Medical school debt and refinancing: How borrowers are managing student loans

For health care professionals at all levels, from medical students to attending physicians, student loan debt is as pervasive as the common cold. Unfortunately, it takes a lot longer to go away. Severe student loan debt can affect borrowers’ financial health for years or even decades.

This spring, SoFi surveyed 229 medical professionals across the career spectrum to ask about their loan-related aches and pains. As SoFi reports below, many hope a student loan refinance can bring them some relief.

Key Findings

- More than 61% of respondents carry student loan debt of more than $100,000, showing that high debt burdens persist even as professionals advance in their careers.

- At least half of respondents at every career stage owe $50,000 or more.

- Most respondents’ debt currently involves interest rates between 5.00% and 7.99%.

- Borrowers who want to refinance student loans are most often motivated by a desire to lower interest rates, a goal shared by nearly half (45%) of respondents.

- Most respondents are confident that refinancing student loans could save them money over the long term.

Introduction to Medical School Debt and Refinancing

In SoFi’s survey, more than one-quarter (27%) of respondents are medical students and early-career doctors known as residents. About 10% are attending physicians, while almost half (45%) are “other health professionals,” a broad category made up of nurses, dentists, therapists, and other related practitioners.

Almost all of these health care workers have financed their many years of schooling by borrowing. Due to the financial strain, they’re thinking about student loan refinancing for some or all of this debt.

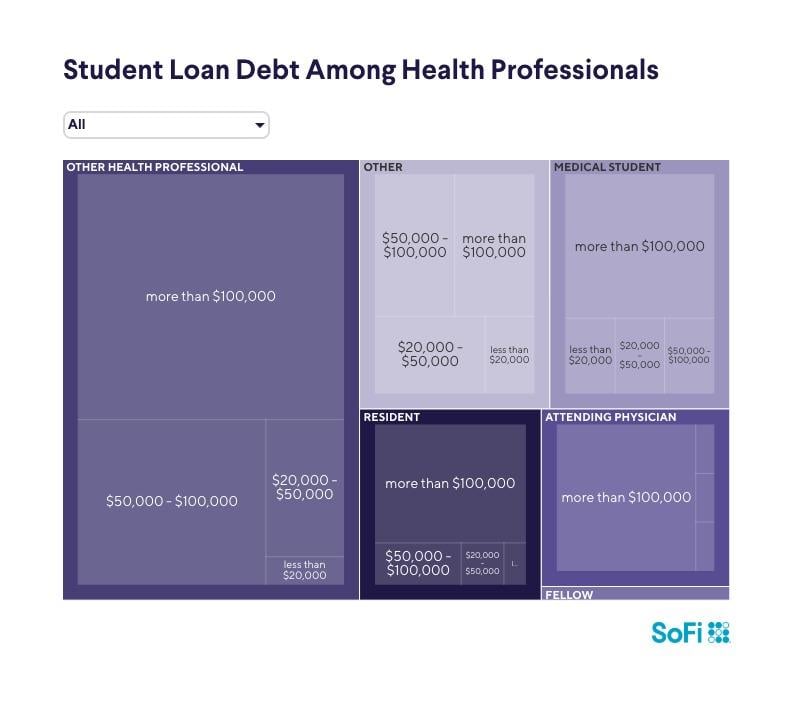

Most Borrowers Are Not Early-Career Health Care Professionals

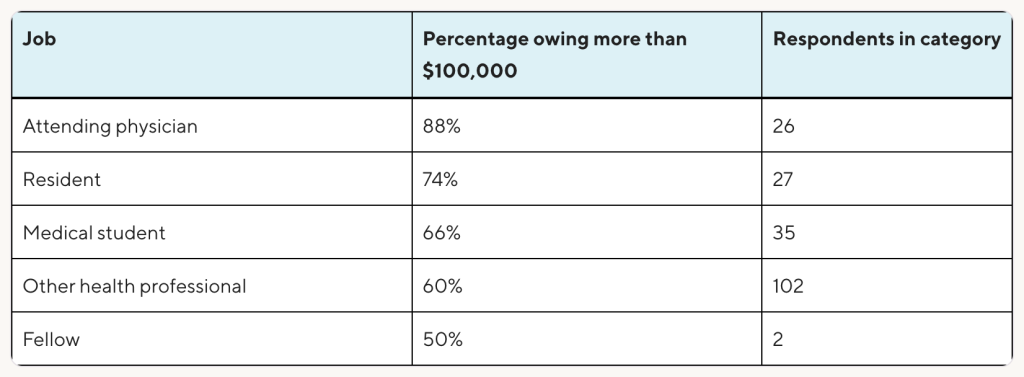

At first glance, you might expect early-career health care professionals to be carrying more medical school debt than full-fledged doctors do, since they haven’t had as much time in the workforce to earn money and pay back their loans.

But SoFi’s survey found otherwise. Among medical students, only two-thirds (66%) owe more than $100,000. Almost three-quarters (74%) of residents owe that much. And almost 9 out of 10 (88%) attending physicians carry a six-figure debt. Other health professionals — people who may not have medical degrees — also carry a great deal of student loan debt. There’s no indication of how long these borrowers have been out of school, but as a group, their debt load is comparable to that of residents: 89% of residents and 88% of other health professionals owe at least $50,000.

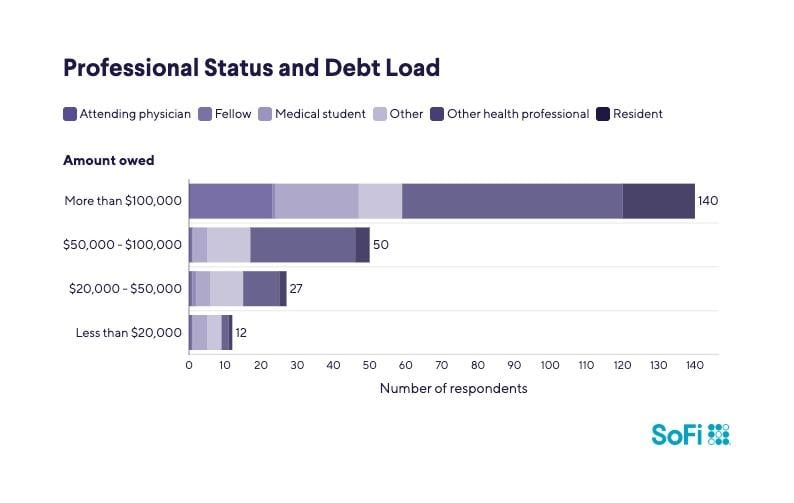

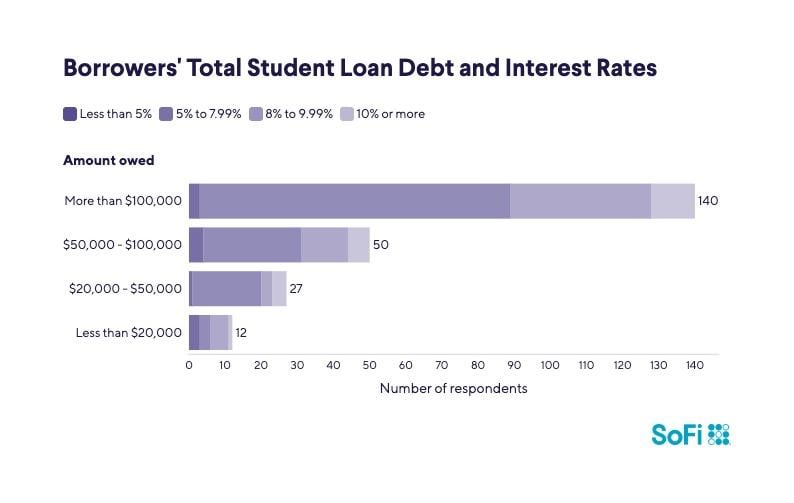

The Majority of Borrowers Carry Over $100,000 in Student Loan Debt

Regardless of career stage or role, more than three-fifths (61%) of all survey respondents have medical student loans in excess of $100,000. More than four out of five (83%) owe at least $50,000.

As shown below, there is a correlation between debt load and professional status. It’s worth noting that at least half of the respondents within each category owe more than $100,000.

Most Borrowers Have Interest Rates Between 5.00% and 8.00%

Though student loan rates have fluctuated dramatically over the past decade — even dipping below 3.00% during the COVID-19 pandemic — most borrowers in the survey are facing rates above 5.00%.

The vast majority of them (85%) pay rates between 5.00% and 10.00%.

Most — almost 3 out of 5 (59%) — pay interest ranging from 5.00% to 7.99%, while a sizable minority (26%) pay 8.00% to 9.99%. Only 1 in 20 respondents pays interest of less than 5.00%.

Many of these borrowers may be able to bring down their average rates by student loan consolidation or refinancing.

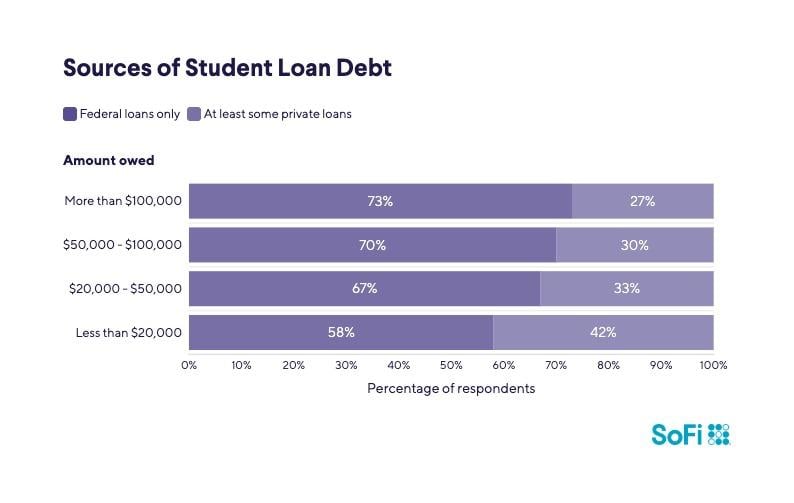

Federal Loans Make Up the Majority of Borrower Debt

It’s not surprising that Uncle Sam is the most frequent provider of medical school loans. What’s notable is the degree to which those government-sponsored loans overshadow private ones.

Almost 9 out of 10 respondents (86%) have at least some federal loans — and roughly 7 out of 10 (69%) say their student debt is nothing but federal loans.

Of the 159 respondents who borrowed exclusively from the government, 110 (or 69%) pay interest rates between 5.00% and 7.99%. Almost all pay less than 10.00% for the loans.

At all levels of indebtedness, private loans are less prevalent. The survey found that as debt grows, the share financed by private lenders shrinks.

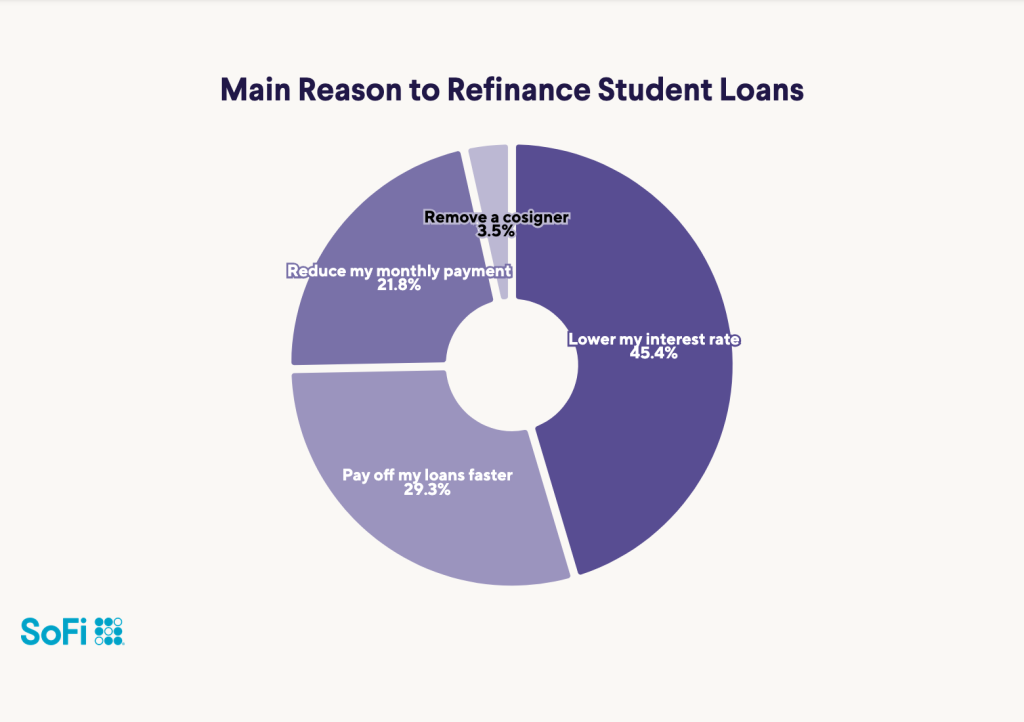

Lowering Interest Rates Is the Primary Goal for Refinancing

Refinancing at a lower APR (annual percentage rate, which includes interest and any account fees) can often ease the process of paying down longstanding loans. Smaller monthly payments — or the ability to direct a larger share of existing payments to principal rather than interest — can have a big impact.

Among survey respondents, almost 3 in 10 (29%) say they want to refinance student loans in order to pay off the debt faster, while about 1 in 5 (22%) would do so to reduce their monthly payments.

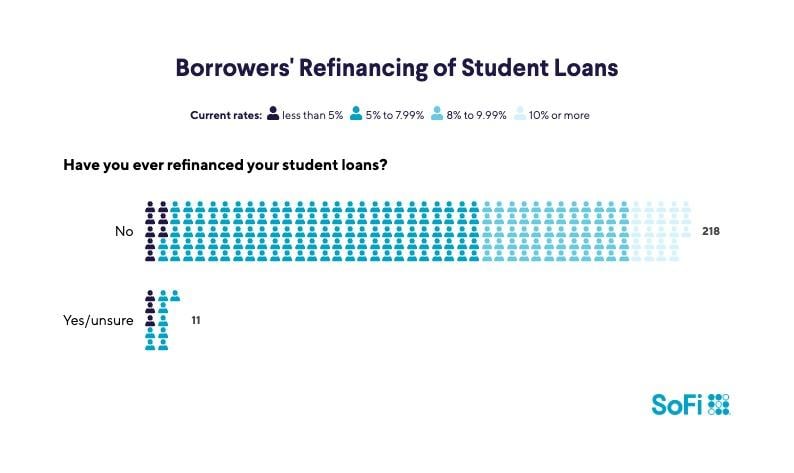

Most Borrowers Have Not Refinanced Their Loans Before

Of the 229 respondents, the vast majority (218, or 95%) have not previously refinanced their medical student loans. About 38% of them pay an average interest rate of more than 8.00%. By contrast, everyone who has refinanced pays less than 8.00%.

To be sure, not everyone who refinances will reduce their interest rates. But those with strong credit scores, solid payment histories, and accommodating lenders may well secure lower student loan refinancing rates that represent real savings.

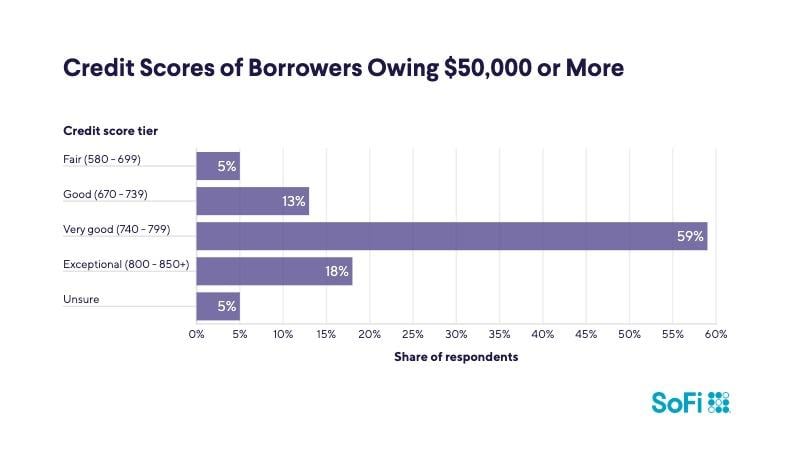

Most Borrowers Have Strong Credit Profiles

Most respondents to the survey (59%) report they have “very good” credit. This label generally equates to credit scores ranging from 740 to 799. Within that credit score tier, more than two-thirds of people (68%) have student loan debt in excess of $100,000.

Of the 18% with “exceptional” credit scores (800 or higher), almost 3 in 5 (59%) owe more than $100,000.

Meanwhile, within the group of borrowers who owe at least $50,000, more than three-quarters (77%) have very good or exceptional credit scores.

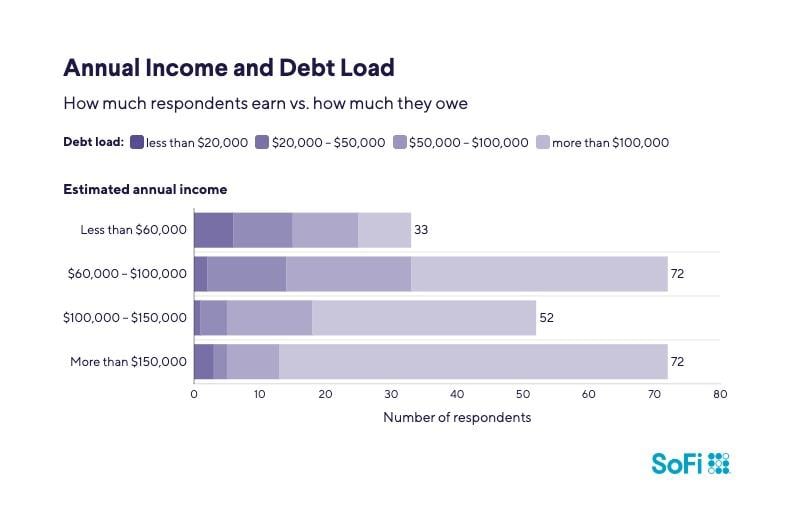

Borrowers Span a Wide Range of Income Levels

For established professionals, many health care positions pay well. Depending on the field and the role, median pay can range well into six figures. But students and residents generally haven’t entered their prime earning years yet. Their participation in the survey helps explain the wide range of annual incomes shown in these results.

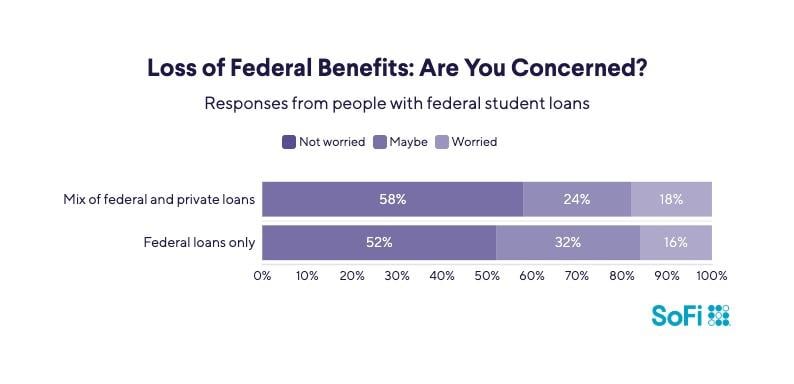

Most Borrowers Are Not Concerned About Losing Federal Benefits

When federal student loans are refinanced with a private lender, borrowers lose important federal benefits, such as income-driven repayment, deferment, and access to Public Service Loan Forgiveness. Overall, more than half (57%) of borrowers in the survey say they’re not concerned about the loss. That could be because they don’t foresee utilizing those programs, or they feel the advantages of refinancing outweigh the drawbacks.

More than two-thirds (69%) of respondents have all federal student loans. Within that group, 52% are confident about the loss of benefits, while 16% are definitely concerned.

Among the 17% who have a combination of federal and private loans, 58% are confident that giving up federal benefits is the right decision, while 18% are worried.

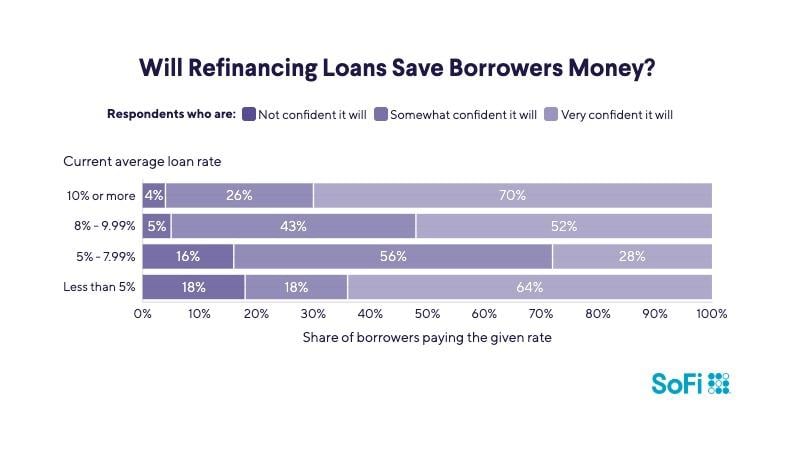

Borrowers Are Generally Confident Refinancing Will Save Money

Almost 9 out of 10 borrowers (88%) report they’re somewhat or very confident that refinancing their student loans now will enable them to save money in the long term.

Of the roughly 10% of respondents paying 10.00% interest or more on their loans, almost all (96%) believe that refinancing will save them money.

At the other end of the spectrum, a tiny share of respondents (5%) are paying rates of less than 5.00%. Most of them (82%) are also confident they’d see some savings after refinancing.

The Takeaway

Health care professionals are servicing their medical school debt at all income levels, grappling with a wide variety of interest rates. Many are repaying six-figure sums. Though few have refinanced their loans in the past, almost all believe that doing so now could save them money in the future.

Methodology

Survey findings reflect the answers of 229 people who answered a SoFi.com online quiz from 2026. All dollar amounts and interest rates are self-reported. Percentages may not total 100 due to rounding.

This story was produced by SoFi and reviewed and distributed by Stacker.