Is malpractice insurance the same as professional liability insurance?

Malpractice insurance, professional liability insurance (also called professional indemnity insurance), and errors and omissions (also called E&O insurance) are closely related. But what should you call the liability business insurance you need for your profession? The right term depends on your type of business and the types of business risks you face, NEXT reports.

Read on to learn which policy is necessary for your industry to fulfill licensing requirements, be in compliance with legal requirements or satisfy client requests.

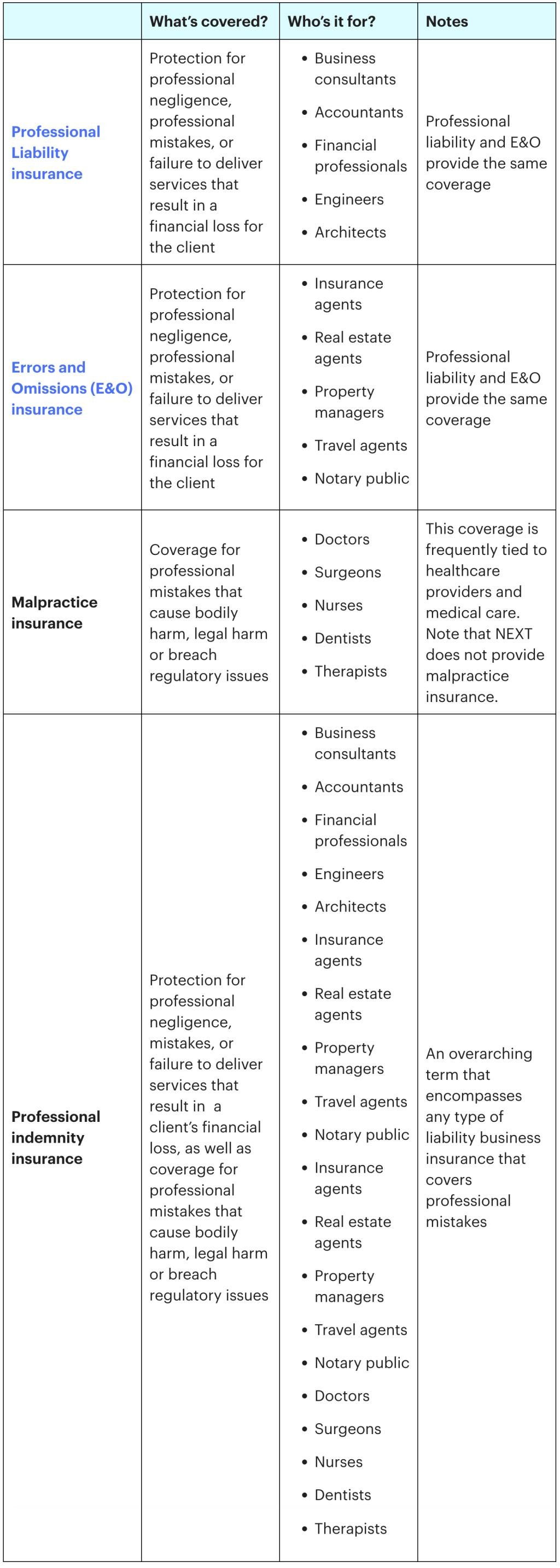

Compare professional liability vs. errors and omissions vs. malpractice insurance vs. professional indemnity insurance

What is professional liability insurance?

Professional liability insurance can help cover professional negligence, professional mistakes, misrepresentation or failure to deliver professional services as promised. That could mean a missed deadline, poor professional advice or a professional error that hurt their business.

Professional liability coverage can help cover legal defense costs, attorney fees, settlements or judgments if a client claims your work caused them financial loss – whether their accusation is true or not.

Professionals such as business consultants, accountants and financial service providers, engineers and architects often refer to this type of business insurance as professional liability.

Example of professional liability insurance in action: A small business owner hires a tax consultant to prepare their quarterly filings. The consultant overlooks a major deduction, and the client ends up with a larger tax bill than necessary. The owner sues for financial damages related to the error. Professional liability coverage can step in to help with defense and damages.

What is errors and omissions insurance (E&O insurance)?

E&O insurance is professional liability by another name for a different set of professions. It offers the same protections as professional liability insurance, but this term is more commonly used for industries like insurance, real estate, property management, travel agents and notaries public.

Like professional liability, the protection focus is on financial harm. That could include a professional misrepresentation, a missed deadline or a breach of contract that leaves your client losing money. E&O insurance coverage could offer financial protection so your own bottom line doesn’t take a hit.

Example of errors and omission insurance in action: A real estate agent provides incorrect information about a property’s zoning restrictions. After closing, the buyer realizes they can’t use the property as intended and sues for misrepresentation. E&O insurance could help cover the legal expenses and potential settlement.

E&O coverage is also frequently required in contracts, especially in fields where errors can have a ripple effect on a client’s profitability. Additionally, some state laws or contracts may require certain professions to carry E&O or professional liability. For example, Alaska real estate agents must have an E&O policy to obtain or renew their professional license.

What is malpractice insurance?

Malpractice insurance is professional liability insurance specific to fields where mistakes can cause bodily harm or serious legal consequences. It’s most often required for doctors, nurses, dentists, therapists and other healthcare professionals, but the term can also be used in other professions where errors can have high stakes.

The key difference for this type of liability policy is scope. Malpractice coverage can help cover claims that claim not just financial loss, but also injury, professional negligence or regulatory violations such as HIPAA (Health Insurance Portability and Accountability Act) breaches. Professional Liability/E&O specifically excludes bodily injury claims.

Example of malpractice insurance in action: A patient experiences complications after surgery and they claim their surgeon made a professional error in their medical procedure. Medical malpractice insurance could help with legal fees, court costs or settlements.

What is professional indemnity insurance?

Professional indemnity is a blanket term that refers to any type of professional liability business insurance for any profession. Professional liability insurance, errors and omissions insurance, and malpractice insurance all fall under the umbrella of professional indemnity coverage.

4 tips to choose the right liability coverage for your industry

Make sure the professional indemnity insurance policy you choose fits your profession and the business risks you face. A few things to keep in mind:

1. Learn the rules and requirements for your profession

Some states and licensing boards require liability coverage to work. Even if professional liability or errors and omissions aren’t required to practice, some clients may require you to show proof of insurance (also called a certificate of insurance, or COI) before they’ll sign a contract to work with you.

2. Choose the best coverage limits and deductibles for your risk

A professional indemnity policy has a maximum it will pay per claim (called the per claim limit) as well as an amount you must pay out of pocket before the insurance will kick in (known as the deductible). Higher limits can provide more protection for your business, but that usually also means a higher premium.

3. Compare costs

Monthly or annual premiums (what you’ll pay for business insurance) can vary widely depending on a number of factors, including your type of business, number of employees, insurance claims history and coverage limits (the maximum amount that your insurance company will pay for a claim). For example, malpractice insurance for a surgeon has a lot of business risk. It will often cost more than E&O insurance for an IT consultant as a result.

Learn more about professional liability/E&O insurance costs.

4. Extend your coverage continuity

Gaps in coverage can leave your business exposed to the potential of big expenses.

Optional insurance add-ons like tail coverage can help extend your business insurance protection after your policy’s end date. Say, for example, you’re an architect who retires and lets their liability coverage lapse. A former client files a claim against you because of faulty work you did back when you had coverage. Tail coverage could extend the protection of your policy if a claim comes in after your policy expires.

Some insurers also offer prior acts coverage, which can help cover incidents that happened before your current policy’s start date — as long as you didn’t already know about the issue.

Options like these can be a huge help for business professionals.

This story was produced by NEXT and reviewed and distributed by Stacker.