As rate cuts loom, retirees rethink income strategy

When interest rates move, markets react in seconds. Retirees feel the impact over months and years.

After the fastest series of rate hikes in decades, attention has shifted to when the Federal Reserve might begin cutting rates. For investors, it is part of the economic cycle. For retirees living on a fixed income, it can feel far more personal.

A new survey from John Stevenson highlights that tension: 74% of retirees believe the Fed’s rate decisions primarily benefit Wall Street rather than average retirees.

As this article from John Stevenson reveals, the results show that interest rate decisions are closely linked to retirees’ sense of financial stability.

Key Findings

- 40% of retirees rarely or never follow news about the Federal Reserve’s interest-rate decisions.

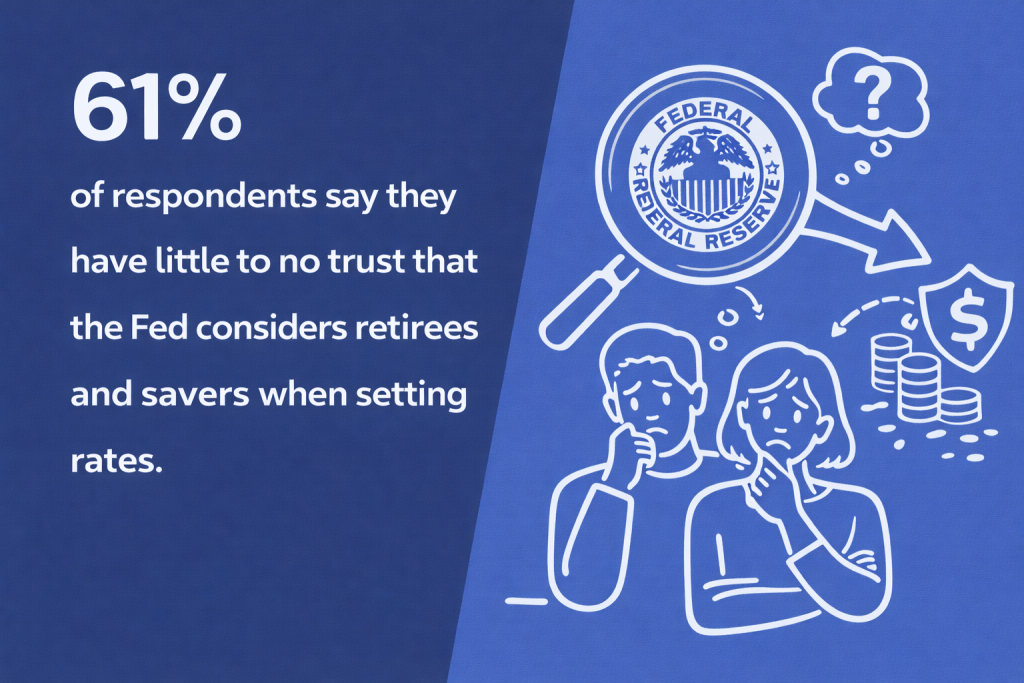

- 61% have very little to no trust that the Fed considers retirees and savers when setting rates.

- 58% say lower interest rates are detrimental to people who have saved responsibly.

- 45% fear inflation will outpace their income if rates fall and yields decline.

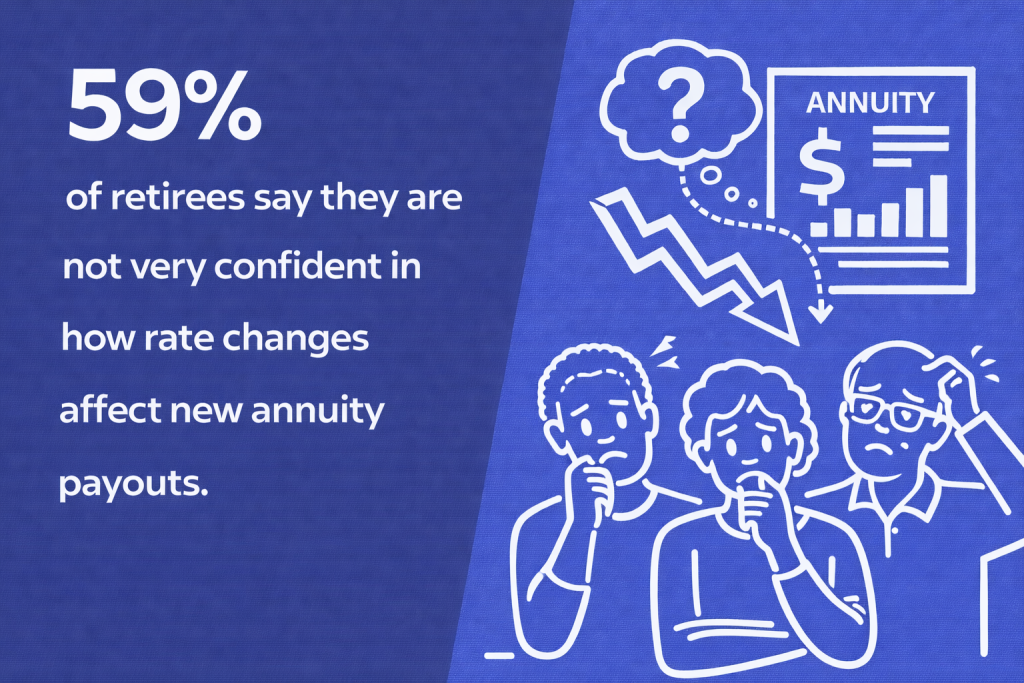

- 59% are not confident they understand how interest-rate changes affect new annuity payouts.

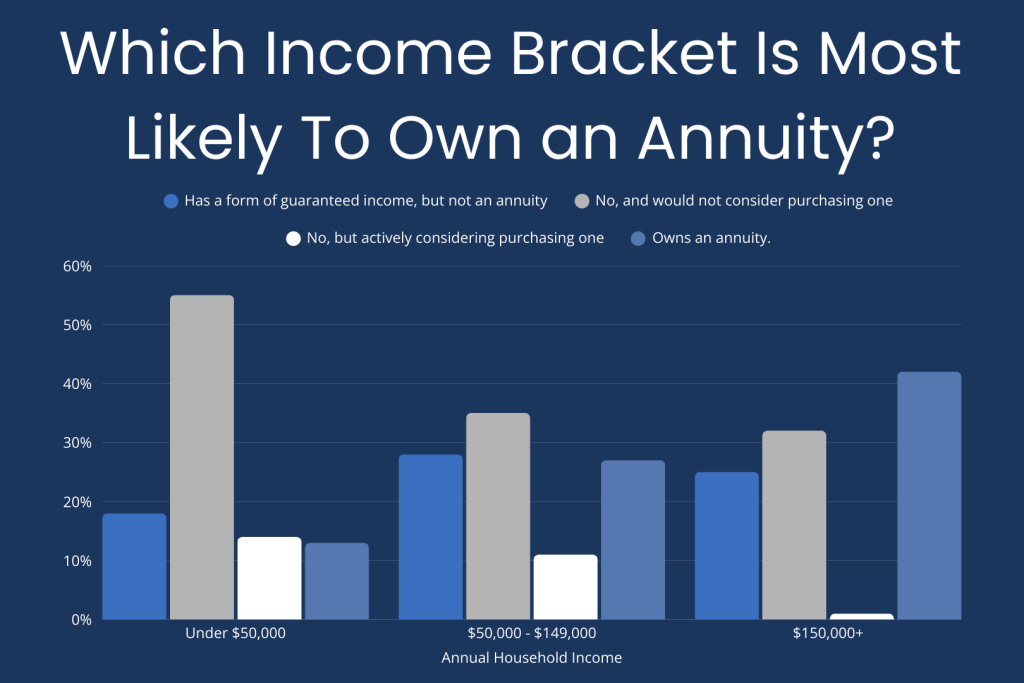

- Among retirees earning $150,000 or more, 42% own an annuity.

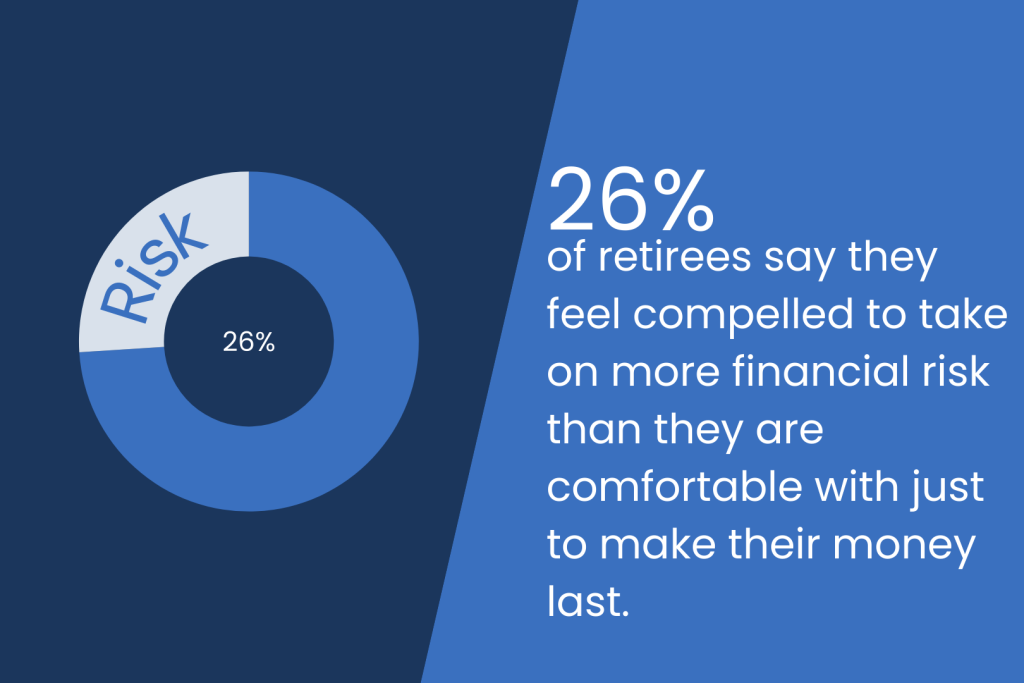

- 26% feel compelled to take on more risk than they are comfortable with to make their money last.

A Growing Trust Gap Around Federal Reserve Policy

Many retirees are not closely watching Fed announcements. In fact, 40% rarely or never follow rate decisions. Still, that distance does not mean they are unconcerned.

61% say they have little to no trust that the Fed considers retirees and savers when setting rates. That perception matters.

The past few years have been unusually volatile. After a long stretch of near-zero rates, the Fed raised rates at the fastest pace in decades to fight inflation. Now, markets are watching for potential cuts. Rapid policy swings can make retirement planning feel unstable, especially when income strategies are built to last decades.

Why Lower Interest Rates Feel Like a Setback for Savers

Lower interest rates can stimulate borrowing, but for retirees, they often mean smaller income streams.

When rates decline, newly issued CDs and Treasuries typically offer lower yields. Retirees who locked in strong returns last year may face noticeably smaller payouts when reinvesting.

That helps explain why 58% of retirees say lower interest rates hurt people who saved responsibly. Many spent years building conservative portfolios designed to generate stable income, and falling yields disrupt that expectation.

Inflation compounds the worry. While price growth has cooled from recent peaks, everyday expenses remain higher than they were a few years ago. Nearly half, 45%, fear inflation will continue to outpace income gains if rates fall.

Without employment income to offset rising costs, small yield changes can have outsized effects on monthly budgets.

Annuity Timing and Interest Rate Uncertainty

Interest rates directly influence annuity payouts. Prospective buyers often review projected income scenarios using annuity calculators to understand how different rate environments may affect payouts. As rates climbed in recent years, payouts improved, drawing attention to the importance of timing.

Even so, understanding remains limited. 59% of retirees say they are not very confident in how rate changes affect new annuity payouts. Among female retirees, that figure rises to 65%.

Annuities come in many forms, including fixed and indexed structures. For some retirees, the range of choices creates hesitation. 39% cite selecting the wrong annuity product and regretting the decision as their greatest concern.

Timing adds another layer. One in five Gen X retirees (20%) say they would wait several months if they believed payouts might increase within the year. That reflects a growing awareness that interest rate policy can shape long-term guaranteed income.

Changes in interest rates can influence when retirees choose to lock in guaranteed income.

Income Differences Shape How Rate Cuts Land

Interest rate changes do not affect all retirees the same way.

Among retirees earning $150,000 or more, 42% own an annuity. Just 9% of this group say none of their income comes from interest or dividends, compared to 53% of retirees earning under $50,000.

Higher-income households tend to hold more interest-sensitive assets. For retirees evaluating how a lump sum might translate into monthly income, reviewing example payout scenarios at different investment levels can provide useful context. That makes them more responsive to rate shifts.

Recent years have seen record inflows into high-yield money market funds during periods of elevated rates. Reflecting that pattern, 25% of higher-income retirees report moving more money into CDs, Treasuries, or money market funds in the past year.

If yields fall, behavior may shift again. 30% say they would move into higher-risk investments if safe income were to drop.

The Pressure to Take More Risk in Retirement

Retirement income has changed over time. Traditional pensions have declined, and many households now rely on personal savings, Social Security, and defined contribution plans.

Social Security data shows that Americans are living longer than previous generations, extending the average length of retirement. Healthcare remains one of the largest unpredictable expenses. As each year passes, income stability tends to become a greater priority over time in retirement.

Still, 26% of retirees say they feel compelled to take on more financial risk than they are comfortable with just to make their money last.

The data suggest an ongoing tradeoff between stability and return. Retirement is meant to reduce uncertainty. Yet rate shifts and inflation pressures can make conservative strategies feel less secure.

When Monetary Policy Meets Retirement Reality

The Federal Reserve sets interest rates to guide inflation and economic growth. Retirees experience those decisions in more personal terms.

For many, interest rates influence income built over decades of disciplined saving. When rates rise or fall quickly, that income can shift in ways retirees cannot control.

Financial markets interpret rate cycles through economic indicators. Retirees experience them through changes in income.

That difference helps explain the survey’s findings.

Methodology

To understand how Americans approach interest rate policy and retirement income decisions, John Stevenson surveyed 1,000 retirees across the country via Pollfish in February 2026. Participants answered a series of questions about their views on Federal Reserve rate changes, annuities, fixed-income strategies, and financial risk in retirement. Responses were analyzed by income, age, and gender to identify trends, differences, and areas of uncertainty.

This story was produced by John Stevenson and reviewed and distributed by Stacker.