5 factors that secretly raise your auto insurance rates

You drive safely. You haven’t filed a claim in years. Yet, when that auto insurance bill arrives, the number seems stubbornly high. Why?

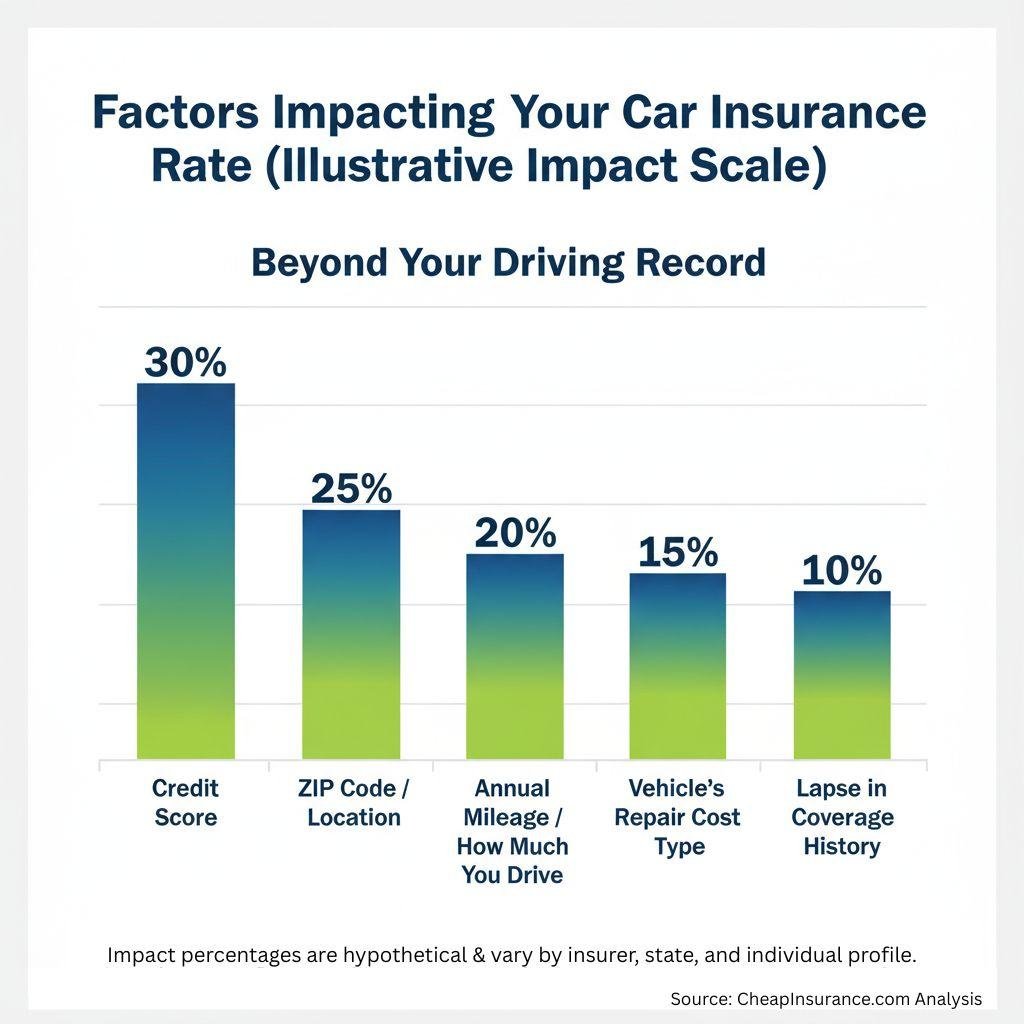

Most drivers believe their rate is based solely on their driving record. That’s only half the story. Your insurance company is actually running a deep, data-driven analysis that pulls information from five surprising, often hidden factors you’d never expect. These silent influencers, from your credit score to your ZIP code, are quietly pushing your rates up, regardless of how clean your record is.

This is your guide to unmasking those forces. CheapInsurance.com is pulling back the curtain to expose the true risk formula. Understanding these invisible influencers is the single most powerful step you can take to challenge your next renewal quote and reclaim control over your policy. Let’s dive in and expose the five secret factors that inflate your auto insurance rates.

1. The Not-So-Secret Agent of Cost: Your ZIP Code (Location, Location, Location!)

Insurance companies are masters of statistical risk assessment, and your ZIP code is a giant red flag, or a green light, on their map. They aren’t just looking at your past claims; they’re looking at the collective risk of your neighbors. Live in a bustling, high-traffic metro area? Rates go up. Is your neighborhood seeing a spike in car break-ins or theft? Up goes the rate. Are you on the coast where hurricanes are common, or in a region prone to severe hail storms? You guessed it: premium spike.

The Personality Angle

It feels profoundly unfair, doesn’t it? You could be a meditative, zen driver who follows every rule, but if the guy three blocks over keeps totaling his sports car or your neighborhood watch is fighting off catalytic converter thieves, you end up subsidizing the chaos.

Actionable Solution

If you park on the street, consider an anti-theft device or garage parking for a potential discount. More importantly, compare auto insurance quotes aggressively. Some insurers use more granular data than just a ZIP code, giving less weight to neighborhood crime statistics and more to your personal driving history.

2. The Unseen Hand: Your Credit-Based Insurance Score

This one is arguably the most controversial factor on the list. Why should your ability to manage a credit card affect your car insurance?

The Insider Scoop

In most states (with exceptions like California, Hawaii, and Massachusetts), insurers use a credit-based insurance score, which is different from your standard credit score, to predict the likelihood of you filing a claim. Studies have shown a correlation: Historically, drivers with lower credit scores are statistically more likely to file more claims, and higher-cost claims, over time. Insurers view a high score as an indicator of overall financial responsibility and, by extension, lower risk.

The Personality Angle

This factor can feel like a punitive double-whammy, especially for young drivers or those recovering from past financial hardship. It’s like the financial world is judging your ability to handle a fender-bender based on a late student loan payment from two years ago. It’s a harsh reality check on the interconnectedness of your financial life.

The good news? You can actively improve this. Focus on fundamental financial health: Pay bills on time, keep credit card balances low, and monitor your report for errors. As your score rises, request a new quote, it’s an investment that pays off in lower car insurance rates.

3. Mileage Matters: How Much You Actually Drive

The less you’re on the road, the less chance you have of an accident. Simple logic, but how is the insurer tracking it?

The Insider Scoop

Your annual mileage is a direct measure of exposure risk. A driver commuting 25,000 miles a year for a long-haul sales job is mathematically more likely to be involved in an incident than someone who only drives 5,000 miles for weekend errands. When you first sign up for a policy, you estimate this number, but often, people forget to update it as their life changes (example: switching to remote work).

The Personality Angle

If your life pivoted during the pandemic to a work-from-home setup, and you’re still reporting your old 15,000-mile commute, you’re essentially over-paying for a ghost risk that no longer exists. This is money being left on the table!

If you drive less than 10,000 miles, call your agent right now to update your estimate. Better yet, look into telematics programs or usage-based insurance (UBI) offered by companies. These programs use a small plug-in device or a smartphone app to track your actual mileage and driving habits (speed, hard braking), rewarding safe, low-mileage drivers with discounts of up to 30%.

4. Your Ride’s Repair Cost: Age, Tech, and the “Cool Factor”

Is your car a technological marvel or an obscure classic? Both can cost you.

The Insider Scoop

Insurers don’t just care about the car’s value; they obsess over the cost of repair. A brand-new luxury SUV packed with sensors and complex aluminum body panels might not be more likely to crash than a sedan, but if it does, the claim will be astronomical. Replacing one sensor in a modern bumper can cost more than a traditional bumper replacement. Conversely, high-performance sports cars inherently carry a higher risk profile due to speed capabilities.

The Personality Angle

That pristine 1965 Mustang you restored? While it might be a showstopper, the insurer sees a nightmare of expensive, hard-to-find vintage parts and specialized labor. That sleek new electric vehicle (EV) that cuts down on gas costs? It’s often an expensive repair bill waiting to happen, due to the battery placement and cutting-edge tech. The sweet spot, financially, is often a moderately-priced, mass-market vehicle with great safety ratings.

Vehicles with top safety picks (like automatic emergency braking and advanced restraint systems) often qualify for substantial safety discounts, helping to offset the repair complexity cost.

5. The “Forbidden Gap”: Lapses in Continuous Auto Coverage

This factor is a genuine financial penalty for not having auto insurance, even if you weren’t driving.

The Insider Scoop

Maintaining continuous auto insurance coverage is one of the easiest ways to prove to an insurer that you are a reliable, responsible customer. Even a brief, voluntary lapse in coverage (a gap of a few days or weeks) is viewed as a major red flag by underwriters. They assume you either drove uninsured (a huge risk) or are simply unreliable, placing you in the “high-risk” pool, which comes with significantly elevated rates when you decide to buy a new policy.

The Personality Angle

Imagine you sell your old clunker and plan to take the bus for six months before buying a new car. You cancel your policy. When you finally go to insure your new ride, the first question is, “Were you continuously covered?” Answering “No” can instantly slap an extra 10-20% on your new rate. You’re being penalized for making a financially sound choice to avoid unnecessary costs!

Never cancel your policy outright unless you’re absolutely certain you won’t own a vehicle for an extended period. If you’re storing a car, switch to “storage” or “comprehensive only” coverage. This removes collision and liability but maintains a continuous record, protecting you from the high-risk premium penalty when you add full coverage back later.

Final Pit Stop: The Proactive Driver’s Checklist

You now possess the five hidden keys to your insurance rate. Don’t let this knowledge sit idle! The insurance world is designed to be confusing, but a savvy consumer can win the game.

Your Annual Review Action Plan

- Re-Verify Your Mileage: If your commute has changed, update your annual miles immediately.

- Credit Check-Up: Run your free annual credit report and fix any errors that could be dragging down your score.

- Shop the Competition: Compare quotes every 12 months. Insurers offer their best rates to attract new customers, so loyalty often means you’re overpaying.

- Confirm Your Discounts: Ask your agent to list every discount applied. You might be missing out on “good student,” “bundling,” or “advanced safety feature” savings.

By taking control of these five factors, you move from being a passive payer to an active premium manager. Get out there, negotiate with confidence, and make sure you’re not secretly footing the bill for risks that aren’t yours.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.