Don’t let winter cost you: Essential insurance changes for the off-season

The onset of winter presents a unique convergence of aesthetic beauty and significant financial risk. While the season offers picturesque scenery, it simultaneously introduces hazards like frozen pipes, increased liability for premises injuries, and damage to seasonally stored assets. These incidents frequently lead to costly insurance claims that can severely impact a household budget.

A common pitfall is treating an insurance policy as a static agreement. However, as climatic conditions and personal usage patterns shift dramatically with the seasons, your coverage requirements must be proactively recalibrated. Optimizing your insurance strategy now is a critical risk management step that can result in substantial financial savings and mitigation of catastrophic loss.

To protect your assets and maintain fiscal stability through the off-season, CheapInsurance.com will outline the essential insurance adjustments required for your home, vehicles, and specialized equipment.

Which Season Has the Most Accidents?

When you think of “accident season,” your mind probably jumps to the icy roads of January. While winter certainly has its dangers, the most frequent time for claims often begins much earlier than you think — right now, in Q4 (October, November, and December).

The rise in accidents and claims during this period isn’t just about the first snow; it’s a combination of unique factors that peak around the holidays:

- Darker commutes and headlight fatigue: Shorter days mean more time driving in the dark. Bad headlights are dangerous, but they also signal something to your insurer. If your lights are yellowed or dim, it speaks to general neglect, which can affect your risk profile.

- The “hurry-up” factor: Holiday shopping, end-of-year deadlines, and travel for family gatherings lead to distracted and rushed driving. Even without ice, parking lot fender-benders, minor collisions, and speeding tickets spike.

- Property claims from pre-winter prep: A huge number of claims arise not from the storm itself, but from the prep before the storm. Think about it: ladder accidents while trimming dead branches, or cleaning gutters, or even a DIY plumbing project gone wrong before the freeze sets in.

The Q4 Policy Review: Should You Change Your Deductible Before the New Year?

Your deductible, the amount you pay out of pocket before your insurance starts covering a claim, is a powerful financial tool. Reviewing it in Q4 is a strategic move, especially if your financial situation has changed.

Strategic Winter Policy Adjustments

Beyond the deductible, the end of the year is the perfect time to add specific endorsements that are most relevant to the coming season.

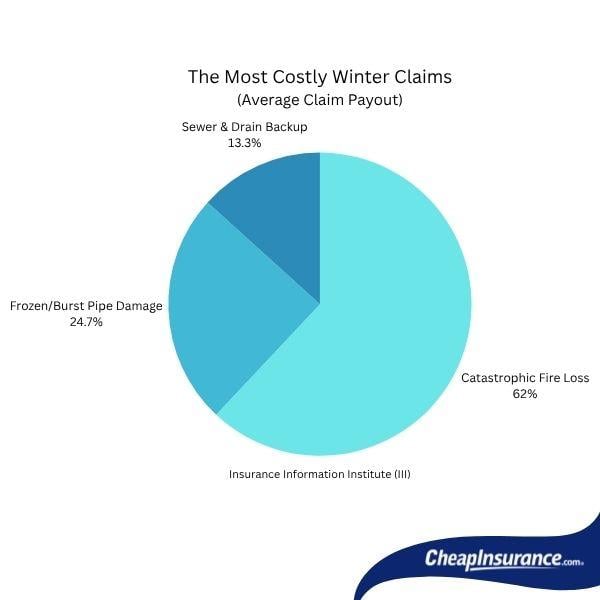

- Sewer and drain backup: Frozen ground and heavy snowmelt can stress municipal sewer systems, pushing water and sewage back up your drains. Standard homeowners policies do not cover this, as it requires a specific endorsement. This is non-negotiable for winter peace of mind.

- Increased contents coverage for gifts: Did you buy a new gaming system, a diamond necklace, or an expensive new snowboard for a family member? Your personal property limit might cover the total loss, but individual categories (like jewelry) are capped. Add a personal property floater (or scheduled property endorsement) now to cover those new high-value items the second they enter your home.

Homeowners Insurance: Bracing for the Deep Freeze

Winter is arguably the toughest season on your home. Heavy snow, ice, and extreme cold create unique risks that your standard homeowners insurance policy might not cover as well as you think.

Conquer the Cold Weather Exclusions

The most common and costly winter claims are often for frozen pipes and ice dams. Many policies have specific exclusions:

- Frozen pipes: Some policies require that you maintain a minimum temperature (like 55-60 degrees Fahrenheit) or have a neighbor check on your home if you’re away. If you don’t meet these rules, your claim might be denied.

- Ice dams: Damage from water leaking into your home due to an ice dam is usually covered, but the actual cost to remove the ice dam itself may be excluded. Ask your agent about an endorsement to cover specific ice-related mitigation.

Guard Your Walkways: Liability in the Snow

That blanket of fresh snow is a beautiful sight until your mail carrier slips on the black ice underneath.

- Key review: Ensure your personal liability coverage limits are high enough (at least $300,000 to $500,000) to protect your assets in case of a serious injury lawsuit.

- Preventative action is protection: Clearing snow and salting walkways promptly is not just neighborly; it’s a crucial risk management practice that can prevent a claim entirely.

Auto Insurance: Strategic Coverage for Seasonal Storage

If you own a seasonal vehicle such as a classic car, convertible, RV, or motorcycle that will be stored and undriven throughout the winter, you are likely overpaying for unnecessary coverage. Maintaining a full, year-round auto insurance policy, or motorcycle insurance policy on a parked asset is a common, yet easily corrected, budget inefficiency.

The Financial Strategy: Comprehensive-Only Coverage

The most significant financial adjustment you can make is to suspend your active driving coverages and maintain only Comprehensive Coverage (often referred to as “comp-only” or “storage insurance”).

Protecting Your Winter Gear and Adventures

As you put away the summer car, you’re likely pulling out expensive winter equipment like skis, snowboards, snowmobiles, and specialized clothing. Don’t let the loss of a new snowboard or a backcountry medical emergency turn your fun into a financial disaster.

Insuring High-Value Sports Equipment

A custom snowboard, high-end skis, or a luxury helmet represents a significant investment. Your standard homeowners or renters insurance provides limited coverage, often with low claim limits and high deductibles that make filing a claim impractical.

The solution is a personal property floater (also called scheduled coverage).

- How it works: You specifically list the high-value item and its worth on your policy.

- The benefit: Float policies often offer a low or $0 deductible and cover risks like accidental damage or theft that occur even when the item is away from your home, such as at a mountain resort. This is the most efficient way to protect your gear.

Specialized Coverage for Vehicles and Travel

Off-road vehicles and remote adventures carry risks that require policies beyond standard home and auto coverage.

- Snowmobiles and ATVs: If these “off-road toys” are leaving storage, they need their own separate policy. Your standard auto or homeowners insurance will not provide adequate liability or physical damage coverage for these vehicles.

- Backcountry safety (medical evacuation): For destination trips and remote skiing, travel insurance with a focus on high limits is crucial. The most critical component is medical evacuation coverage. This pays for the emergency transport from a remote location (like the side of a mountain) to a suitable hospital — a cost that can easily run into five figures and is often not fully covered by basic health insurance.

Your Winter Risk Mitigation Strategy: A Final Checkpoint

Successful financial navigation of the winter season hinges on proactive policy management, not reactive claim filing. To solidify your preparedness, dedicate a brief consultation with your insurance professional today to focus on these three high-impact adjustments.

- Comprehensive-only auto coverage: A strategic cost-saving measure for any vehicle placed in seasonal storage.

- Sewer backup endorsement: Essential protection against the most common and expensive water damage claims stemming from winter ground conditions.

- Personal property floater: Ensures high-value items and new seasonal gear are protected with adequate limits and low deductibles, regardless of where the loss occurs.

By implementing these essential off-season changes, you shift from simply being insured to being strategically protected. This vigilance guarantees your financial well-being remains resilient against the inevitable challenges of the cold season.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.