How to find a gas credit card that actually pays off in 2026

The average American household spends over $2,400 a year on gas, according to data from the Bureau of Labor Statistics. That’s $201 a month just on gas. That's a big number — and it's also a big opportunity if you're using the right credit card every time you fill up.

Motley Fool Money has reviewed hundreds of credit cards with one goal in mind: helping people get more out of every dollar they spend. Since gas is one of the most consistent budget categories for most families, using the right gas rewards credit card can turn that routine spending into real money back in your pocket.

This guide walks you through exactly how to find a top gas credit card worth having — and how to actually get approved for one.

What is a gas credit card, exactly?

A gas credit card is any card that earns boosted rewards at gas stations. They're designed to turn every mundane fill-up into a small but steady win for your wallet.

There are two main types:

- Co-branded gas station cards — These are issued by a specific fuel brand (think Shell or Chevron). They can offer the highest per-gallon savings, but only at that brand's pumps.

- General rewards cards with gas categories – These are regular credit cards from the big issuers (Chase, Amex, etc.) that earn extra cash back or points whenever you pay at any gas station. They tend to be more flexible and often come with perks in other common spending categories, too, like groceries.

For most people, a general rewards credit card with a strong gas category wins on flexibility. But if you're fiercely loyal to one gas station and fill up there consistently, a co-branded card could edge it out on per-gallon savings.

How to find the best gas credit card for you

Everyone's driving habits are a little different — their commute, city, and favorite go-to stations. So the best gas card that works for you might not be the right fit for someone else.

Here's what matters most when you're comparing options:

1. The rewards rate on gas

Most basic credit cards earn a flat 1% back on everything — including gas. That's the baseline, and honestly, it's not great. Anything 3% or above is where things start to get genuinely interesting for rewards.

Some cards push as high as 5% back on gas, which, on real-world spending, can mean the difference between $20 a year in rewards and $100+.

2. Spending caps and annual fees

Some cards advertise a high rewards rate, but have sneaky limits attached to how much you can earn at the elevated rate. After a certain monthly or annual threshold, the rate might drop to a flat 1%.

It's worth doing a bit of homework on your actual gas spending before assuming a high rewards rate will hold all year.

On the fee side, a card charging $95 annually needs to return more than $95 in rewards to be worth it. Many strong gas cards carry no annual fee at all, which makes the math a lot easier.

3. Rewards on other spending

Many rewards cards are designed to match higher spending across several everyday categories, not just gas. Groceries, dining, and streaming are common ones — and if a single card pulls double or triple duty across your biggest expenses, that's an even better boost to your overall rewards.

4. How rewards are redeemed

Cash back is the simplest reward structure around. Rewards build up slowly over time, and when you're ready to use them, it's usually as easy as redeeming for a statement credit or a direct deposit.

Earning points or miles can be a little trickier. Some programs let you transfer points to airline or hotel partners for more value. Others lock you into a portal with limited options. If simplicity matters to you, a straightforward cash-back credit card usually wins.

5. Big box and warehouse memberships

If you already pay for a warehouse club membership (think Costco or Sam's Club), it's worth checking whether a co-branded credit card makes sense. Warehouse clubs often have some of the lowest per-gallon prices around, and pairing that with a credit card with a strong rewards rate on top can make for a genuinely hard-to-beat combination at the pump.

Are you self-employed or driving for work? A business card may pay off more

If you're a freelancer, small business owner, or someone who logs serious miles for work, a business credit card could unlock even better rewards on gas than a personal card. Business cards often come with higher earning rates, bigger welcome offers, and expense-tracking tools that make tax season a lot less painful.

Stacking gas station loyalty programs to maximize your savings

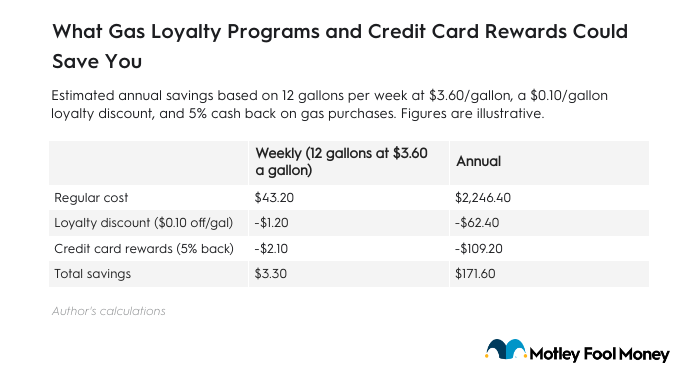

Many gas stations offer app-based loyalty programs that shave anywhere from $0.03 to $0.15 off per gallon, just for being a member.

These are typically free to sign up for and can stack additional savings on top of your credit card rewards.

Here's an example of what savings could look like in real life:

That's over $170 a year saved on gas — just by using the right rewards card and loyalty programs.

Of course, what you pay at the pump varies widely depending on where you live. Drivers in higher-cost states like California, Washington, and Hawai‘i are paying well above the national average — meaning their annual savings from stacking rewards could be significantly higher.

And with gas prices surging in March 2026 amid ongoing Middle East tensions, the case for swiping a rewards card has never been more timely.

How to get a gas credit card

Getting approved for a gas credit card follows the same process as any other credit card. Here's how to do it right.

Step 1: First, check your credit score

Most rewards cards require good to excellent credit (typically a 670+ FICO score). Check your credit score before you apply so you're not guessing. Many banks and credit unions offer free credit score access through your account dashboard.

Step 2: Decide what type of card fits your life

Co-branded station card or general rewards card? Cash back or points? Annual fee or no fee?

Nail down your priorities before you start browsing so you don't get distracted by offers that might not match your actual spending.

Step 3: Apply online

Most applications take less than 10 minutes. You'll need your Social Security number, annual income, and housing costs handy. Be sure to answer all the questions honestly and accurately — mistakes can delay your processing.

Most of the time, you'll get an instant decision. And if you're approved, you might be led to an online portal to set up app access.

Step 4: Download the mobile app

One of the best ways to track your rewards balance and monitor spending is by using the credit card issuer’s mobile app. It takes 60 seconds to set up and makes staying on top of your rewards a whole lot easier.

Step 5: Use your card every time at the pump

Once your new card arrives, make it your default card for gas purchases (and groceries, if the card earns rewards there too). The rewards add up fastest when the card is your automatic choice — not an afterthought.

The bottom line

Gas prices aren't getting any easier to stomach, and every dollar saved at the pump matters more than it used to. While you can't control what the price of gas does next week, you can control how you pay for it.

Swiping a rewards card instead of a debit card is one of the smallest habit changes you can make. It lets you claw a little money back from an expense that isn't going anywhere soon.

Stack a solid gas card with your local station's loyalty program, and you're doing more than most people ever think to do.

Frequently asked questions

Can I get a credit card just for gas?

Yes, it can be worth having a dedicated credit card just for gas purchases. Either a co-branded gas station card or a general rewards card can give you boosted rewards for gas purchases, and not replace your current everyday card. Many people carry 2-3 credit cards for exactly this reason.

Are gas credit cards worth it?

For most drivers, yes. If you're spending $200 or more per month on gas, a credit card earning 3%-5% back can return $72-$120 a year in rewards. You're spending the money anyway — may as well be rewarded for it.

Can gas credit cards build credit?

Absolutely. As long as you pay your balance in full and on time, a gas credit card reports to the major credit bureaus just like any other credit card and can help strengthen your credit history over time.

Are gas station credit cards good?

They can be — if you're loyal to one brand and fill up frequently. But if they have higher annual fees, the net benefit might actually be nonexistent, or even negative. The biggest trade-off with a co-branded card is limited usability everywhere else.

This story was produced by Motley Fool Money and reviewed and distributed by Stacker.