SpaceX stock: 7 things every investor should know ahead of the SpaceX IPO

The newly unveiled Space Exploration Technologies (SpaceX) S-1 registration statement delivers essential financial disclosures that potential investors must scrutinize before considering buying SpaceX stock. This filing officially lifts the veil on SpaceX's financials, detailing everything from its rapid Starlink subscriber growth to a massive, capital-intensive pivot into orbital artificial intelligence (AI) infrastructure.

Because this is a preliminary prospectus — the regulatory filing companies submit before going public — the final share price and size of the public float, which is the number of shares available to buy, are still blank. Investors will need to monitor subsequent announcements closely, as these missing figures will ultimately dictate the exact share availability, SpaceX's stock price, and SpaceX's valuation at debut.

Prospective buyers should keep a close eye on the upcoming timeline as the company gears up for its historic market launch. The official executive roadshow is expected to begin June 4, which will lead directly to the final initial public offering (IPO) pricing on June 11. Trading is expected to officially commence the very next day, with the highly anticipated public listing on June 12.

Below, The Motley Fool breaks down what investors need to know ahead of the SpaceX IPO.

Key Points

- SpaceX S-1 reveals a $4.9 billion loss in 2025, driven by heavy AI and Starship investments.

- Elon Musk, who serves as CEO, CTO, and chairman of SpaceX, retains 85.1% voting power post-IPO, ensuring control over company decisions.

- Starlink, SpaceX's profitable segment, shows slowing growth with revenue per user decreasing.

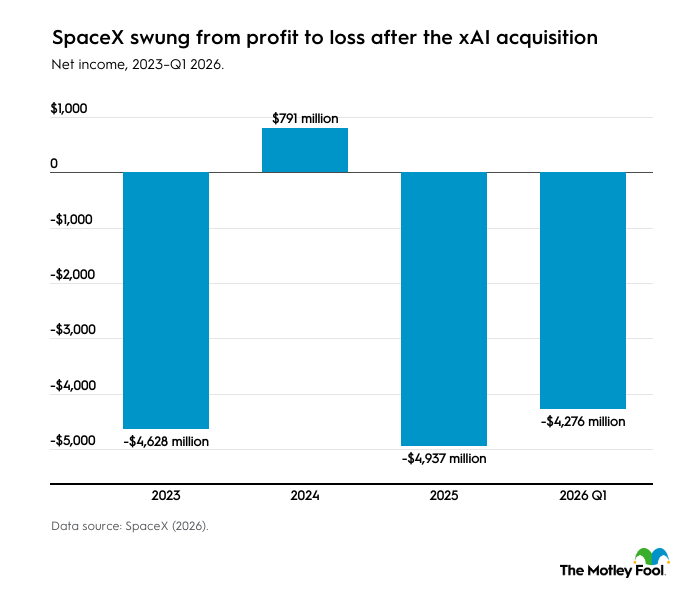

SpaceX was not profitable in 2025, and the S-1 explains why

While SpaceX posted a net income of $791 million in 2024, its new S-1 filing reveals a pivot to a $4.9 billion net loss in 2025 due to aggressive investment in the business.

The loss does not mean the underlying business is faltering. The company's space and connectivity segments demonstrated their financial muscle, generating $6.6 billion in non-GAAP (generally accepted accounting principles) adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $6.8 billion in operating cash flow over the same period.

Instead, the net loss stems directly from a $6.4 billion operating loss in its newly integrated AI segment and $3 billion in capital expenditures dedicated to developing the company's massive Starship rocket, totaling $20.7 billion.

To cushion this intensive spending, SpaceX also holds 18,712 Bitcoin, purchased at a cost basis of $661 million, which had a fair value of $1.637 billion as of Dec. 31, 2025.

These metrics show that while the launch and satellite operations are engines of real cash, overall short-term profitability is being absorbed by the double-edged sword of scaling xAI and accelerating Starship simultaneously.

Elon Musk controls 85% of the votes required to remove him as CEO and chairman

The SpaceX filing continues a trend in tech IPOs toward founders taking steps to retain control.

Post-offering, CEO Musk will retain 85.1% of the combined voting power preoffering, including 93.6% of the class B shares, which will elect 51% of the board as a separate class. Because of this structure, any attempt to remove Musk as CEO or chairman requires the approval of a majority of class B shares, effectively giving him absolute unilateral control over leadership.

To raise future capital without diluting this tightly held power dynamic, SpaceX has also authorized the issuance of 10 billion nonvoting class C shares.

It should also be noted that legal recourse for outside investors is severely limited. All shareholder disputes are funneled into mandatory ICC arbitration, stripping shareholders of their rights to class actions or jury trials.

This framework means public shareholders receive pure economic exposure to SpaceX's growth but no meaningful governance rights. This extreme voting concentration, zero-vote share structure, and restrictive legal environment underscore a vital reality for potential buyers: You aren't just investing in a company, you are explicitly buying into Musk himself.

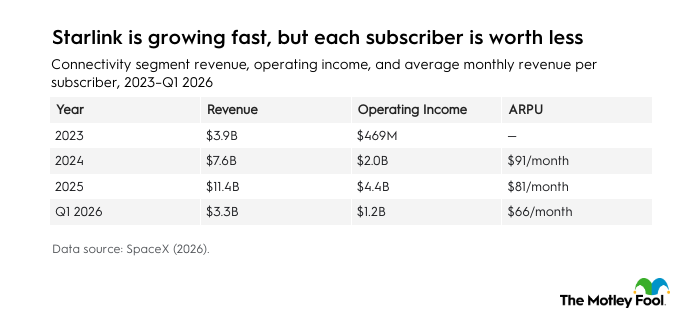

Starlink is the only profitable segment of SpaceX, but growth is slowing

SpaceX’s S-1 reveals that Starlink is its only profitable segment, generating $11.4 billion in revenue in 2025, even though its annual revenue growth slowed to 49.8% from 96.4% in 2024.

Despite this deceleration, the division boasts exceptionally robust margins, recording GAAP operating income of $4.4 billion, a 39% GAAP operating margin, and a 63% non-GAAP segment-adjusted EBITDA margin. To feed this massive deployment, SpaceX utilized 122 of its 165 total Falcon launches in 2025 for internal Starlink missions, successfully propelling total subscribers to 10.3 million as of March 31, 2026 — a 105% year-over-year increase.

However, this rapid global expansion has diluted pricing power, causing average revenue per user (ARPU) to plunge from $91 a month in 2024 to $81 in 2025, and down to $66 in the first quarter of 2026. So while Starlink is highly profitable with strong margins, its average revenue per subscriber has fallen 27% in just over a year.

This trend is critical for potential shareholders to track, as Starlink's cash generation is funding both the company's intensive Starship development and its massive AI investment cycle.

The big question for the market is whether this declining ARPU will soon stabilize, and if the segment can continue expanding at a pace that will satisfy public investors.

Anthropic is paying SpaceX $1.25B a month

Investors found out earlier this year about a deal between SpaceX and Anthropic. The S-1 provided the details, most notably the $1.25 billion monthly compute fee Anthropic will pay through May 2029.

The SpaceX AI segment generated $3.2 billion in revenue in 2025, and Grok reached 117 million monthly active users (MAUs) as of March 31, 2026.

SpaceX also has the option to acquire AI firm Cursor at an implied equity value of $60 billion.

The newly revealed Anthropic contract confirms there is genuine, large-scale commercial demand for SpaceX’s AI compute infrastructure rather than just internal workloads.

This deal serves as the strongest evidence that SpaceX's heavy tech infrastructure commands true market value, forcing prospective investors to decide whether the AI segment's steep losses represent a lucrative multi-year investment or an ongoing financial drain.

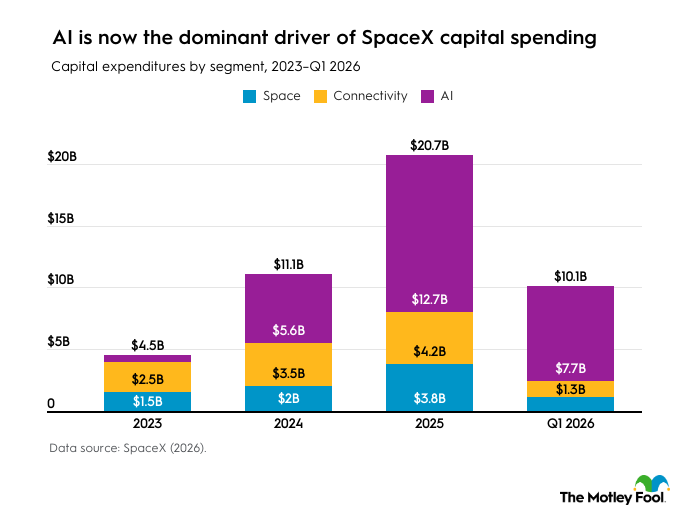

The AI bet is enormous, and years from profitable

SpaceX aggressively expanded its technological footprint in 2025, investing roughly $19 billion in AI as overall spending continued to accelerate.

In total, the company reported a 2025 operating loss of $6.4 billion from AI, with $12.7 billion in AI capital expenditures (capex) and $5.1 billion in AI research and development. Additionally, the company recorded $9.1 billion in "other financings," representing AI infrastructure assets categorized as failed sale-leaseback transactions.

This momentum carried over heavily into Q1 2026, when AI capex reached $7.7 billion. That number surpassed the company's full-year 2023 capex of $4.4 billion.

SpaceX's space and connectivity businesses are both EBITDA-positive. Investors hope the AI segment can follow a similar path, but on a capital base roughly 10 times larger.

SpaceX carries $29B in debt

As of March 31, 2026, SpaceX's total debt stands at $29.1 billion, including a $20 billion bridge loan established in March 2026 to retire xAI's legacy debt.

In the "Use of Proceeds" section of the S-1, SpaceX is focused on growth, noting investments in AI compute infrastructure, launch infrastructure, and satellite constellations. However, a separate liquidity disclosure reveals a stricter reality, disclosing that the $20 billion bridge loan must be repaid within six months of receiving IPO proceeds.

This means that a highly meaningful portion of what investors are funding through the IPO is actually a massive debt refinancing rather than new operating investments.

Further complicating the long-term capital outlook is a separate deal with EchoStar to acquire its wireless spectrum assets, set to close in November 2027. That deal includes the issuance of 261.8 million new Class A shares at $42.40 per share, plus up to $8.5 billion in cash.

As a result of these heavy financial commitments and restrictive debt covenants, no dividends are planned for the foreseeable future.

SpaceX dominates space launches, but it’s betting the future on Starship

SpaceX commanded more than 80% of the global mass to orbit in 2025, continuing an aggressive trajectory in which total payload mass surged from 1,210 metric tons in 2023 to 1,699 metric tons in 2024 and to 2,213 metric tons in 2025.

This scaling is underpinned by extreme efficiency, with Falcon Heavy reducing launch costs to low Earth orbit to just $1,400/kg — a 92% drop from NASA’s historical average of $18,500/kg.

Flight-proven boosters handled 157 of 165 launches in 2025, including a single booster reused 34 times.

While this unmatched launch dominance provides the structural foundation for both Starlink’s economics and the company's orbital AI ambitions, future growth hinges entirely on Starship, which received $3 billion in 2025 R&D and is targeting its first commercial payload delivery in the second half of 2026.

This timeline carries intense pressure because Starship has not yet successfully delivered a commercial payload to orbit.

The success of Starship could determine the success of the space business. The prospectus flags any potential Starship delay as the single most consequential risk to SpaceX's growth strategy.

How should investors think about the SpaceX IPO?

The prospectus confirms that SpaceX's core launch and satellite operations are robust, cash-generative engines, with the company commanding more than 80% of global mass to orbit in 2025 and Starlink generating $11.4 billion in connectivity revenue. But the steep 2025 net loss of $4.9 billion also shows the impact of growing investments into Starship R&D and a rapidly scaling AI infrastructure segment.

On governance and leverage, the filing discloses an incredibly restrictive structure in which Musk controls 85.1% of the voting power, leaving public shareholders with economic exposure but no meaningful corporate governance rights. Furthermore, SpaceX carries $29.1 billion in total debt, including a critical $20 billion bridge loan used to retire xAI's legacy debt that must be repaid within six months of closing the IPO. While the final company valuation and exact equity dilution remain unanswered until pricing, it is clear that a meaningful portion of investor funds will immediately go toward debt refinancing rather than fueling fresh operational expansion.

Ultimately, the prospectus frames SpaceX as a high-stakes combination of an unparalleled aerospace growth story and an early-stage, capital-intensive AI titan. The opportunity lies in the company successfully replicating its space profitability model across an AI infrastructure segment built on a capital base roughly 10 times larger. The challenge, like the challenge of reusable rockets and moon colonies, is formidable. But the opportunity is massive if SpaceX can execute from here.

FAQ

What does SpaceX's IPO prospectus say about its finances?

SpaceX’s prospectus revealed a highly complex financial picture. The document shows that while its core aerospace operations generate significant cash, the company has transformed into a massive, capital-intensive bet on artificial intelligence infrastructure.

Is SpaceX profitable?

SpaceX is not currently profitable, but it has been profitable in the past. The company posted a net loss of $4.9 billion last year, down from a net income of $791 million in 2024.

What is Elon Musk's stake in SpaceX after the IPO?

Musk will control 85.1% of SpaceX's voting power after the IPO, including ownership of 93.6% of a special B-class of shares.

This story was produced by The Motley Fool and reviewed and distributed by Stacker.