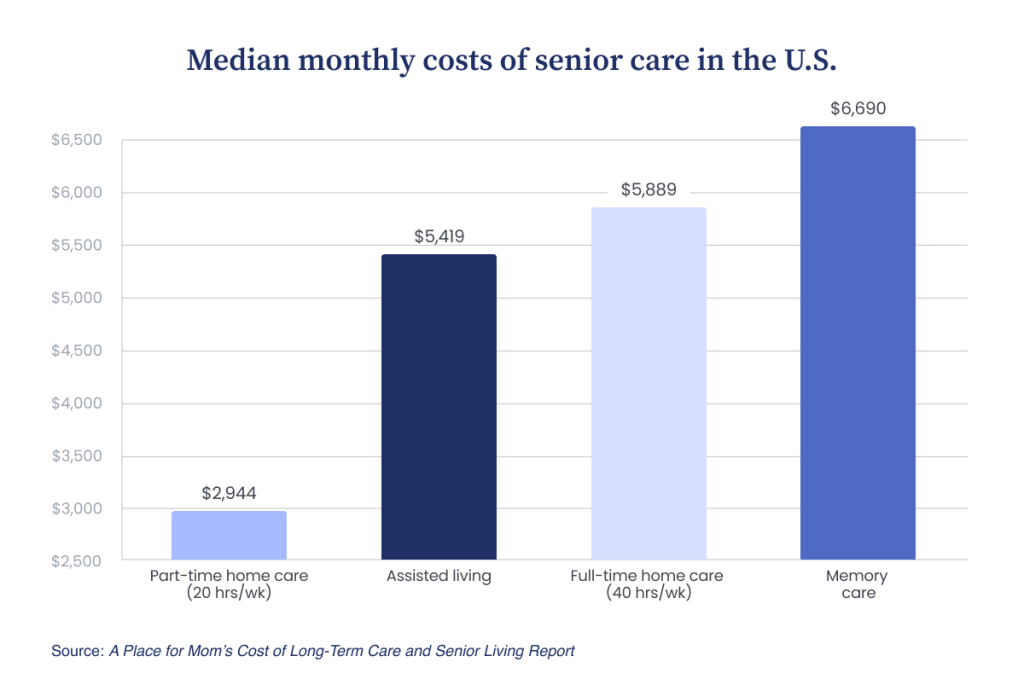

High costs are the leading cause of concern among families seeking both senior living (64%) and home care (72%). The median monthly cost of assisted living in the U.S. is $5,419, which adds up to more than $65,000 annually. Families seeking more specialized support for a loved one with dementia can expect even higher costs. The national median cost of a memory care community is $6,690 per month (roughly $80,280 annually).

Some families face the challenge of both finding and funding care when a loved one’s care needs increase. Many seniors would prefer to age in place in their own homes or live with family. While hourly scheduling and rates can make hiring professional support at home seem more economical, that isn’t always the case in the long term.

“Families may expect to pay less for home care than a senior living setting,” notes Vicki Demirozu, a 30-year veteran of the home care industry, “but costs can rise quickly as their loved one needs more hours of care or more highly skilled care.”

The national median starting rate for nonmedical home care services is $34 per hour. At that rate, a typical care schedule of 20 hours per week costs around $2,944 per month, or $35,330 annually. If a senior needs full-time care (roughly 40 hours of home care per week), they can expect to pay around $5,889 per month or $70,666 a year.

Financial risks families face when they wait to talk about senior care

Delaying senior care planning conversations carries both immediate and long-term financial risks that can often compound. When families must make rushed care decisions, they can unintentionally put their loved one’s financial stability — and their own — at risk.

Loss of financial planning opportunities

Many financial tools that can help cover the cost of senior care require advance planning. For example, long-term care insurance can offset thousands of dollars in future care expenses. According to the American Association of Long-Term Care Insurance, policies are most affordable and accessible when an applicant is still in good health, ideally in their mid-50s. Seniors who wait to apply may be declined coverage due to their age or health status. Even if an older adult can purchase a policy later in life, the premiums may be too high to afford long term.

While long-term care insurance isn’t right for everyone, conversations about care needs and costs can help families consider all their options. Patrick Johnson, CLU, AEP, CLTC, an independent agent who specializes in financial planning for older adults, emphasizes starting early.

“There are so many good products out there now beyond traditional long-term care insurance, including life insurance and long-term care policy combinations, or annuities with long-term care riders,” Johnson notes. “However, families who wait until there are care needs aren’t able to take advantage of these.”

Consider this:

Early planning preserves access to a wider range of financial tools to help fund care — such as hybrid insurance products and annuities with long-term care benefits. Once health needs become more complex, these options may not be available.

Higher costs for senior care

The financial consequences of acting late also appear in the care market itself. Families seeking a senior living community on short notice may encounter higher deposits, higher monthly rates, or fewer opportunities to take advantage of promotions or discounted move-in periods. Researching and planning a senior living transition typically gives families time to tour and compare communities, gather detailed pricing information, and schedule a move that minimizes overlapping housing costs. Without preparation or support, a family looking for care during a crisis rarely has that luxury.

Finding home care in a short time frame presents its own challenges. Families who have been providing care themselves often underestimate the cost of bringing in professional caregivers and how many hours of support a loved one will need. Seeking help for a senior who wants to remain at home on short notice can also mean making urgent and costly home modifications such as installing ramps, grab bars, and other necessary safety equipment.

Rushed liquidation of assets

A fall, sudden hospitalization, or serious illness can force families to find immediate care. Under that pressure, they may make decisions that feel necessary in the moment but carry long-term financial repercussions. Homes are sold quickly rather than strategically. Investment accounts are tapped without time to understand tax consequences. Assets that once offered security and growth become the first casualties of an unplanned transition into care.

And when savings, investments, or property must be converted to cash quickly, the ripple effects can reach the next generation. As Chris Orestis, CSA, president of Retirement Genius, explains, “Along with the capital gains tax burden of liquidating financial assets, families in a rush to finance care may be forced to sell a family home. This means less wealth to pass down to the next generation.”

Delays or ineligibility for benefits

Delaying conversations and planning can also affect eligibility for and the timely receipt of certain federal benefits.

For instance, Medicaid remains one of the most important payment methods for seniors who need but can’t afford long-term care. Yet many families aren’t aware that there are strict and complex financial eligibility requirements to qualify for coverage. In addition to meeting income and asset limits, a five-year look-back period applies in most states. This look-back is a close review of all financial transactions made during the five-year period immediately preceding a senior’s application for Medicaid. It’s designed to ensure large assets that could have been used to pay for their care haven’t been gifted or sold below market value just to qualify. Families who make last-minute financial moves, such as transferring a home or consolidating accounts, may trigger a costly penalty period of ineligibility for Medicaid. During this time, the senior and their family will have to find other ways of covering care costs.

Veterans benefits are another example. While there are many different benefits available to veterans and their families through the U.S. Department of Veterans Affairs (VA), lengthy application and determination processes are common. The Aid and Attendance benefit is a monthly payment available to eligible wartime veterans and their surviving spouses who meet financial criteria and require assistance with activities of daily living. This benefit is often used to help pay for senior care services at home or in a senior living community. The full application with supporting documents can easily grow to 30+ pages. It includes detailed financial reporting like what’s required for Medicaid, although the look-back period is only three years.

Suzette Graham is the founder and CEO of Patriot Angels, a company that helps wartime veterans and their families access VA benefits, with a focus on the Aid and Attendance benefit. She notes that family members can be very helpful in gathering the extensive documentation required and helping their loved one complete the application accurately to avoid delays.

“Approval can take anywhere from 30 to 90 days, so families who wait until a crisis often forfeit benefits during those early months of care,” says Graham.

Consider this:

Learning about available VA benefits early — and preparing documentation in advance — can help families access valuable financial support when a loved one needs care.

For families who want to preserve options, safeguard their financial resources, and honor a senior’s wishes, conversations that feel difficult today may prove to be their most important source of stability down the road.

Why waiting until a crisis may limit senior care options

Financial costs are not the only downside of delaying senior care conversations. Families may put off senior care planning because their loved one still seems healthy. But waiting too long may affect health outcomes and limit care choices, leading to rushed decisions, fewer options, and greater stress for everyone.

Niki Gewirtz, the manager of sales performance and training at A Place for Mom, says this is a scenario she’s seen play out many times in the 20+ years that she’s helped families navigate care options. “The family waits until there’s a crisis. Their loved one is now sicker — maybe hospitalized — and needs to go into a skilled nursing facility rather than the senior living setting or home care situation everyone would prefer.”

Gewirtz says that starting with nonmedical care at home can help families avoid that situation and can even save money in the long term.

“Having someone provide a lower level of care can help keep a loved one healthier [and] more independent for longer [and] ensure they eat and take medications. It also makes the adjustment easier when the person does need a higher level of care,” she adds.

Consider this:

Understanding care options before a crisis allows families to consider supportive services that can help maintain senior independence and improve health outcomes.

Families in crisis mode may have limited senior care options to choose from, primarily due to an ongoing national shortage of professional caregivers within the long-term care sector. Low wages, high turnover rates, and a fast-growing senior population all contribute to the problem. The National Center for Health Workforce Analysis projects that demand for personal care aides will rise 38% and demand for home health aides will rise 36% from 2023 to 2038. However, the Bureau of Labor Statistics projects that employment of personal care aides and home health aides will only grow 17% from 2024 to 2034. This marked difference between the estimated supply of and demand for long-term care workers underscores the importance of planning ahead for senior care as much as possible.

A last-minute search for home care services — without guidance or proper support — often means less time to interview and compare agencies and can result in having fewer reliable choices in terms of schedules and providers. Families may also have less time to coordinate care schedules among other providers like doctors, physical therapists, and nurses.

Similarly, families seeking a senior living setting for their loved one on short notice may find themselves compromising. Waiting lists are common for reputable, affordable communities. This means that preferred locations, floor plans, amenities, and price points may not be available immediately. Seniors and families may have to take the first available opening rather than choosing a community based on the best fit.

“If you’re waiting for a crisis moment to happen, you may be stuck with what you can find and not truly the best option for your loved one. It’s always best to have a plan in place,” Gewirtz says.

The real cost of family caregiving

Family caregiving, at its core, is both an act of love and a long-term financial and emotional commitment. According to A Place for Mom’s 2025 State of Caregiving Report, family caregivers spend an average of 23 hours per week on caregiving tasks, and 75% of family caregivers provide care for at least a year. That’s the equivalent of a part-time job on top of working, parenting, and other personal responsibilities.

Richard Wexler, J.D., CEO of the nonprofit APlan2Age, is all too familiar with the multifaceted struggle that family caregivers face.

“I’m an older parent, and some years ago, my wife and I found ourselves providing care for all four of our parents while taking care of two young kids. That experience was so stressful and difficult,” he says.

In addition to the risk of caregiver burnout, 69% of family caregivers say the role places a significant strain on their finances. While many families hesitate to acknowledge caregiving as a financial burden — seeing it instead as their duty — the cumulative effects can follow caregivers and their family members for years.

Even when families help pay for a loved one’s care, the larger financial impact of caregiving often comes from reduced work hours, lower earning potential, diminished retirement savings, and career stagnation. Roughly 1 in 10 caregivers leave the workforce entirely to care for an aging family member, while 35% report having less time to focus on work. The result? An estimated loss of over $21,000 in yearly income on average.

“There is a cost to the time the family spends providing care and assistance — whether that is time away from work, family obligations, or self-care,” Gewirtz cautions.

For members of the sandwich generation, the combination of caregiving and a career is an even more delicate balancing act. They’re supporting aging parents at their most vulnerable while trying to stay present for children in their formative years — all while absorbing the career and earning impacts of carrying both loads.

Consider this:

Exploring available care resources can help families create more sustainable caregiving arrangements to support both the senior’s and the caregiver’s health and financial future.

Wexler was so moved by his own experience that it inspired him to start “Caring in America,” a podcast to help educate and empower other family caregivers. His podcast eventually led to the founding of APlan2Age, which offers free care planning information and resources.

“I found myself offering advice to help other families avoid that situation,” Wexler recalls. “That’s how APlan2Age got its start.”

A proactive approach to senior care planning

In a 2025 survey of family caregivers, more than half (54%) reported wishing they had begun planning for senior care sooner. Early planning gives families time to clarify long-term care goals and preferences, align financial resources, and define roles and responsibilities. It also allows families to put essential legal protections in place — creating the foundation for a sustainable and well-rounded care plan.

Set goals and learn about care options

The first step in creating a senior care plan is identifying personal preferences for long-term care. While more than half of caregivers (53%) report a strong preference for in-home care over senior living, having open conversations about what aging in place truly requires helps set realistic expectations.

Aging at home may be achievable, but — just like transitioning to senior living — it comes with potentially high costs. Families need to prepare for expenses such as home modifications, in-home support, transportation, and help with daily tasks.

It’s equally important to consider alternative plans if staying home becomes too challenging, unsafe, or expensive. Exploring options early on, such as a move to senior living, allows families to compare costs, prepare financially, and make decisions that honor a loved one’s preferences as their needs change.

Today’s senior care landscape is diverse, offering a wide range of services — from home care and adult day care programs to assisted living and specialized memory care. Yet 41% of family caregivers report they aren’t sure what they’re looking for in a senior care experience, and 88% say they need more guidance when navigating senior care. Seeking information and support to understand options in advance can empower families to make more informed choices.

Form a care team with clear roles

Effective care planning relies on well-defined roles and support systems. Early planning allows families to establish clear decision-making structures — from designating a power of attorney to determining who will manage appointments, provide hands-on assistance, or contribute financially. Clear delineation of roles can help minimize the risk of family conflict and promote a more equitable distribution of caregiving responsibilities.

Beyond family involvement, professional expertise can play a critical role in developing financially and logistically sustainable care models. Financial advisors help project long-term costs and identify viable funding strategies. Elder law attorneys ensure legal documents are current and aligned with a senior’s evolving preferences. And senior care experts — such as advisors at A Place for Mom — bridge knowledge gaps to help families understand care options and costs when needs change.

“Asking the right questions helps the advisors create options tailored to the senior’s needs and offer solutions that the family may not have even considered,” Gewirtz explains.

A multidisciplinary team that combines family engagement with professional guidance positions families to adapt more successfully as health, financial, logistical, and emotional demands evolve over time. When planning occurs proactively rather than during a crisis, it may be less overwhelming and more financially viable.

Consider this:

When families define responsibilities and involve trusted professionals early, they build a stronger care foundation that reduces conflict and adapts more easily to changing health or financial needs.

Understand care costs

Grounding a senior care plan in realistic cost expectations can help protect a family’s financial stability while helping to ensure access to the appropriate level of care at the right time.

A clearer understanding of projected care costs enables more deliberate financial decision-making in the years preceding care needs. Even preliminary cost estimates allow families to budget, save, invest, and assess benefits strategies with greater intention. This level of clarity can inform decisions about when to seek additional support, how to pace spending, and when to adjust the care plan.

Explore payment options

Planning for senior care requires a comprehensive assessment of the funding options available. A common misconception is that Medicare pays for long-term care, when in reality it will only cover medically necessary home care services and nursing home stays for a limited time. In fact, nearly half of families (46%) rely on a combination of private pay sources such as monthly income, savings, investments, home equity, and contributions from family members to pay for care.

A practical first step is to evaluate current income and assets as well as any future income sources, such as Social Security benefits, pensions, and annuity payments. With this baseline in place, families can determine whether additional assets and tools — such as home equity, insurance products, government programs, and family support — might help fill the gaps. Each option carries financial, tax, legal, and logistical implications.

Home equity is one of the most common — and often most valuable — financial resources available to pay for senior care. Families may choose to rent the property, use a reverse mortgage to access funds while the senior remains in the home, or sell the home. However, Massachusetts-based elder law attorney Jay Marsden explains that selling a home can introduce logistical implications and complicate family dynamics: “If an adult child is living with Mom and Dad, selling the home essentially means putting them out in the street, which can exacerbate family tensions.”

When personal resources fall short, family members sometimes step in to help. Gewirtz emphasizes the importance of transparency in these arrangements: “It’s essential to have candid conversations not only about what’s important to the senior, but also who else can contribute and how much.”

Support may also take the form of unpaid caregiving. Some families step in to provide unskilled care themselves, helping with daily activities, such as dressing, bathing, and eating.

Insurance tools — including long-term care insurance and certain life insurance products — can also help offset costs, but they require advance planning and a clear understanding of policy terms. Coverage levels, benefit triggers, waiting periods, and documentation requirements vary. Orestis recommends “being ready to be denied.” Carefully compiling all supporting medical and financial documentation — including notes from physician visits, specialist referrals, and needs assessments — can strengthen the initial claim and reduce delays.

For those who qualify, veterans benefits can offer meaningful financial relief. Graham notes that these benefits are “hugely underused nationally,” largely because families are unaware of what they’re entitled to receive. Consulting a VA-accredited agent can help families prepare documentation and avoid missteps that delay or prevent access to benefits.

Lastly, Medicaid is a critical source of support for seniors with limited incomes and assets, yet it’s one of the most complex aspects of America’s long-term care system. Programs, benefits, and eligibility criteria vary by state, and the requirements can be difficult for families to navigate. Even when a loved one’s finances appear straightforward, proactive Medicaid planning is essential to avoid penalty periods and unintended financial consequences.

Create a care budget

Creating a care budget is one of the most practical steps to evaluate a family’s ability to afford care and the long-term sustainability of financial resources as care needs evolve. The process begins with accounting for all sources of income and assets, including savings, pensions, Social Security benefits, investment accounts, and home equity. Outlining debts and ongoing monthly expenses can offer a clear picture of what funds are available for care.

With this information, families can estimate how long current and projected funds may cover different care scenarios, such as in-home support or senior living. A detailed budget also informs strategic decisions about larger assets, such as whether to sell or rent a home, downsize, or consider a reverse mortgage as part of a broader financial plan.

Understanding the gap between resources and expected care costs can help determine whether Medicaid may be needed in the future. Early clarity gives families more time to adjust their plans, explore benefits, and make informed, financially sound choices.

Consider this:

A thoughtful care budget provides the clarity families need to align financial resources with future care needs and explore options proactively.

Develop a legal plan

Developing a legal plan ensures preferences are clearly documented and enforceable, even if the senior eventually becomes unable to advocate for themselves. Core documents typically include powers of attorney for health care and finances, a living will or advance directive, and a will or trust to guide the distribution of assets. Putting these pieces in place reduces uncertainty and minimizes the risk of conflict and delays when decisions need to be made quickly.

For families who expect to rely on Medicaid or want to preserve certain assets, legal planning may also require an understanding of Medicaid eligibility rules and the allowable planning approaches that help families stay compliant with program requirements. Consulting an elder law attorney can help ensure that documents are properly structured and that financial decisions align with state-specific regulations and long-term care goals.

Revisit plans regularly

Care plans aren’t static — they must evolve as a senior’s health status, living arrangements, and financial resources change over time. Revisiting plans regularly is essential, especially after major health events, significant financial developments, or family changes, such as illness, death, or loss of a primary caregiver.

Periodic reviews help families recalibrate budgets, update legal documents, reevaluate care options, and stay aligned on roles and expectations. Most importantly, revisiting the plan keeps communication open. Regular conversations make it easier to address concerns proactively, identify emerging needs, and ensure that everyone is prepared for what comes next.

Starting conversations about senior care

Planning for senior care can feel daunting — not only because decisions are complex but because they touch on core issues of independence, identity, and family dynamics. However, these conversations don’t need to happen all at once. The most effective planning typically emerges from a series of thoughtful, incremental discussions that build trust and clarity over time. Starting early, maintaining a positive tone, and choosing appropriate moments to engage can make the process more comfortable for everyone involved.

While family members and professionals — including physicians, financial advisors, and attorneys — play important roles in care planning, 84% of caregivers agree that the senior remains the most important voice in the decision-making process. Yet initiating these discussions can be challenging for both older adults and their families.

Wexler recommends approaching conversations about senior care with intention and preparation. This may include checking in with siblings first to determine who is in the best position to talk with the loved one. He suggests that starting the conversation can be as simple — and as gentle — as saying: “Mom, I could use some advice on what’s important to you when you need care.” Offering advice is often a natural role for parents, and this framing invites them to lead decision-making rather than feel pushed or overruled.

It also helps to start small. Early conversations should focus on the senior’s goals, preferences, and values. As circumstances evolve, revisit the discussion to address changes in health, finances, or living arrangements. Wexler notes that APlan2Age offers resources to help families start conversations before a crisis occurs.

Consider this:

Small, ongoing conversations help families stay connected on what matters most, making later care decisions more comfortable and more aligned with a loved one’s wishes.

Support from outside the family can also reduce tension and help keep discussions focused on shared goals. Erin Martinez, Ph.D., CFLE, associate professor of gerontology at Kansas State University, says involving a neutral party — such as a family therapist, social worker, or trusted friend — can help facilitate more collaborative decision-making. She also encourages caregivers to draw on local and community-based resources.

“Community supports such as local Area [Agencies] on Aging offer practical resources, and many elder law practices have satellite offices for people who live in rural areas,” she explains.

Her advice to caregivers? “Make community connections,” Martinez urges. “Don’t feel guilty for using free or low-cost resources even if you feel that others need them more. It’s OK to ask for help.”

Beginning the conversation early — and returning to it regularly — positions families to navigate senior care with greater clarity, respect, and shared purpose. It helps to ensure that when needs change, everyone already knows what matters most.

Note: This article was developed in collaboration with APlan2Age, a nonprofit organization focused on helping individuals and families prepare for aging with intention, clarity, and confidence. Through free tools, practical guides, and expert-informed resources, APlan2Age encourages proactive planning and early conversations about care, finances, and personal priorities — so families are better prepared long before decisions become urgent.

FAQs

What happens if families wait too long to plan for senior care?

Waiting to plan for senior care often leads to rushed decisions, higher costs, and fewer care options when a health crisis occurs. Many families who delay end up needing care within 60 days, leaving little time to compare services or pricing. Early planning helps reduce financial stress and preserves more choices.

Why do senior care costs end up being higher than families expect?

Many families underestimate senior care costs because they begin researching during a crisis and lack time to fully understand pricing structures. Assisted living, memory care, and home care expenses can add up quickly, especially as care needs increase. Planning ahead allows families to budget realistically and explore financial tools before costs escalate.

How can early conversations about senior care protect a family’s finances?

Starting senior care conversations early gives families time to explore insurance, benefits, and asset-planning strategies that may not be available later. It can help avoid rushed asset sales, tax consequences, and delays in Medicaid or veterans benefits eligibility. Proactive planning supports both financial stability and long-term care goals.

This story was produced by A Place for Mom and reviewed and distributed by Stacker.