As the Great Wealth Transfer begins, most families remain unprepared

The largest intergenerational wealth transfer in history is here. According to the Federal Reserve, Americans born before 1965 hold more than $105 trillion, or 63%, of household wealth in the U.S. Over the next two decades, the Great Wealth Transfer will see most of that passed on to younger generations.

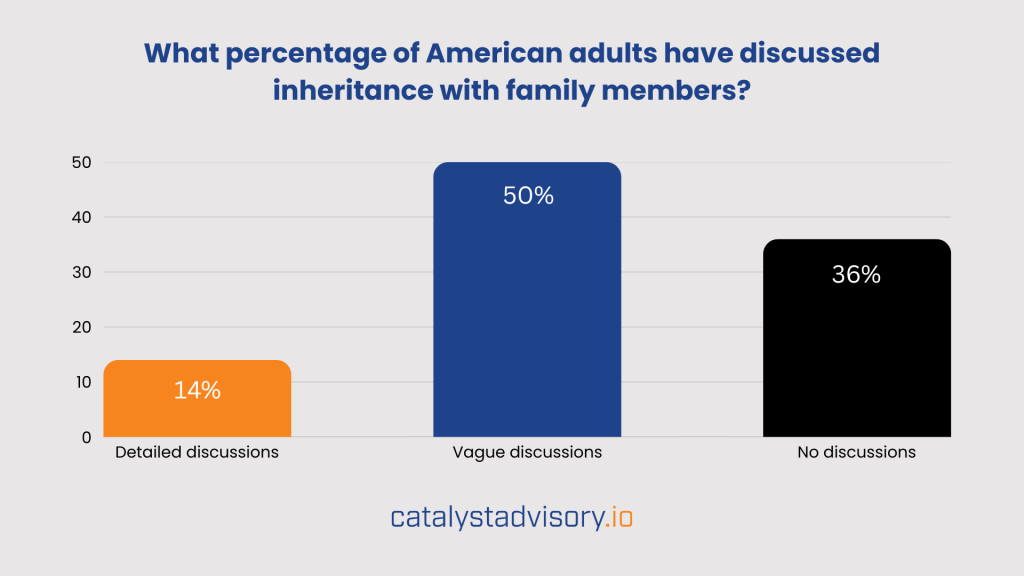

Yet, new research reveals that only 14% of American adults have had detailed conversations about inheritance with family members. One thousand U.S. adults were surveyed in November 2025 as part of the Family Wealth in America study conducted by Catalyst Advisory, a Pennsylvania-based wealth transfer advisory firm. The study found that half of Americans have discussed inheritance only in general terms, and more than a third (36%) have never discussed inheritance with family at all.

Despite the trillions of dollars set to change hands in the coming decades, most families simply haven't talked about inheritance in any meaningful way. Without proper communication and planning, families may experience damaged relationships, financial confusion, frustrating probate delays, unnecessary fees, and estate erosion from taxes that could have been avoided.

The Silence Problem

The stats are eye-opening. The Family Wealth in America survey revealed that 47% of American adults are uncomfortable or very uncomfortable talking openly about inheritance or finances with family members. And as a result, many simply avoid it altogether.

The lack of communication and planning isn’t limited to those who dread financial conversations. Even among those who claim they're comfortable discussing money with family, 26% have never actually done it.

Of course, inheritance topics have higher stakes for some families than others. But one of the most alarming details that came out of the study — nearly 1 in 4 adults (22%) who expect or think they may receive an inheritance have never discussed it. Far too many families are relying on assumptions and avoiding crucial conversations.

“By far the biggest issue is confusion,” says Clint Haynes, certified financial planner, founder and president of NextGen Wealth. “Where is everything located? What is going to whom? Why did you make these choices? The list can go on and on. That's why it's so important to have these conversations before anything happens, to ensure everyone is on the same page. While these conversations may not be the most enjoyable, particularly if the parents have made decisions the children may disagree with, they are essential.”

The Generational Divide

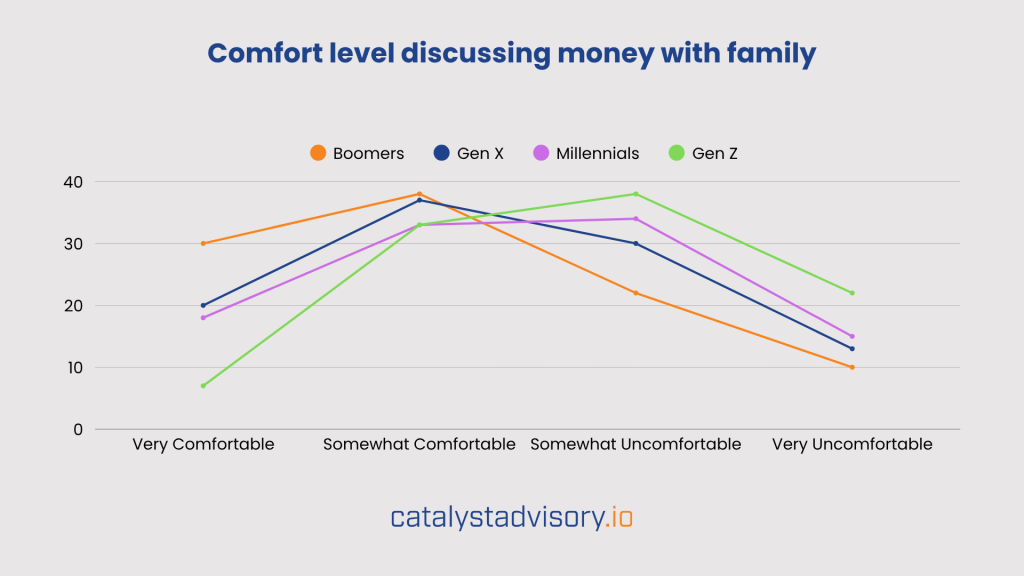

Some striking generational differences were also discovered. Those in Gen Z are more than twice as likely as Baby Boomers to be “very uncomfortable” discussing money with family (22% of Gen Zers, compared to 10% of Baby Boomers). Only 18% of Millennials (ages 28-43) and 7% of Gen Zers (18-27) are “very comfortable” discussing money with family.

Federal Reserve data shows that only 10.7% of U.S. household wealth currently belongs to those under 44 years old. These individuals and households will inherit significant assets over the next two decades; however, many in this group are especially uncomfortable with the discussion and planning needed.

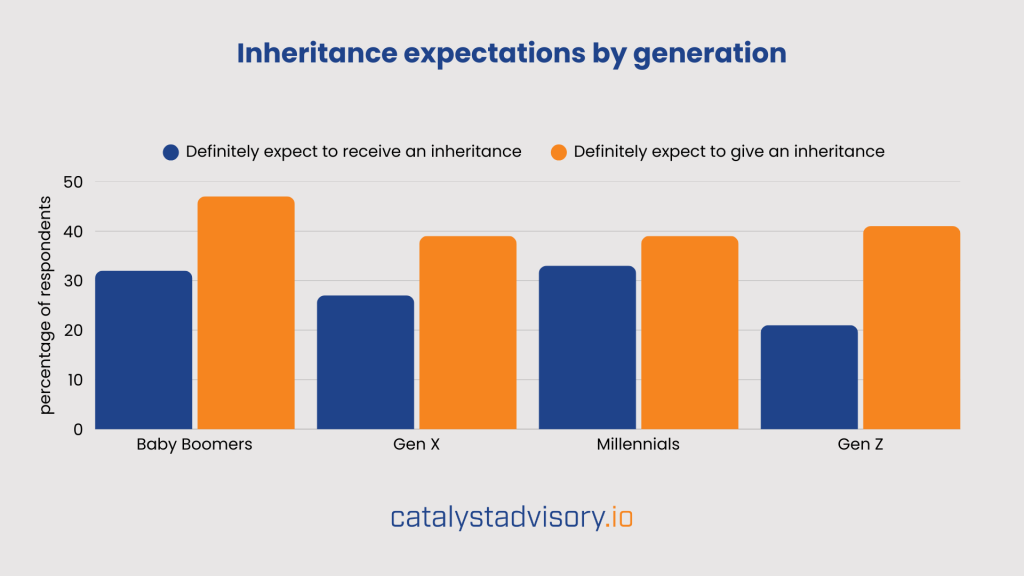

Interestingly, Gen Zers showed stronger expectations than any other generation for plans to leave something behind. Only 21% of Gen Z respondents expect to receive an inheritance, yet 41%, nearly double, expect to leave one. It’s obvious that younger Americans care about legacy; they’re just not very comfortable talking about it with loved ones yet.

The Gender Gap

The Family Wealth in America survey also uncovered a concerning difference between men and women. Most significantly, women are 43% more likely to be “very uncomfortable” talking openly about finances (16.7% of women, compared to 11.7% of men).

The survey also revealed slight differences in terms of expectations. Men are more likely than women to expect or think they may receive an inheritance (68% to 60%), and also more likely to definitely plan to leave an inheritance (45% to 36%).

The Desire for Legacy

The absence of inheritance conversations does not indicate a lack of concern about legacy. Survey participants were asked what they would do if they had wealth. Ninety-one percent said they would leave something behind, while only 9% would spend it all. And among those expecting to receive an inheritance, 93% also expect to leave something behind for future generations.

These numbers show that legacy does matter to most Americans. The issue is not that families don’t care. It’s that many struggle to talk about it. Money, inheritance, and mortality are uncomfortable subjects. However, when planning and communication are put off, families are more likely to experience confusion, tension, and preventable mistakes.

"I have seen many families torn apart when there was no plan, no decision maker, and no documentation providing direction,” says Evan Farr, certified elder law attorney with Farr Law Firm. “Siblings fight over money, who makes care decisions, and perceptions of unfair treatment by others. Relatives may even go to court to settle disputes regarding the loved one's estate and spend tens of thousands of dollars fighting each other rather than honoring the individual they care about."

Practical Steps to Begin Your Estate Planning

The need for financial conversations is clear. However, many people are overwhelmed and don’t know where to start or what’s involved. Attorney Michael J. Brooks emphasizes that estate planning doesn’t have to be complicated or intimidating. “In its most basic form,” he says, “it is simply about ensuring that a small set of essential decisions are made in advance, rather than left to the courts or to chance.”

What follows are the foundational elements families should understand as they begin the process.

Essential Documents Every Family Needs

The specific estate planning needs vary from one family to the next, depending on factors like the estate’s value, asset types, and family dynamics. But every family should have these basics:

- Will: Specifies how assets should be distributed after death

- Advance directive: Medical instructions for healthcare and end-of-life care preferences

- Durable power of attorney: Authority granted to a trusted individual to make financial and legal decisions in case of incapacitation

- Beneficiary designations: Names who will receive assets from retirement accounts, life insurance policies, and other financial accounts

Needs of More Complex Estates

A revocable living trust can be useful in certain situations, especially for avoiding probate delays, maintaining privacy, or ensuring smoother asset distribution. While not necessary for every household, trusts may be considered when assets are complex or in multiple states.

For families with significant wealth, business interests, or complex family structures, advanced planning may be needed.

Irrevocable trusts can address long-term planning goals, like tax efficiency, asset protection, and efficient wealth transfer. Unlike revocable trusts, these arrangements generally cannot be altered once established, so careful planning and professional guidance are essential.

When businesses are involved, families should also consider business succession planning. This ensures continuity, protects employees, and prevents disputes among heirs.

How to Start the Conversation

The need for communication and planning is clear. However, discomfort isn’t the only reason many families don’t discuss money and inheritance. Simply knowing where or how to start the conversation is another challenge.

- Start with context: Frame the conversation around planning for the future or recent life events, rather than jumping straight into specifics.

- Lead with curiosity: Ask open-ended questions that invite dialogue.

- Focus on preparation, not distribution: Early discussions should be about clarity and readiness, not deciding who gets what.

- Treat it as ongoing: Position the conversation as a first step, not a one-time discussion.

“Put yourself in your future self's shoes and recognize how grateful you will feel once you have a process/plan in place,” says Haynes. “While it may feel overwhelming at first, it will only get worse the longer you wait, and it can lead to much worse outcomes when it's too late after something has happened. Like anything that may be overwhelming, it's simply one step at a time.”

These specific questions can help direct the conversation in a practical and constructive way.

- What are your wishes if you become seriously ill or incapacitated?

- Where are important documents and account information located?

- Who would you trust to make financial or medical decisions on your behalf if needed?

- What values do you want to pass along with assets?

- Are there specific items with sentimental value that matter to you?

- Have you talked about what family members should and shouldn’t expect?

- Have you updated your beneficiaries recently?

Most Americans care deeply about legacy and want to leave something behind, yet far fewer feel comfortable talking about inheritance or taking the necessary steps. The findings suggest that silence, not indifference, is the primary obstacle.

The path forward starts with conversation, clarity, and a willingness to address uncomfortable topics before they become urgent. Those who take the time to talk and plan earlier are better positioned to reduce confusion and avoid preventable mistakes.

Methodology for the Family Wealth in America Survey

In November 2025, Catalyst Advisory surveyed 1,000 American adults (aged 18 and over) via Prolific.com. Respondents answered a series of questions about their feelings on inheritance and comfort level discussing money with family. All data is based on self-reported responses from survey participants.

This story was produced by Catalyst Advisory and reviewed and distributed by Stacker.