HELOC vs. home equity investment

Whether you’re funding renovations, consolidating debt, or planning for the future, the equity you have in your home can be a powerful financial tool. But what’s the best option for actually leveraging that equity?

Traditional options, such as home equity lines of credit (HELOCs), offer flexibility but come with variable interest rates and monthly payments. Newer tools like home equity investments (HEIs) provide cash upfront with no monthly obligations, trading a share of future home value instead.

HELOCs have remained a standard home equity tool, with data from the Federal Reserve Bank of New York’s Household Debt and Credit Report showing aggregate HELOC balances increasing by 20% from Q1 2021 to Q4 2024. But as borrowing costs remain high, with average HELOC rates at nearly 8% as of October 2025, understanding the differences between these two models has never been more crucial. This guide from Splitero breaks down how each option works and what sets them apart in today’s housing market.

Key Takeaways

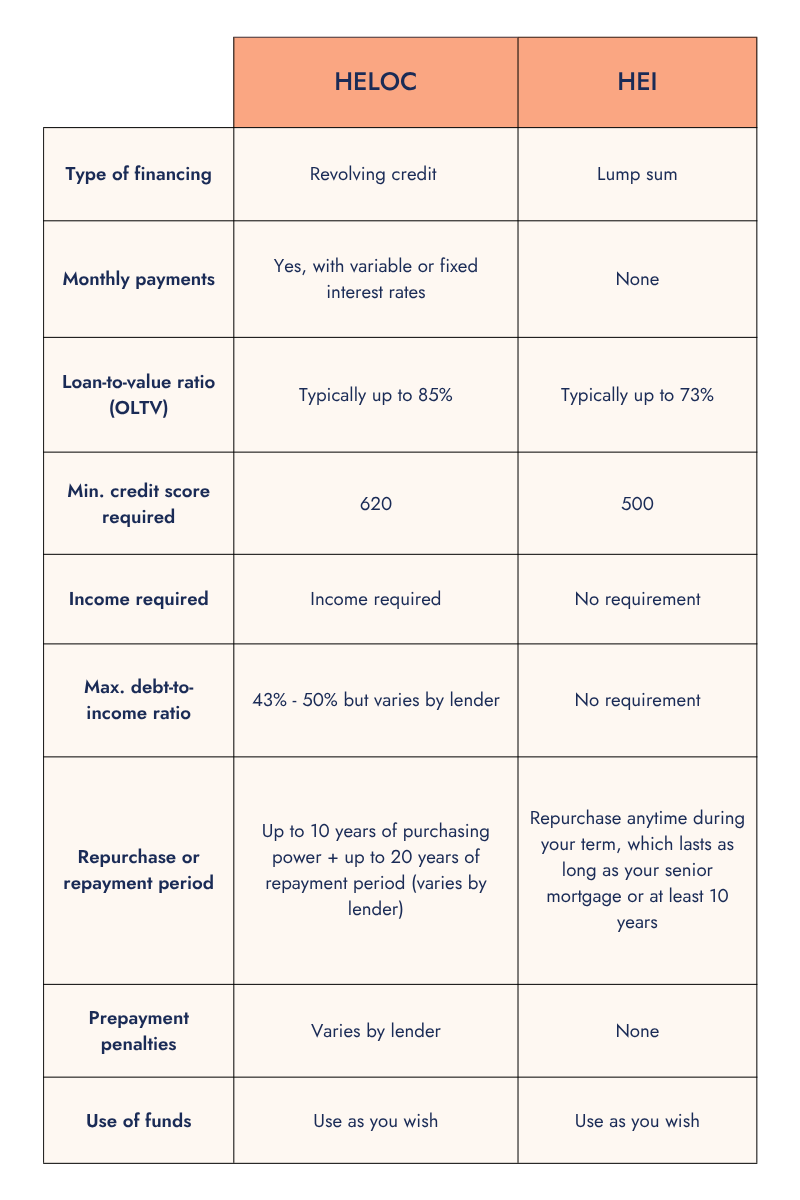

- A HELOC is a revolving line of credit that lets homeowners borrow against their equity, make withdrawals during a draw period, and repay with interest over time.

- A home equity investment (HEI) provides a lump-sum payment in exchange for a share of the home’s future value, with no monthly payments or interest.

- HELOCs function like credit lines, offering flexible access to funds and variable repayment terms, while HEIs operate as investments, repurchased later based on the home’s value.

- Both options use home equity as collateral but differ in cost structure, qualification requirements, and how repayment or repurchase is handled.

What is a HELOC, and how does it work?

A HELOC, or home equity line of credit, is a revolving line of credit that allows you to borrow against the equity in your home. With a HELOC, you can access funds up to a pre-determined credit limit and use them as you see fit. The credit limit is based on the amount of available equity you have in your home. You only pay interest on the amount you borrow, and you can use the funds for any purpose.

Additionally, HELOCs are characterized by a few key aspects.

- Interest rate: A HELOC typically has a variable interest rate, meaning your monthly payments may fluctuate with the market.

- Draw period: During this stage, you’re able to make purchases using your line of credit and repay as needed. The draw period usually lasts up to 10 years.

- Repayment period: The initial draw period is followed by a repayment period during which you can no longer use your credit line for purchases. During the repayment period, you pay back any remaining balance on the principal and any outstanding interest.

Pros

- Use and reuse your funds: During the draw period, you can use your available credit, repay it, and use it again.

- Only pay what you borrow: A line of credit allows you to withdraw only what you need. This means that you only pay interest on what you actually borrow, not the total value of your credit line.

- Tax benefits: If you leverage your HELOC to fund home improvements, the interest you pay on the funds you use could be tax-deductible.

Cons

- Variable interest rates: HELOCs typically have variable interest rates. When rates are low, this could be beneficial. But when rates are high, it could end up costing you significantly.

- Credit and DTI limitations: The minimum credit score typically required to qualify for a HELOC is around 620, but many lenders may prefer a higher score. Additionally, the maximum debt-to-income ratio typically allowed is around 43% to 50%. Even if you meet basic credit score and DTI requirements for a HELOC, you may still end up with an unfavorable rate if you don’t have a pristine credit history.

- Income requirements: If you’re self-employed or retired, you may have trouble qualifying for a HELOC due to the income requirements lenders require.

What is an HEI?

A home equity investment, or HEI, allows you to access the equity you’ve built in your home as a lump-sum cash payment in exchange for a percentage of your home’s future value. As the home’s value changes over time, an investor also shares in that appreciation or depreciation.

The investment option, or “the option-purchase agreement,” you enter into usually lasts at least 10 years.

There are various ways to repurchase your investment, including a cash settlement or through the proceeds of a home sale. Regardless of the method you choose, there are no monthly payments, and you can exit the agreement at any time during the term.

Pros

- No monthly payments or APR: HEIs don’t require monthly payments and don’t accrue interest.

- Low qualification requirements: HEIs typically have a much lower minimum credit score requirement (500) and do not require income.

- Shared downside protection: If your home depreciates over the course of your investment term, the investor shares in that loss with you, as your repurchase amount is not a fixed dollar amount.

Cons

- Limited availability: HEIs are a relatively new financing option and aren’t yet available in every U.S. state.

- Limited refinancing flexibility: Some lenders may require you to settle your HEI before refinancing or taking out additional home loans.

- Repurchase cost varies with home value: Your repurchase amount is impacted by your home’s future value. If your home appreciates rapidly over the course of your investment term, the final repurchase amount may come as a surprise. Not all HEI companies are alike, and their capped percentages may differ.

What’s the difference between a HELOC and an HEI?

HELOCs and HEIs differ in several key aspects, including financing structures, qualifications, and risk:

- Credit line vs. lump sum: A HELOC is a line of credit, so during the draw period, you can use it, pay it down, and use it again. An HEI, on the other hand, gives you a lump sum payment of your equity without any monthly or incremental payments.

- Monthly payments: HELOCs enter a repayment schedule once the repayment period begins, which typically involves monthly payments until both the principal and interest balances are paid down. Home equity investments do not require any monthly payments, and you can repurchase your agreement at any time during your term.

- Credit qualifications: HELOCs are credit lines, so they naturally have tighter credit score qualifications. Many HELOC lenders will require a credit score of at least 620, but you’ll get more favorable terms if your credit score is higher. On the other hand, HEIs are not a line of credit, so their credit score requirement is set lower, usually around 500.

- Income qualifications: HELOCs require you to have a verifiable income, whereas home equity investments do not typically have stringent income requirements, making them ideal for self-employed homeowners or retirees.

- Risk: With a home equity investment, the investor shares the risk of the home’s value decreasing, but also has the potential for a greater return if the home’s value increases. A HELOC is secured by the value of your home, and failure to make payments could result in foreclosure (you lose your home).

Comparison table: HELOC vs. HEI

HELOC vs. HEI: Which is best for you?

If you’re trying to decide between a HELOC versus an HEI, the best option will depend heavily on your specific financial situation. However, there are a few initial considerations that may help you begin narrowing down your options.

- Your credit score: If you have a great credit score, either option will benefit you. If you have a credit score below 620, you may have trouble qualifying for a HELOC. If you have a credit score below 680, you may have difficulty obtaining favorable rates.

- Your employment status: If you are retired, unemployed, or self-employed, an HEI may be easier for you to qualify for, as HELOCs typically have income requirements. If you are employed, then either option could be a good fit for you.

- Your financial goals: Do you plan to use your funds toward a large purchase, like a retirement fund or your child’s education? If so, a home equity investment may make more sense than a HELOC, as you can avoid monthly payments and interest accrual.

- Monthly payments: If you’re not comfortable taking on monthly payments, a home equity investment may be a better option for you. A HELOC will require monthly payments once the draw period ends, whereas an HEI does not require monthly payments.

- Fees and closing costs: Each option includes various fees and closing costs, including appraisal fees, origination fees, and title search fees. When considering each option, ensure you understand the upfront costs associated with each.

Considering these variables, here are a handful of circumstances in which one option may be better than the other:

Additionally, it's always important to weigh the risks and benefits of each option and consult a financial advisor or expert to help determine which is best for you.

Frequently Asked Questions

What is a home equity investment (HEI)?

A home equity investment, or HEI, allows you to access the equity you’ve built in your home as a lump-sum cash payment in exchange for a percentage of your home’s future value.

What is a home equity line of credit (HELOC)?

A HELOC, or home equity line of credit, is a revolving line of credit that allows you to borrow against the equity in your home.

What’s the difference between a HELOC and an HEI?

The key difference is financing structure: A HELOC is a revolving line of credit, while a home equity investment (HEI) is a lump sum of cash. Additionally, HELOCs require monthly payments once you enter the repayment period, whereas HEIs do not require any monthly payments.

This story was produced by Splitero and reviewed and distributed by Stacker.