What is probate, and how does it work?

When a loved one passes away, their finances, property and personal belongings don’t automatically transfer to family members. A formal, court-managed process called probate handles this transfer.

Probate can feel unfamiliar and overwhelming, especially during an already emotional time as you grieve. The good news is that understanding the basics goes a long way toward easing that uncertainty.

Here is Inheritance Funding’s in-depth guide to the probate process so you know what to expect at every stage.

What Is Probate?

Probate is the formal court process for distributing a person’s assets after they pass away. Think of it as the official “closing out” of someone’s financial life. The court steps in to make sure that any outstanding debts and bills are paid and that whatever remains is distributed to the rightful heirs.

This process happens through the probate court, which is a specific type of court that handles matters related to estates, wills and the transfer of property after death. Every state has its own version of this court, and the rules can vary depending on where the deceased person lived.

The probate process is detailed and time-consuming because it helps the court confirm that the person’s wishes, as stated in their will, are carried out honestly. It also ensures that everyone who is owed money is paid before assets are distributed to heirs.

Why Is Probate Necessary?

The probate process exists to protect everyone involved, including the heirs, creditors and the wishes of the person who passed away. It provides structure and accountability during a time that can otherwise feel chaotic.

Without a formal system in place, there would be no way to verify whether a will is real, no organized method for paying off debts and no official record of who received what.

Some protections that probate provides include:

- It confirms the will is real: The court reviews the will to confirm it is authentic and represents the deceased person’s final wishes. This process may involve witness statements confirming the person was fully sane and sober when they signed it.

- It puts the executor in charge: The person named in the will to manage the estate, known as an executor, must be formally recognized by the court. The official recognition gives them the legal power to act on behalf of the estate, like accessing bank accounts or selling property.

- It protects creditors: Probate creates a formal window of time for anyone who is owed money by the deceased to come forward and file a claim. This process makes sure that debts, medical bills and other financial obligations are addressed before assets are handed out.

- It settles disagreements: If loved ones disagree about the will or how assets should be distributed, the probate court provides a setting where those disagreements can be heard and settled.

- It creates a clear record of ownership: For assets like real estate, probate documents an official record that the property has been transferred from the deceased to the new owner. This transparent chain of ownership is vital for future sales or refinancing.

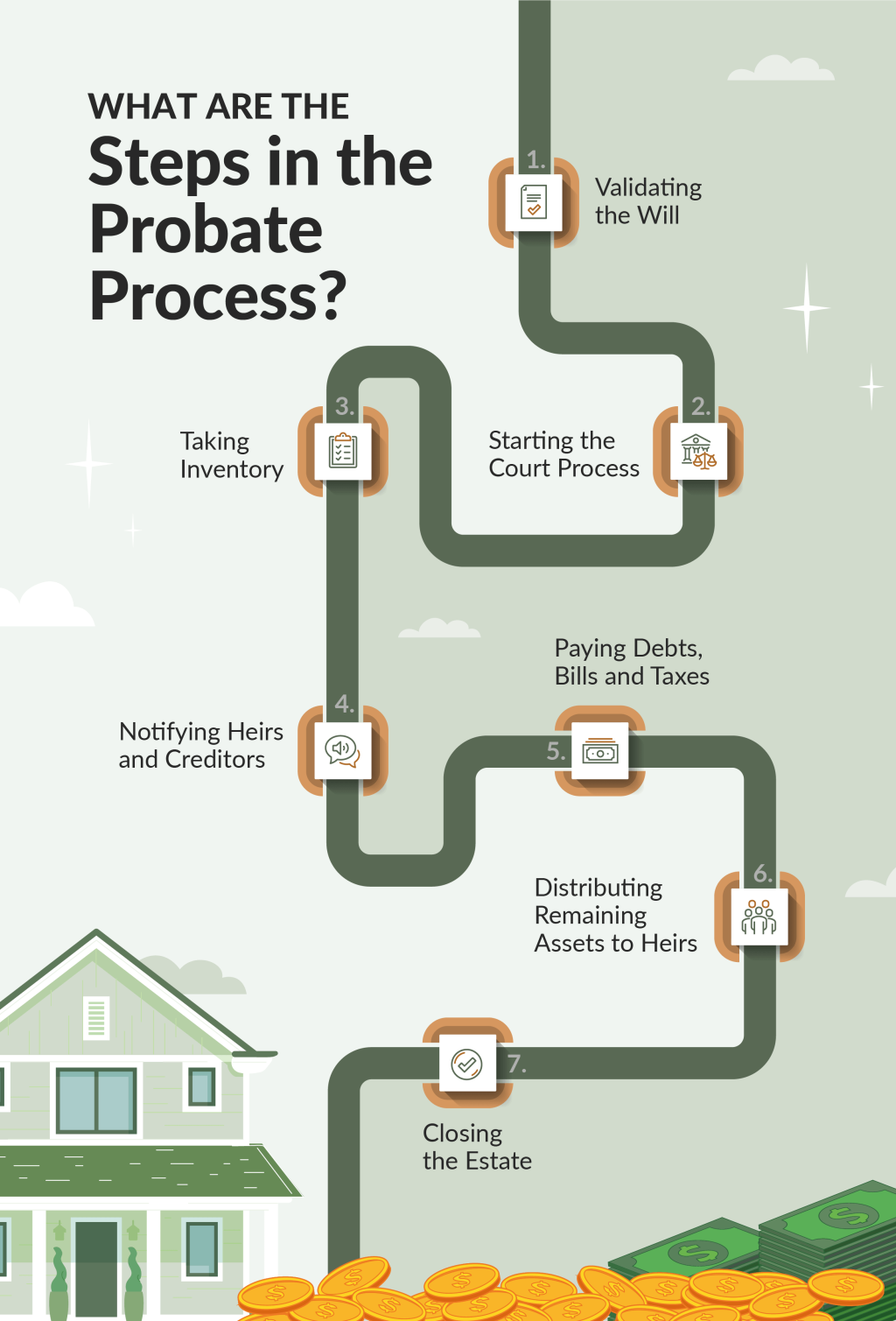

What Are the Steps in the Probate Process?

The probate process follows a standard sequence. While the exact timeline and requirements vary from state to state, the overall structure is consistent across the country.

1. Validating the Will

The first thing the court does is prove that the will is legally valid. This validation process is actually where the word “probate” comes from. The court reviews the document to make sure it was signed properly and that the person who wrote it was of sound mind — sane, sober and not on any medication that would compromise their decision-making capabilities.

In some cases, witnesses who were present at the signing may need to provide testimony. If the court decides the will is legitimate, the process moves forward. If there is no will or it is found invalid, the court follows state law to figure out who gets what.

2. Starting the Court Process

The person named as executor in the will files a petition with the probate court, along with the original will and a certified copy of the death certificate. The court then schedules a hearing. If satisfied with the paperwork, the court officially appoints the executor.

This appointment gives the executor the legal power to manage all aspects of the estate, including accessing financial accounts and communicating with creditors. In many states, the court also issues official documents called Letters Testamentary (or Letters of Administration if there is no will), which serve as proof of the executor’s authority.

If you’re the executor, the work has just begun. If you’re not the executor, you can relax and wait for the process to end. But it’s still worth knowing the rest of the stages your loved one’s estate must go through while in probate before you can receive your inheritance.

3. Taking Inventory

Once appointed, the executor’s next job is to find and document everything the deceased owned, including bank accounts, real estate, vehicles and anything else of value. The court requires this full inventory before anything can be distributed.

This step can take a while, especially if your loved one had scattered or incomplete records. The executor may need to do the following for a complete inventory:

- Contact banks.

- Review tax records.

- Search through personal files.

- Track down assets that were not well-documented.

- Hire professional appraisers to value items like real estate or artwork.

4. Notifying Heirs and Creditors

The executor is required to formally notify all potential heirs and known creditors that the estate is in probate. In most states, this also involves publishing a notice in a local newspaper.

This public notice gives anyone who might have a financial claim against the estate a set window of time to come forward. This period is often several months, depending on state law.

The notification process also makes sure that no heir is accidentally left out. Even family members who are not mentioned in the will must be notified, since they may have the right to challenge the will or claim a share of the estate under state law.

5. Paying Debts, Bills and Taxes

Before any assets go to heirs, the executor must use estate money to pay all legitimate debts, including outstanding bills, medical expenses, credit card balances and any taxes owed.

The executor must also file a final income tax return for the deceased and, if needed, an estate tax return. All debts and taxes must be settled before anything can be distributed to heirs. If a creditor disputes a claim or the estate challenges a debt, this step can take extra time to sort out.

6. Distributing Remaining Assets to Heirs

Once all debts, bills and taxes are paid, the executor asks the court for permission to distribute the remaining assets to heirs. The court reviews the request and, if everything is in order, approves it.

The executor then distributes assets according to the instructions in the will. The process might involve transferring a property title, writing checks or handing over personal belongings. If there is no will, state law determines who gets what.

7. Closing the Estate

The final step is the official closing. The executor provides a full accounting to the court that shows every dollar, covering income, expenses, debts paid and assets distributed.

Some courts may require a final hearing. Certain states require a closing document from the IRS to confirm that all tax matters have been taken care of. Once the court approves this final report, the executor is officially done with their duties and the estate is closed.

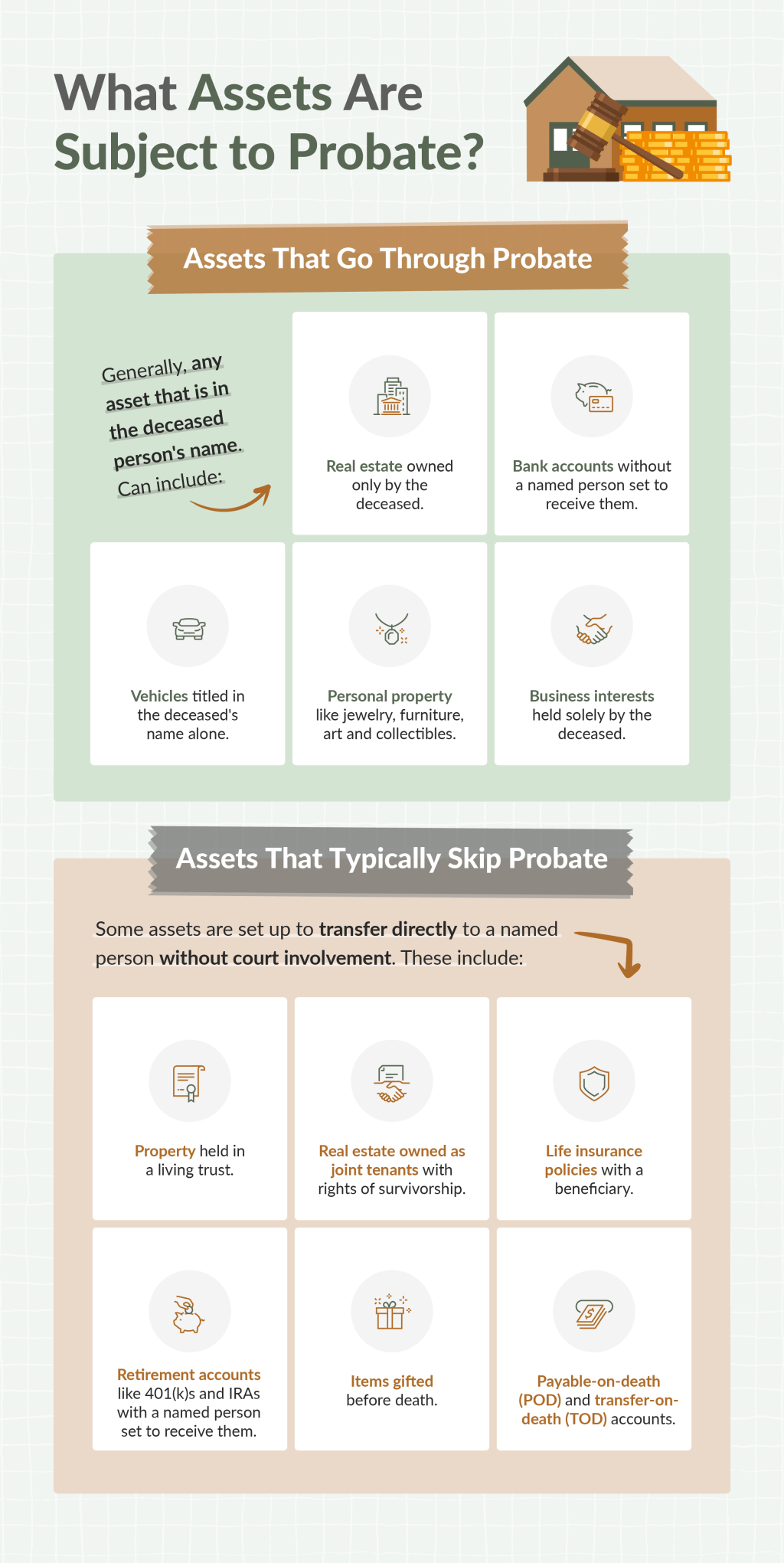

What Assets Are Subject to Probate?

Not everything a person owns goes through probate. The court process applies only to certain types of assets, and understanding the difference can save heirs a lot of confusion.

Assets That Go Through Probate

Generally, any asset that is in the deceased person’s name alone will need to go through probate. These assets include:

- Real estate owned only by the deceased.

- Bank accounts without a named person set to receive them.

- Vehicles titled in the deceased’s name alone.

- Personal property like jewelry, furniture, art and collectibles.

- Business interests held solely by the deceased.

Assets That Typically Skip Probate

Some assets are set up to transfer directly to a named person without court involvement. These include:

- Property held in a living trust.

- Real estate owned as joint tenants with rights of survivorship.

- Life insurance policies with a beneficiary.

- Retirement accounts like 401(k)s and IRAs with a named person set to receive them.

- Items gifted before death.

- Payable-on-death (POD) and transfer-on-death (TOD) accounts.

These assets skip probate because they already have a built-in way to tell banks, insurance companies and financial institutions exactly who should get the money. No court order is needed. This is why some family members or friends may receive certain assets quickly, while others must wait for the court to finish its work.

How Much Does Probate Cost?

Probate is not free, but the executor doesn’t pay for the costs out of pocket. Depending on the situation, probate costs generally fall between 3% and 7% of the estate’s total value, though the exact amount depends on the state, the assets involved and whether there are any complications. All probate expenses are paid from the estate’s money, meaning they reduce the total amount that will eventually go to heirs.

Here are the common probate costs you can expect:

- Court filing fees: Every probate case begins with a filing at the courthouse, which comes at a fee. Filing fees vary by state.

- Executor or administrator fees: The person managing the estate is entitled to be paid for their work. In many states, this payment is set by law as a percentage of the estate’s value.

- Attorney fees: Most executors hire a probate attorney to help them through the process. Attorneys may charge by the hour, a flat fee or a percentage of the estate’s value, depending on the state and how complex the case is.

- Appraisal and valuation fees: Certain assets, like real estate, antiques or business interests, may need a professional to determine what they are worth.

- Accountant fees: If the estate’s finances are complex, an accountant may be needed to prepare tax returns and manage financial records.

- Surety bond costs: Some courts require the executor to get a surety bond, which is basically an insurance policy that protects the estate if something goes wrong. The fee is usually a small percentage of the estate’s value.

- Taxes: The probate itself does not create new taxes. However, the estate is responsible for paying any final income taxes owed by the deceased and any estate taxes due.

Probate costs can go up significantly if someone contests the will or challenges how it is being handled.

How Long Does the Probate Process Take?

The average probate timeline is six to nine months, but more complex cases can take years. Several things can cause probate delays, pushing the timeline further, including:

1. The Complexity of the Assets

If the estate includes a business, rental properties, investments in multiple states or unusual personal property that is hard to value, the executor will need more time to get it sorted out.

2. Disagreements Among Family Members

If heirs challenge the will or argue over how assets should be distributed, the court has to schedule hearings and review evidence before the process can move forward. Even disagreements over small items can create holdups if they require a judge’s involvement.

3. Selling of Property

If property, like a home, needs to be sold before its value can be distributed, it can slow things down. The executor will need to list the property, find a buyer, close the sale, handle any costs, plus taxes, and then distribute the money.

4. Creditor Claim Periods

After creditors are notified, most states require a waiting period, often four to six months, before the estate can move forward. The waiting period gives anyone who is owed money the chance to come forward.

Frequently Asked Questions

Here are answers to the most common questions about the probate process:

How Long Do I Have to File for Probate?

You should file for probate as soon as possible after a loved one passes away. Deadlines to file vary by state and sometimes by county, so check your local requirements early to avoid unnecessary delays.

Where Does Probate Happen?

In most cases, probate takes place in the county where the person resided at the time of their death. The one common exception is real estate, which may be handled by a court in the county where the property is located.

Does Probate Still Happen Without a Will?

If your loved one passes away without a will, probate still happens. In that situation, the court follows state law to determine how assets are distributed and appoints an administrator to manage the estate.

What Probate Means for You

Probate is the official court-managed process for settling an estate after someone passes away. It involves confirming the will, putting an executor in charge, paying off debts and taxes and distributing what remains to the rightful heirs. This process takes time because it is meant to be thorough, transparent and legally binding.

If you’re waiting for assets to be distributed, understanding how the probate process works can bring peace of mind during what is often a difficult and emotional time.

This story was produced by Inheritance Funding and reviewed and distributed by Stacker.