The state of home insurance in 2026: Increasing rates, climate change, and consumer frustration

Rate increases over the past few years have been hitting homeowners hard, thanks to increasingly volatile weather, inflation, and other factors. 2026 should see stabilization in the home insurance market, but, depending on where you live, you probably shouldn’t count on seeing lower rates on your renewal.

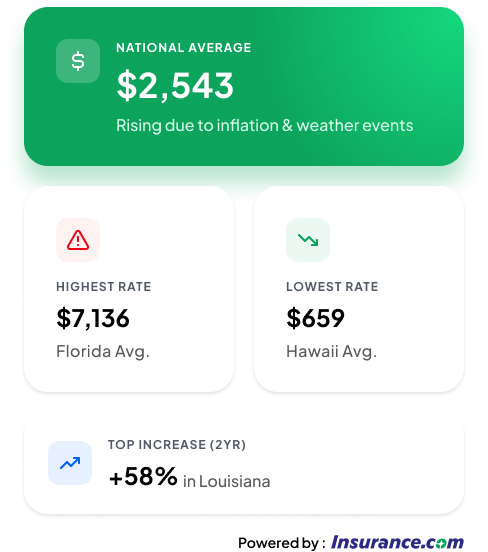

The Consumer Federation of America’s April 2025 report, Overburdened, found that U.S. homeowners spent $21 billion more on homeowners insurance in 2024 than in 2021.

Although the market in general is improving, with AM Best elevating the market segment from negative to stable in December 2025, it may be a while before many homeowners see any sign of lower rates.

What’s driving home insurance rate increases? Will rates go down in 2026, or ever? What can homeowners expect when it comes to their insurance coverage and bills, and how do they feel about it? While we see improvements on the horizon, home insurance remains a source of sticker shock and frustration. Read on for insights from Insurance.com, data, and details on the state of home insurance in 2026.

Home insurance rates rise: Here’s what’s to blame

Home insurance rates have been climbing over the past few years, with homeowners facing sticker shock both on renewal and when shopping for new coverage. There are several reasons, some less obvious than others.

- Severe weather and natural disasters. 2025 began with some of the worst wildfires in history, with billions of dollars in damage resulting from the Palisades and Eaton fires in California. Following several years of devastating wildfires and hurricanes, along with increasing damage from storms nationwide, home insurance companies responded with rate increase requests. The good news? A quiet Atlantic hurricane season provided some breathing room.

- Increased construction costs. Inflation has made all the materials used to build and repair houses more expensive. The more it costs to rebuild a home, the higher claim costs become, and insurance companies respond by increasing premiums to offset the additional expenses.

- Litigation. High numbers of lawsuits, particularly in states where the law has been favorable toward those suing insurance companies, drive up costs for insurance companies, which are again passed on to consumers.

- State regulations. Some states have much stricter limitations on home insurance rate increases than others.

Why do natural disasters or lawsuits elsewhere affect my insurance rates?

Insurance companies spread risk. While rates will go up a lot more in high-risk areas to reflect that risk, the increases can spread well beyond those areas as insurers balance their incoming premiums with their outgoing claims payments, or what they call loss ratios.

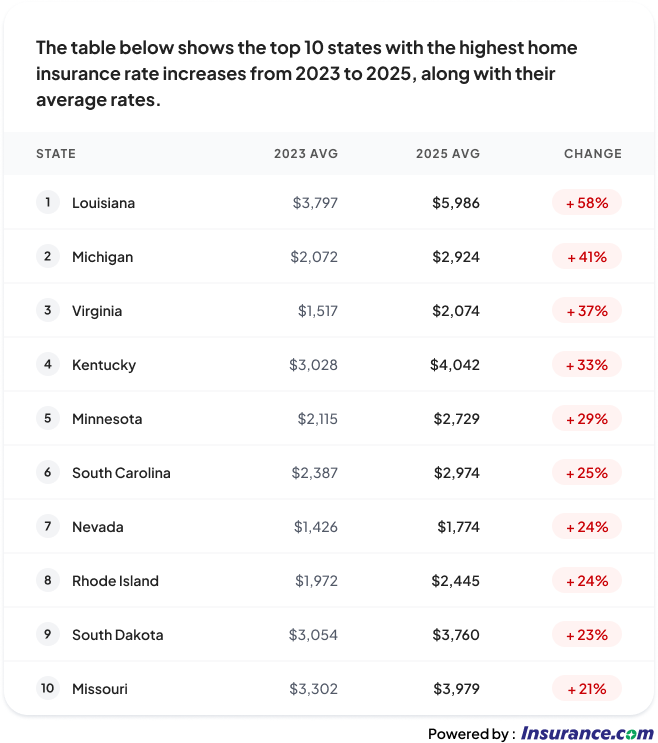

Where have home insurance rates increased the most? State-by-state trends

The state where home insurance rates have increased the most in the past two years is Louisiana, with a 58% rate increase from 2023 to 2025.

The top five states for rate increases between 2023 and 2025 are:

- Louisiana (58%)

- Michigan (41%)

- Virginia (37%)

- Kentucky (33%)

- Minnesota (29%)

What about Florida? Although Florida has struggled with high insurance rates for years, Insurance.com data show a slight reduction between 2023 and 2025. It remains the most expensive state for home insurance, but rates are starting to decrease.

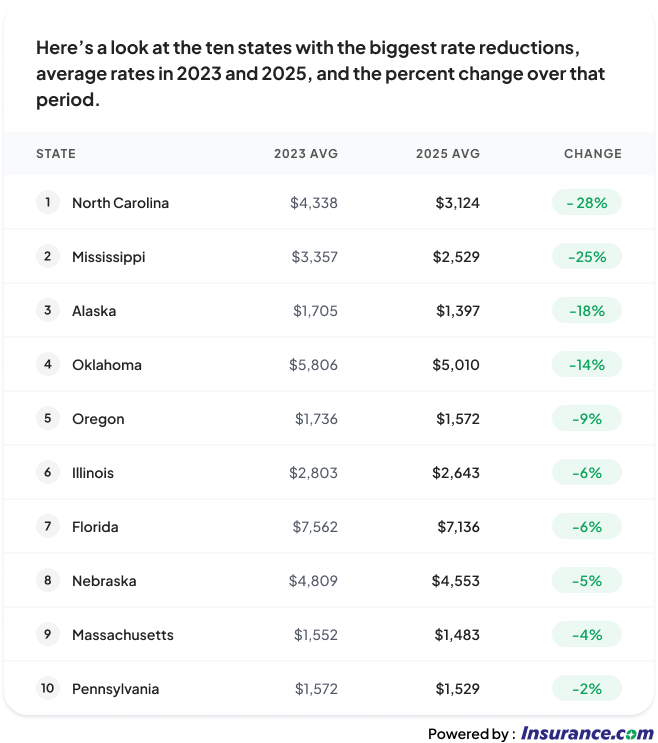

Where have homeowners insurance rates gone down?

Some states have seen significant reductions in average home insurance rates over the past two years, with North Carolina experiencing the largest drop of 28%.

The five states with the biggest home insurance rate reductions are:

- North Carolina (-28%)

- Mississippi (-25%)

- Alaska (-18%)

- Oklahoma (-14%)

- Oregon (-9%)

The biggest surprise here is that Oklahoma, previously the most expensive state for home insurance, saw a 14% drop in home insurance costs.

Florida’s modest decrease (down 6%) is good news, but less surprising, given that changes in legislation have been showing signs of improving the market and reducing insurance rates over the past year.

In December 2025, Florida’s insurer of last resort, Citizens, filed for a rate decrease of 2.6%. That follows years of big rate increases. Citizens has reduced its policy count dramatically to end 2025 with the lowest count ever (385,000 policies) as new carriers have entered the market and eased the burden.

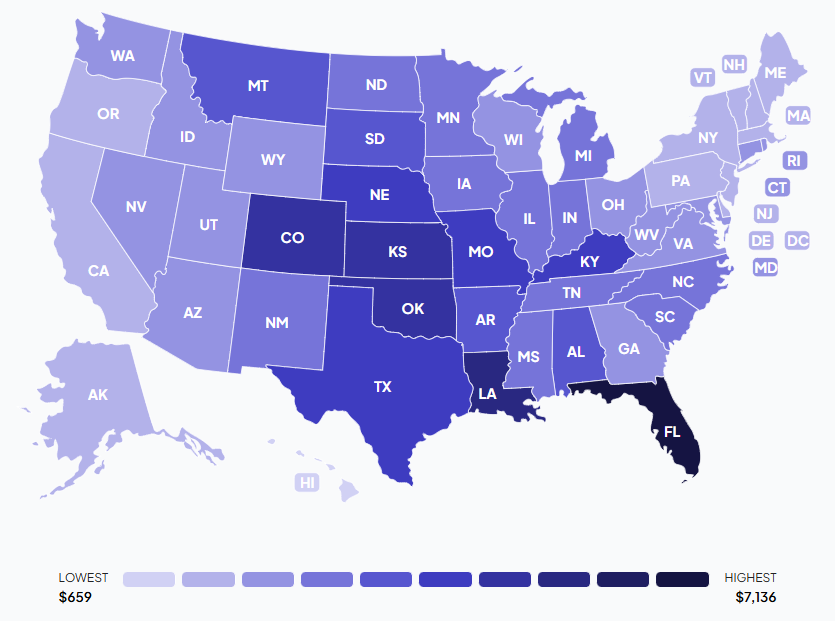

The big picture: How much home insurance costs across the U.S.

Homeowners insurance buyers' pain points: What’s driving customer satisfaction?

Not surprisingly, rates are the biggest pain point for homeowners insurance customers. Insurance.com’s annual survey found that both satisfaction with fair rate increases over time and with discounts is down five points from last year’s survey.

The areas where satisfaction decreased the most are:

- Fair rate increases (-5%). In last year’s survey, 65% of customers were satisfied with how their insurance company applied rate increases. This year, that rate dropped to 57%, indicating that while rate increases weren’t an area of high satisfaction before, the situation has worsened.

- Discounts (-5%). Fewer people are satisfied with the discounts offered by their home insurance companies, which may tie into rate increases overall. Satisfaction with discounts dropped from 68% to 63%.

- Older homes (-5%). As insurance companies pull back on risk, older homes are likely to be among those viewed as higher risk; that may result in higher rates or more difficulty finding coverage. Insurance.com’s survey found a decrease from 73% to 68% satisfaction for older home coverage.

- Digital experience (-5%). As people rely more and more on digital tools to handle insurance policies, there’s a higher expectation for those tools to be top-notch. Insurance.com’s survey found that insurers may be missing the mark, as overall satisfaction dropped from 85% to 80%.

- Buying process (-4%). Whether it’s that they are having trouble finding affordable rates, that it’s harder to get a person on the phone, or simply that the process of buying home insurance has become more of a chore, satisfaction in this area dropped from 82% to 78% overall.

Overall, customer satisfaction took a drop of 2% year over year, likely driven by some of the pain points above. Other areas that dropped:

- Exceptional standard coverages (-3%)

- Claims handling (-2%)

- Billing process (-1%)

Are homeowners insurance customers more satisfied in any areas?

There were a few categories of the survey that saw an improvement, notably in customer sentiment:

There was a 3% increase in people who said they would recommend their home insurance company, those who said they trust their insurance company, and those who plan to renew.

Additionally:

- Satisfaction with bundling increased 2%

- Ease of service and policy offerings saw slight increases of 1% for each category

Are people switching home insurance companies?

Rate increases are driving some customers to switch, according to J.D. Power’s 2025 U.S. Home Insurance Study, which tracks customer satisfaction with the overall home insurance experience.

The study found that 49% of people reported a rate increase, and it’s impacting their decision to switch carriers:

- Among people who reported a rate increase, 43% of those who also said they don’t intend to renew gave rate increases as the reason.

- Homeowners who already pay higher-than-average premiums and have multiple types of insurance were more likely to say rate increases were driving them to switch; 45% of these customers (called high-value customers due to the value of their business) who said they probably won’t renew said increased rates are the reason.

The fallout of fires and hurricanes: How increasing natural disasters are affecting insurance

Scenes of homes engulfed by fast-moving flames and washed away by hurricane-driven floodwaters have horrified viewers across the nation, and in their wake, billions of dollars in insurance claims have been filed.

More and bigger insurance claims have caused insurance companies to file rate increases, while in some areas, insurers have pulled back or even gone out of business.

State Farm in California: A real example of disaster directly driving rates

- State Farm, the largest home insurance company in the state, stopped writing new homeowners insurance policies in 2023 and has nonrenewed thousands of policies.

- State Farm requested a 30% increase in June 2024, which has not been approved.

- Following the Eaton and Palisades fires in January 2025, State Farm filed for a 22% rate increase and was approved for a 17% increase on homeowners insurance policies.

- If the company wins the additional increase to 30% it’s still pursuing, homeowners in California will see an average increase of $600 a year.

However, the impact of natural disasters and severe weather on home insurance extends far beyond California’s wildfires and hurricanes that hit the Gulf Coast. Rates are skyrocketing even in places far from the coasts.

Severe convective storms, marked by high winds and large hail, cause cumulative losses in a year on par with a one-time hurricane event. Midwest states, like Minnesota, have seen a significant jump in rates as a result.

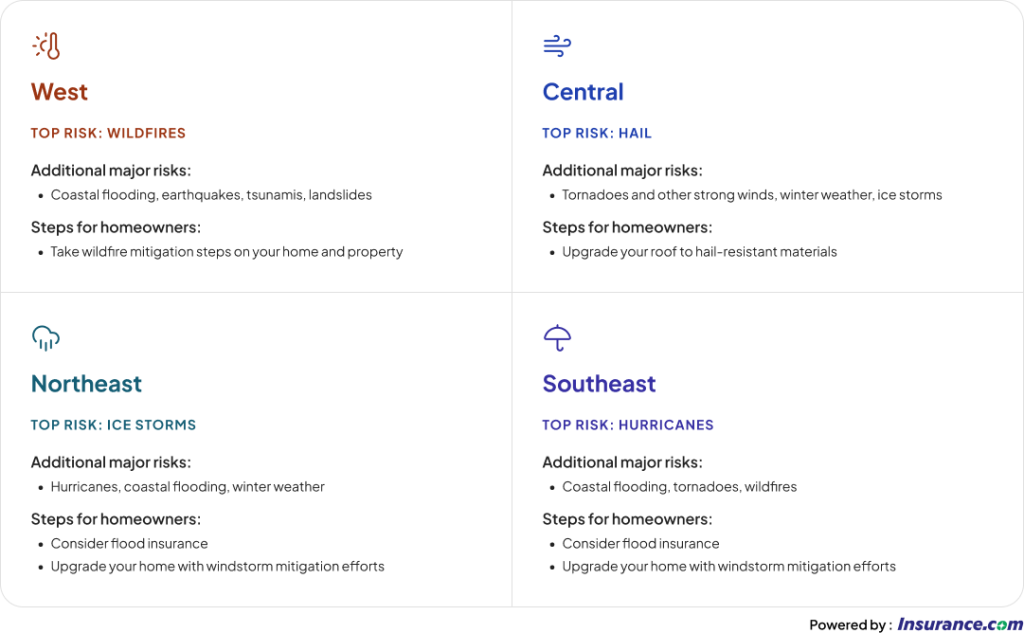

Home insurance challenges across the nation: Regional rate impacts

What’s most likely to raise your home insurance rates depends on where you live. While there are many areas of overlap, it’s good to know what risks are most likely to damage your home, so you can be prepared.

The future of home insurance: Where will rates get higher or lower?

Whether rates will continue to increase in 2026 and beyond depends on a lot of factors. For one, rate increases for which insurance companies have filed haven’t hit many homeowners yet, and some are still in the process of approval.

There are both some points in favor of home insurance rates stabilizing in 2026 and some factors that may still point to increases.

Rates may stabilize or even get lower due to:

- A quiet Atlantic hurricane season. Mainly impacting the Atlantic and Gulf coasts, the lack of any hurricanes making landfall in 2025 is likely to ease insurance companies’ loss ratios.

- Regulatory changes. A number of states are making efforts to better regulate insurance rate increases and minimize the impact of litigation on home insurance rates; Florida, where legislation has curbed frivolous lawsuits, is a good example.

- Previous rate increases. Rate increases over the past few years have pushed insurance company profits up, which makes it less likely they’ll need to file for additional increases.

On the other hand, rates may increase due to:

- Rate changes that haven’t hit yet. Rate changes that were approved haven’t necessarily reached consumers yet. The example of State Farm in California is just one area where increases are still on the horizon.

- Future natural disasters. An active hurricane or wildfire season in 2026 could put the brakes on any possible rate reductions and even drive rates higher. Tropical Storm Risk (TSR), a tropical storm tracking resource, predicts seven Atlantic hurricanes for 2026, three of which are predicted to be intense, but early forecasts are subject to change.

- Tariffs. While there has yet to be any significant reported impact on home insurance rates, tariffs on building materials (such as lumber from Canada) will raise costs and have the potential to drive additional rate increases.

This story was produced by Insurance.com and reviewed and distributed by Stacker.