Actual cash value vs. replacement cost: Which renters policy saves you money?

The world of insurance can often feel like deciphering an overly complex text. The field is dense, confusing, and frequently causes frustration for policyholders. However, when examining renters insurance, one critical distinction exists that can determine financial outcomes following a loss: actual cash value (ACV) versus replacement cost value (RCV).

This is not simply insurance jargon; it represents a fundamental choice within renters insurance that dictates the monetary recovery amount when a disaster strikes. In an environment where consumers strive to be savvy with spending, understanding this difference is not just beneficial, but essential for protecting the policyholder’s finances and peace of mind under the terms of the renters insurance agreement. Cheap Insurance will demystify ACV and RCV, explore their respective merits, and determine which renters insurance policy truly delivers superior financial protection when it is most needed.

The Great Divide: What Are ACV and RCV?

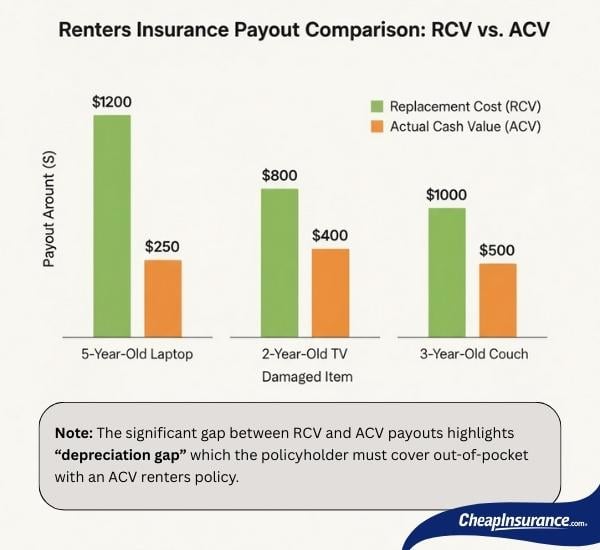

Imagine a scenario where an apartment suffers damage from a burst pipe, resulting in the ruin of a 5-year-old laptop and a 2-year-old couch. Upon filing a renters insurance claim, the method the renters insurance company uses to calculate the payout determines the financial outcome for the policyholder. This critical determination involves actual cash value (ACV) and replacement cost value (RCV), each representing a distinctly different approach to settling the renters insurance claim. Understanding the method employed by the renters insurance policy is essential for all policyholders.

Actual cash value: The “Used Market” Approach

Actual cash value in renters insurance is best understood as the amount an item would fetch on a used market just prior to being destroyed or damaged. Essentially, ACV is calculated as the item’s replacement cost minus depreciation.

- Replacement cost: The cost to purchase a brand new, similar item today.

- Depreciation: The loss in the item’s financial value due to age, wear, and tear. Everything loses value over time, a key factor in the ACV determination of a renters insurance claim.

The ACV Calculation for Renters Insurance

If a policyholder’s laptop cost $1,000 new five years ago, and a similar new one today costs $1,200, an ACV renters insurance policy will not provide the $1,200 replacement amount. Instead, the policy determines the current depreciated value of the five year old laptop. If that current value is only $200, that reduced amount becomes the claim payout.

Key Takeaway for Renters Insurance

ACV renters insurance policies typically come with lower insurance premiums. The policyholder pays less upfront but receives a lower payout in the event of a covered claim.

Replacement Cost Value: The “Brand New” Approach

RCV is considered the superior option for renters insurance payouts. A policy utilizing RCV aims to restore the policyholder to the same financial position held immediately before the loss occurred, without factoring in depreciation of belongings.

The Calculation

Considering the example of a damaged laptop, if the cost to purchase a brand new, comparable laptop is $1,200 today, an RCV renters insurance policy provides a payout of $1,200 (less the applicable deductible). The actual age of the destroyed item is irrelevant to the payment amount for the item’s replacement.

Key Takeaway for Renters Insurance

RCV renters insurance policies typically involve higher insurance premiums. The policyholder pays a modest amount more upfront but is guaranteed the full value required to replace damaged items with new ones.

Saving Money: Short-Term vs. Long-Term

The core question regarding renters insurance is which policy ultimately results in greater savings. The answer is not simple, as it depends entirely on the policyholder’s definition of “saving money.”

ACV: The ‘Save Money Now’ Renters Insurance Option

- Lower insurance premiums: This is the most attractive feature of this type of renters insurance. When operating on a tight budget, an ACV policy will undoubtedly offer a cheaper monthly or annual premium for renters insurance coverage.

- Good for minimal possessions: If a policyholder owns very few possessions, or if most belongings are inexpensive and easily replaced without a significant financial hit, ACV renters insurance might appear sufficient.

- The trap: While a policyholder saves money on the immediate renters insurance premium, there is a risk of facing a substantial financial burden when replacing many items after a covered loss. The gap between what ACV renters insurance pays out and the actual cost to replace everything new can be massive. This means the policyholder is effectively self-insuring a large portion of the property’s value.

RCV: The ‘Save Money When it Counts’ Renters Insurance Option

- Higher premiums: An RCV renters insurance policy requires paying a bit more upfront. This represents the trade-off for obtaining superior coverage under the renters insurance agreement.

- Full replacement power: This is where RCV renters insurance truly excels. If belongings are destroyed, the policyholder receives enough money to buy new replacements, significantly easing the financial strain of rebuilding.

- Peace of mind: Knowing that treasured and expensive possessions, from electronics to furniture to clothing, can be replaced without dipping deep into savings or acquiring debt, offers immense peace of mind.

- The smart investment: While the renters insurance premiums are higher, the potential payout in a catastrophic event could be many times the additional premium paid over years. This makes RCV a much smarter long-term financial decision for most renters insurance policyholders.

What’s In Your Apartment? A Reality Check

The optimal method for deciding between actual cash value and replacement cost value for a renters insurance policy is to conduct a realistic inventory of belongings. The policyholder should assess items room by room, including the contents of closets and drawers, to properly value the coverage needed under the renters insurance plan.

Valuation Questions for Renters Insurance

- Electronics: Assess the age of the television, laptop, tablet, and gaming console. Determine the cost to replace them with new versus the estimated used market value. The rate of depreciation on electronics is a crucial factor when choosing renters insurance coverage type.

- Furniture: Note the age of the couch and other furnishings. Ascertaining whether the item is a basic piece or a custom item is vital for accurate valuation under a renters insurance claim.

- Clothing and shoes: Question whether the entire wardrobe could be replaced with the depreciated “used value” paid out by an ACV renters insurance policy.

- Appliances (if owned): Note the age of all owned appliances, such as the microwave, toaster, and coffee maker.

- Jewelry, art, collectibles: These items often require unique valuation methods and may need specialized scheduled personal property coverage, an endorsement often added to the standard renters insurance policy, regardless of the ACV or RCV structure.

RCV Usually Wins for Long-Term Savings

For the vast majority of renters, Replacement cost value is the financially smarter choice for a renters insurance policy. While actual cash value offers lower upfront insurance premiums, it transfers a significant amount of risk and financial burden back to the policyholder. In the event of a substantial loss, the difference between an ACV and RCV payout could be thousands, or even tens of thousands, of dollars. That difference far outweighs the small annual savings achieved on an ACV renters insurance premium.

A fundamental purpose of purchasing renters insurance is to protect financial wellbeing. If a policy only provides a fraction of what is needed to replace possessions, the protection offered by the renters insurance is compromised.

Circumstances under which ACV renters insurance might be considered include situations involving extremely minimal possessions where most items are inexpensive and easily replaced, or a highly temporary living situation where belongings are primarily borrowed or disposable. However, even in these niche cases, the complete protection and peace of mind offered by RCV renters insurance often makes it the preferred option.

Next Steps: Get the Right Renters Insurance

To acquire the most effective renters insurance, several action steps are necessary.

- Inventory of belongings: A thorough inventory of possessions should be conducted. Listing every item and estimating new replacement costs often provides a necessary shock that clarifies the actual need for comprehensive renters insurance coverage.

- Quote comparison: When obtaining renters insurance quotes, the applicant should always request both actual cash value and replacement cost value options. A comparison of the premium difference may reveal that the cost increase for superior coverage is not as dramatic as initially assumed.

- Policy review: It is essential to read the fine print of the renters insurance documentation. A clear understanding of the deductible and any specific sublimits on certain categories of items, such as jewelry or electronics, is paramount.

The allure of a slightly cheaper upfront premium must not distract from the potential financial disaster posed by an ACV policy. Prudent investment in RCV renters insurance ensures that if an unexpected event occurs, the policy truly aids in rebuilding, rather than merely recovering a fraction of what was lost.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.