From marathons to mountaineering: Ranking which sports and hobbies affect life insurance the most

Extreme sports and high-risk hobbies can double your life insurance premium or result in a denial — but specialty insurers, independent brokers, and strategic timing can make affordable coverage possible even for the highest-risk activities.

You could be the healthiest person your doctor has ever seen — perfect bloodwork, no vices, runs marathons on weekends. But if you also happen to jump out of planes or scale mountains in your spare time, life insurance companies are going to see you very differently.

Risky hobbies affect life insurance rates because they change the statistical likelihood of a claim. The more dangerous your activity — and the more often you do it — the higher your premium. In some cases, insurers may decline to cover you altogether.

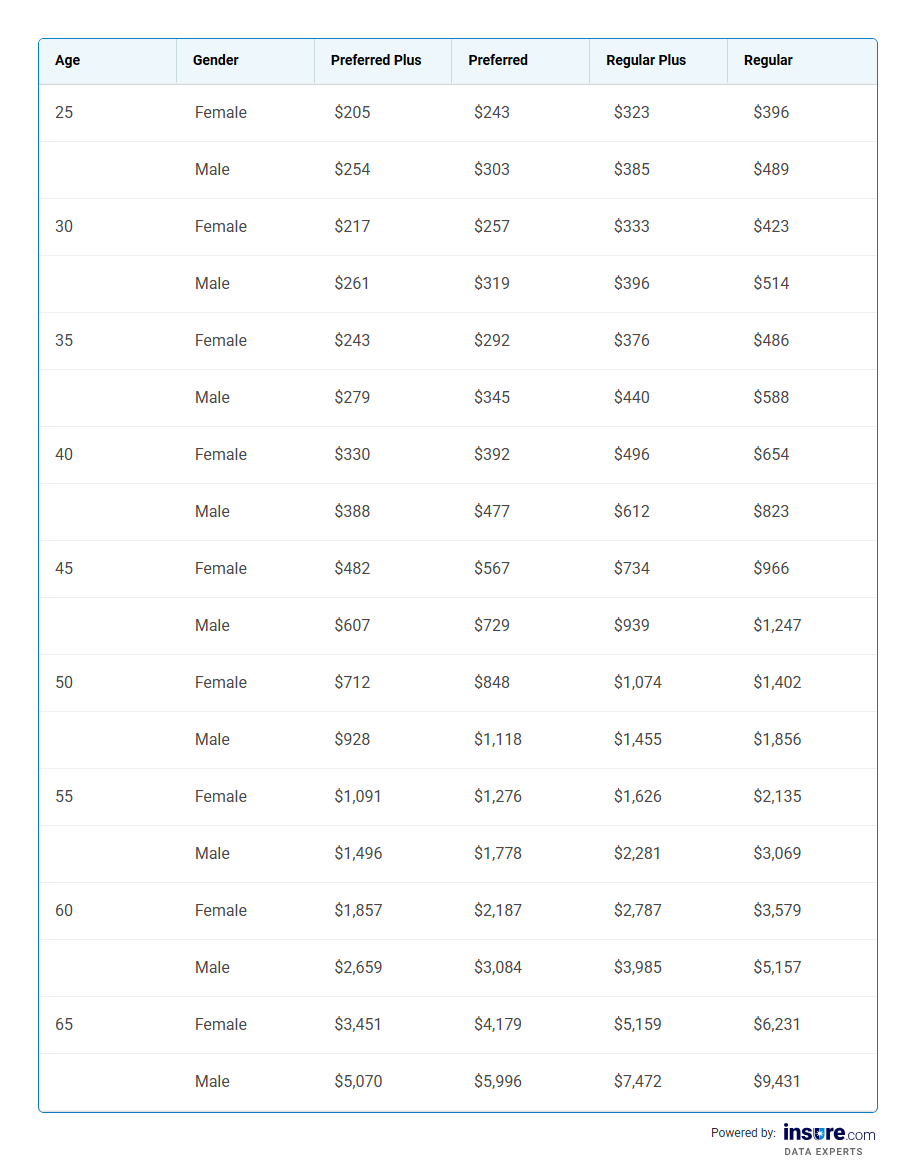

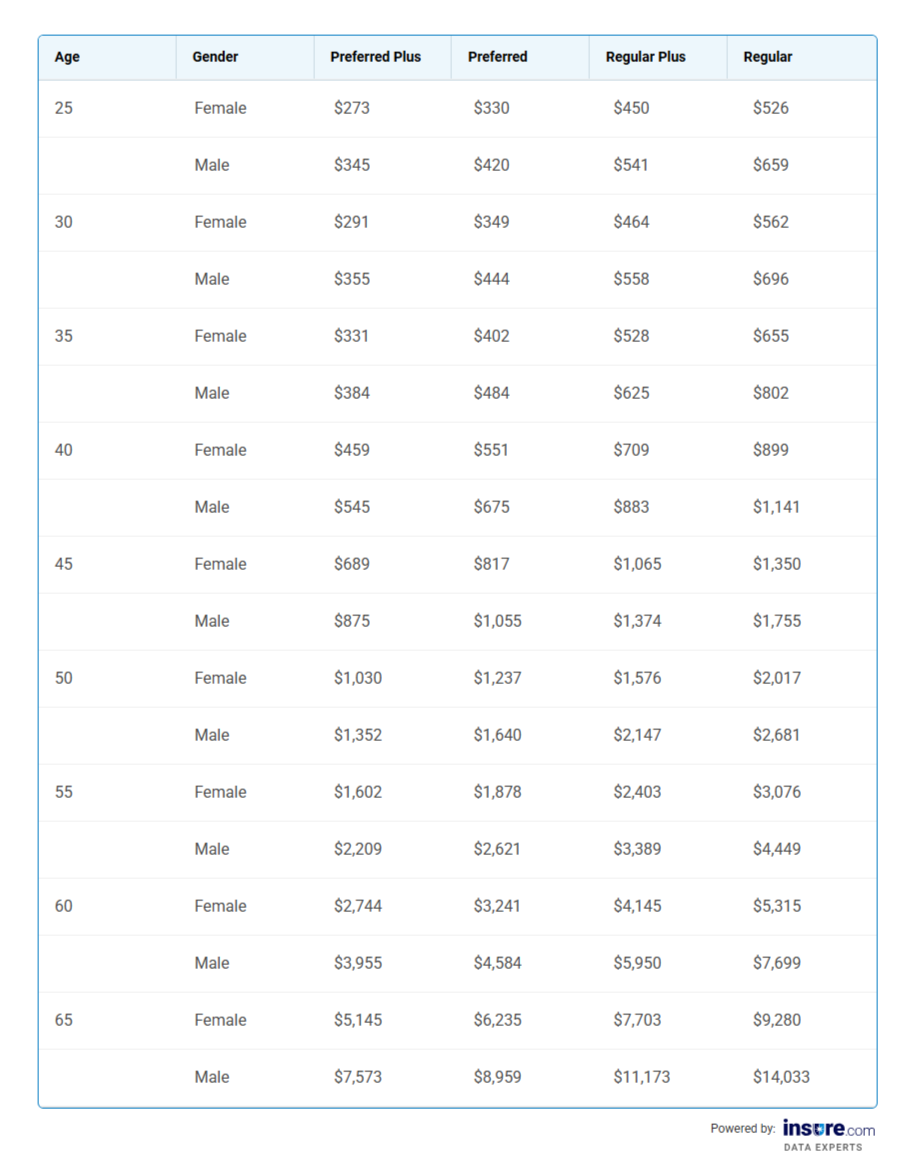

A 25-year-old female could lock in $273 per year for $750,000 in coverage at Preferred Plus rates. A high-risk hobby could push that to $526 at Regular rates — nearly double, and a difference of more than $5,000 over a 20-year term.

A higher premium isn't inevitable. Specialty insurers, independent brokers, and strategic timing can all help adventurous applicants find competitive coverage — even for the highest-risk activities.

Insure.com explores how high-risk hobbies affect life insurance premiums and how applicants can find competitive coverage.

The short version, if you're in a hurry

Risky hobbies can double your life insurance premium — but they rarely make coverage impossible. Here's what matters most:

- Your activity's frequency matters more than the activity itself. A one-off skydiving trip is treated very differently from jumping every weekend.

- Honesty is non-negotiable. Misrepresenting your hobbies can result in a denied claim — the worst possible outcome for your family.

- Rates are locked in when you buy. Quitting a hobby after your policy starts won't lower your premium. Likewise, starting a risky hobby after you already have coverage in place shouldn’t affect your policy.

- Specialty insurers exist for high-risk applicants. If one insurer declines you or quotes you sky-high rates, others may not.

- An exclusion rider is a viable backup. If affordable coverage isn't available, a policy that excludes your hobby is almost always better than no policy at all.

Why do life insurance companies care about your hobbies?

Life insurance companies are in the business of calculating risk and making profitable choices. When they insure someone, they are betting that they will collect more in premiums than they will pay out in claims. If you have a dangerous hobby, the risk of a claim rises — and along with it, your insurance rates.

Basically, if you regularly participate in an activity that statistically increases your odds of an early death, life insurance companies are going to adjust your rates accordingly.

Insurers use four life insurance rate tiers, though the names of these tiers may vary from company to company. The following range from those with the best rates to standard rates:

- Preferred Plus

- Preferred

- Regular Plus

- Regular

Preferred Plus rates are reserved for the healthiest people with no high-risk factors. Meanwhile, those with Preferred rates are healthy with only minor risk factors. Most people who engage in high-risk activities or extreme sports will fall into the Regular Plus or Regular tiers, with Regular rates reserved for those with the highest risk profiles.

Some activities might result in only a slight shift in rates, such as from Preferred to Regular Plus. Others might be deemed so risky that they drop you from Preferred Plus to Regular.

“Different carriers look at different activities as less or more of a risk,” says Daniel Hochler, managing associate with Forest Hills Financial Group in Melville, New York.

If an insurer deems your hobby too risky, it may be possible to request an exclusion rider. This provision means the life insurance company will not pay a claim for a death resulting from the excluded activity.

How life insurers calculate risk for dangerous hobbies

Being active isn't the problem — it’s what you're doing that matters. BASE jumping and marathon running are both physical activities, but the risk of death couldn't be more different. Insurers price accordingly.

The same logic applies to how often you participate. Someone who went skydiving once on a birthday trip has a very different risk profile than someone who jumps every weekend. If your hobby falls somewhere in the middle — recreational skiing, the occasional scuba dive, a cycling race on weekends — you may be surprised how little it affects your rate.

What insurers are really looking at is the statistical likelihood of a claim, factoring in not just the activity itself, but how often you do it, at what level, and whether you have proper training or certification.

The ranked list: Which sports and hobbies affect life insurance the most?

Life insurance for extreme sports enthusiasts works differently from standard policies. Insurers evaluate hobbies during underwriting, and activities like skydiving, BASE jumping, and motor racing can push your premiums higher — or disqualify you from certain coverage types altogether.

Every life insurance company will have its own policies and guidelines, but here’s what you might expect when it comes to life insurance for athletes in extreme sports.

How much more does a risky hobby actually cost you?

If you participate in extreme sports or high-risk activities, your life insurance premiums could be significantly higher than average — or even double what someone in better health pays. The gap between Preferred Plus and Regular rates can run into hundreds of dollars per year, and over a 20-year term, that difference compounds into thousands.

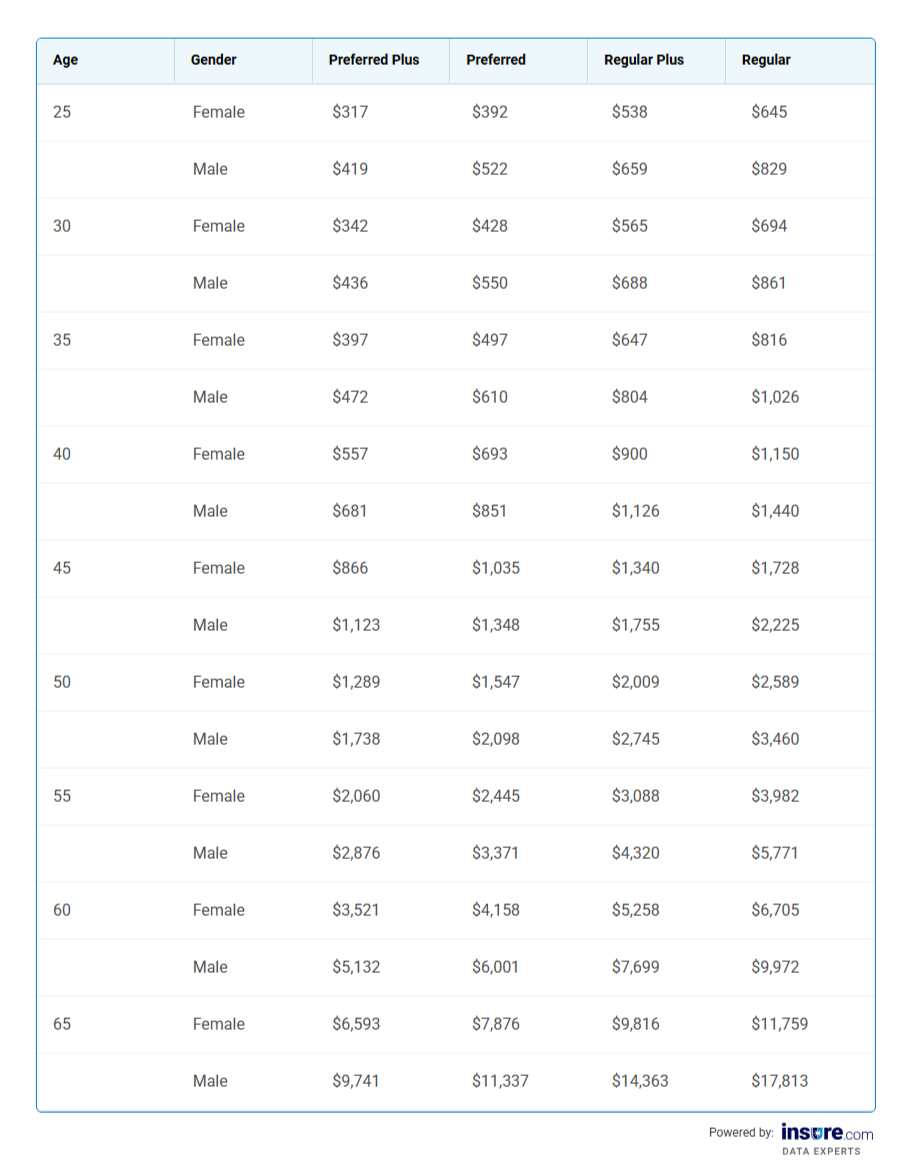

For example, a 40-year-old male paying $545 per year at Preferred Plus rates for $750,000 in coverage could pay $1,141 per year at Regular rates — a difference of $596 annually, or nearly $12,000 over a 20-year term.

The tables below show how premiums shift across all four tiers. Rates are based on a 20-year term policy for a nonsmoker in California. Across all age groups and coverage amounts in the tables below, Regular rates are approximately twice the cost of Preferred Plus rates for the same policy, and the gap widens significantly as you get older.

Rates vary by state and health profile, so compare life insurance quotes for a personalized estimate.

$500,000 in coverage

$750,000 in coverage

$1,000,000 in coverage

How do life insurance companies actually find out about your hobbies?

Life insurance companies find out about your hobbies by asking directly on the application — and then verifying your answers through third-party data sources, medical records, and public information. Lying on your application is not worth the risk. If an insurer discovers a misrepresentation, they can deny your family's claim or cancel your policy entirely.

Being upfront — even if it means a higher premium — protects your family when it matters most. A denied claim costs far more than the difference in rates.

What questions will you be asked on the application?

Life insurance applications typically have at least one question in the lifestyle or medical section that asks if you participate in any hazardous recreational activities. Some applications may ask about specific activities while others may be more open-ended.

“Once you answer yes, they will ask follow-up questions,” says Brandon Norwood, a financial planner with Oak City Financial, a virtual advisory firm serving clients nationwide.

Those follow-up questions may include any of the following:

- How often do you participate in the activity?

- At what level do you participate?

- Do you have certifications?

- Do you compete professionally?

- What equipment do you use?

The more questions you receive about your hobby, the more you can guarantee that it matters to the underwriter — and your rates.

Can insurers verify your hobbies without you telling them?

Insurers have several ways to cross-check your application — even without you volunteering the information. Medical records, public records, and third-party databases can all reveal details about your lifestyle and risk profile.

One of the most significant tools is the MIB (Medical Information Bureau), a shared database used by insurers to flag inconsistencies across applications. If a previous insurer denied you coverage due to high-risk recreational activities, that information may already be on file — and your next insurer can access it.

What happens when your insurer won't cover your hobby — and what to do about it

If an insurer considers your hobby too risky to cover at a standard rate, it may offer you a life insurance exclusion rider rather than declining your application outright. Think of it as a middle-ground option: the insurer agrees to cover you, but with one specific carve-out — it won't pay a claim if your death is directly caused by the excluded activity.

So if you have a skydiving exclusion and die in a skydiving accident, your beneficiaries wouldn't receive the death benefit. But if you died from an illness, a car accident, or any other unrelated cause, the policy would pay out normally.

Whether to accept an exclusion rider comes down to your alternatives. If you can't find affordable coverage elsewhere — or if you've scaled back the activity in question — it's often worth taking. For most people, the risk of dying specifically from their hobby is far lower than the risk of dying from something else entirely. Some coverage is almost always better than none.

Exclusion riders don't have to be permanent, either. If you give up the high-risk activity, you may be able to request its removal. Ask your insurer or broker upfront what is needed to approve that — typically some documented period of inactivity — so you already know the path forward if your circumstances change.

What happens if you take up a risky hobby after your policy starts?

Your life insurance rate is locked in at the time of your application. If you take up a risky hobby after your policy is issued, your existing coverage and premiums are generally unaffected — the insurer can't reprice you mid-policy.

Where it gets complicated is if your policy lapses or you apply for new coverage. At that point, your current activities become fair game for underwriting, and your rates could be significantly higher.

One important caveat: some policies include a duty-to-notify clause that may require you to inform your insurer of certain lifestyle changes. Check your policy documents or ask your agent if you're unsure whether this applies to you.

How can athletes and adventurers get the best life insurance rates?

Don’t be discouraged if you are athletic or adventurous. You can still save on life insurance by working with an experienced broker, shopping specialty providers and timing your application strategically.

Follow these steps to save even if you have a high-risk hobby.

- Find the right insurer. Some companies specialize in insuring athletes and hobbyists that other insurers might decline.

- Work with an independent broker. An experienced broker can be the key to finding these specialty insurers who would be happy to provide you with life insurance coverage.

- Get certified. If your hobby or sport offers safety training or certification, complete it and include the documentation with your application.

- Time your application. If you are taking a season or year off from your activity, that might be the best time to apply.

- Compare quotes. Not every insurer defines risky activities in the same way. Get quotes from three to five carriers to see how much you can save with different companies.

- Consider an exclusion rider. Ask about excluding coverage of your hobby or sport if you are unable to find affordable coverage. While not ideal, a policy with an exclusion rider is better than no life insurance at all.

- Wait to start a new hobby. You can’t lie on your life insurance application — that would be fraud. But if you start a new hobby after your life insurance is in effect, it shouldn’t change your coverage or rates. Just don't rush into it: if you're scaling a mountain three days after your policy was approved, a resulting claim is going to raise eyebrows. Insurers can — and do — contest payouts if they suspect you had plans to take up the activity when you applied.

“There are certain carriers that specialize in high-risk sports,” Norwood says. “That’s their bread and butter; that’s their niche.”

Your hobby doesn't have to define your coverage

A high-risk hobby complicates a life insurance application, but it doesn't end it. Millions of skydivers, rock climbers, pilots, and motorsport enthusiasts carry life insurance.

The most effective move is working with an independent broker who specializes in high-risk coverage — they know which carriers treat specific activities most favorably and can save you significant time finding them.

Timing and preparation also help. Applying during a season off from your activity, or after completing a safety certification, can improve how an underwriter evaluates your application. If affordable coverage still isn't available, an exclusion rider is a legitimate path forward — a policy that excludes your hobby still covers everything else, and some coverage is almost always better than none.

Whatever route you take, be honest on your application. Insurers investigate claims, and a misrepresentation can cost your family the payout when they need it most.

Frequently Asked Questions

Does running marathons affect life insurance rates?

Typically, no. Marathon running is generally considered a low-risk activity and may be viewed by insurers as a sign of a healthy lifestyle. That could work in your favor by improving your life insurance rate tier. Ultra marathons, such as 24-hour races, may be viewed as risky by some underwriters.

Can I be denied life insurance because of a hobby?

Yes, extreme hobbies such as BASE jumping, skydiving and high-altitude mountaineering could result in your application for life insurance being denied. If you are denied because of a hobby, you may be able to request an exclusion rider, which would eliminate coverage for a death related to that activity.

What if I stop the risky hobby after getting coverage?

Generally, you are locked into the rates you receive at the start of a policy. You could notify your insurer and ask for a rate review. If they don’t offer that option, you could compare life insurance quotes and see if it would be cheaper to buy a new policy than keep your existing one.

Do all insurers treat hobbies the same way?

No, life insurance companies have their own underwriting guidelines. One might say skydiving is automatic grounds for a denial, while another may give the occasional skydiver Preferred rates. Work with an independent insurance broker to find the companies that will look most favorably on your hobby.

Does age affect how my hobby is rated?

Yes, age is a prime factor used by insurance companies. An insurer might see scuba diving at age 50 as riskier than scuba diving at age 30. The earlier you apply, the better your chances of finding affordable coverage.

Can insurers find out about my hobbies if I don't disclose them?

Yes, insurers can review medical records and MIB reports when evaluating an application. A bigger risk is if you die while participating in an undisclosed high-risk hobby or extreme sport. The life insurance company may investigate, and if it discovers you were participating in the activity at the time of your application, it could deny your family’s claim.

Does a risky occupation affect rates the same way a hobby does?

Yes, although insurers categorize occupations and hobbies differently. A pilot who flies recreationally in their free time might be considered to have both a high-risk occupation and a hobby, doubly affecting their life insurance premiums.

Methodology

Premium rates cited in this article were obtained from Compulife in March 2026. Quotes reflect 20-year term life insurance policies for nonsmokers in California across three coverage amounts: $500,000, $750,000, and $1,000,000. Rates are displayed across all four standard underwriting tiers — Preferred Plus, Preferred, Regular Plus, and Regular — for male and female applicants at multiple age points.

Rate tiers reflect the underwriting classifications most commonly used by life insurers; actual tier names vary by carrier. Quotes are intended to illustrate how premiums shift across risk profiles and should not be interpreted as guaranteed offers. Actual rates will vary based on individual health history, state of residence, insurer, and underwriting guidelines at the time of application.

This story was produced by Insure.com and reviewed and distributed by Stacker.