Most Social Security recipients say 2.8% COLA isn’t enough

Starting in January 2026, the average monthly Social Security check for the U.S.’s 74.5 million Social Security recipients will be around $1,917, up 2.8% from 2025. That’s an increase of about $52 per month. But the majority of beneficiaries aren’t happy with that increase.

According to The Motley Fool’s annual Social Security Cost-of-Living Adjustment (COLA) Survey, 54% of Social Security recipients say the 2.8% cost-of-living adjustment isn’t enough and 68% say the adjustment will provide very little or no help in covering essential living expenses — crucial findings given how important Social Security is in retirement planning.

The Social Security COLA is determined by the rate of inflation — but most Americans receiving Social Security believe a much higher adjustment is necessary to keep up with rising costs. 31% of respondents say a COLA of 10% or more would be required for their Social Security benefits to stay on pace with the cost of living.

Key points

- 54% of Social Security beneficiaries say the 2026 2.8% Social Security COLA isn’t enough and won’t keep up with rising costs.

- More than half have either returned to work or are considering it because of low Social Security benefits.

- 31% believe a Social Security COLA adjustment of 10% is needed to keep up with inflation.

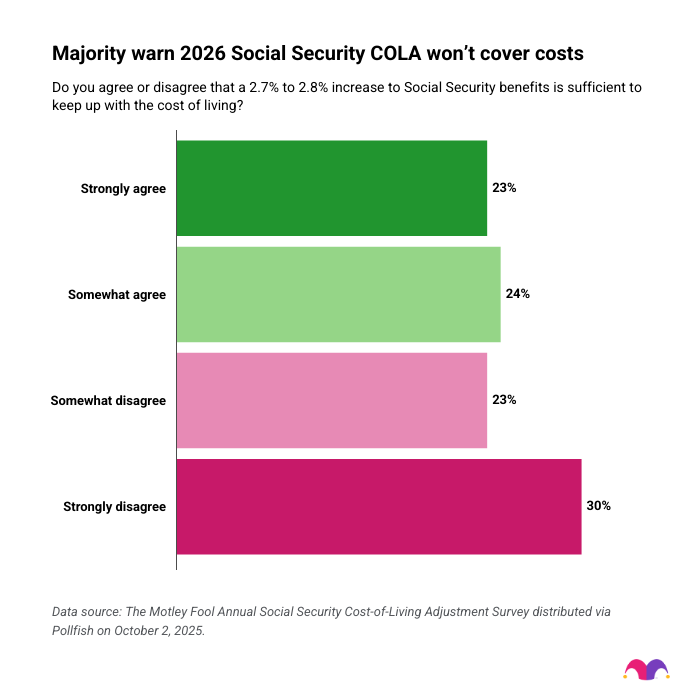

Majority warn 2026 Social Security COLA won’t cover costs

A majority of Social Security beneficiaries surveyed by The Motley Fool believe the 2026 Social Security COLA of 2.8% is insufficient. Overall, 23% of respondents disagreed somewhat that the COLA is sufficient to keep up with the cost of living and 30% strongly disagreed.

Just 23% of respondents strongly agreed that the COLA was enough and 24% somewhat agreed that it was sufficient.

Motley Fool Senior Retirement Advisor and Financial Planning Expert Robert Brokamp, CFP®, sees two factors that make it unlikely for retirees to see the 2.8% COLA as sufficient. “First, inflation has been ticking up recently,” he said, referencing recent inflation reports that have a 12-month increase in prices of over 2.8%.

The second factor has to do with the fact that Medicare premiums — which many retirees pay and are subtracted from Social Security benefits — are projected to increase at a higher rate than the COLA.

“Currently, premiums for Part B of Medicare are projected to go up more than 11% in 2026. So that will take out a bigger chunk of a beneficiary’s monthly check,” Brokamp said.

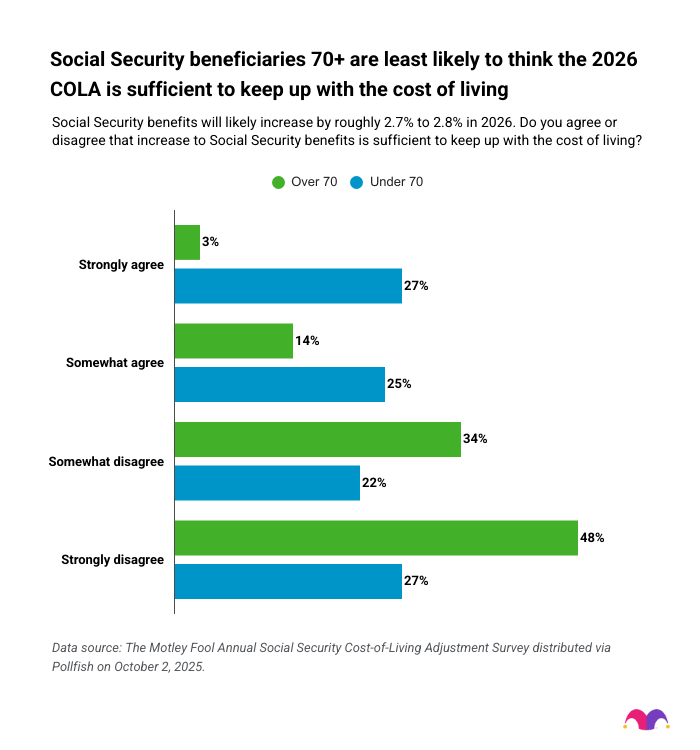

Older adults tend to rely more heavily on Social Security benefits, which may explain why 82% of respondents aged 70+ feel the 2.8% COLA is not enough compared to 49% of those under 70.

The more respondents rely on Social Security, the less likely they are to view the COLA as sufficient. 61% of those who exclusively or heavily rely on Social Security see the COLA as insufficient. Among respondents who rely on Social Security slightly or moderately, 42% see the COLA as not enough.

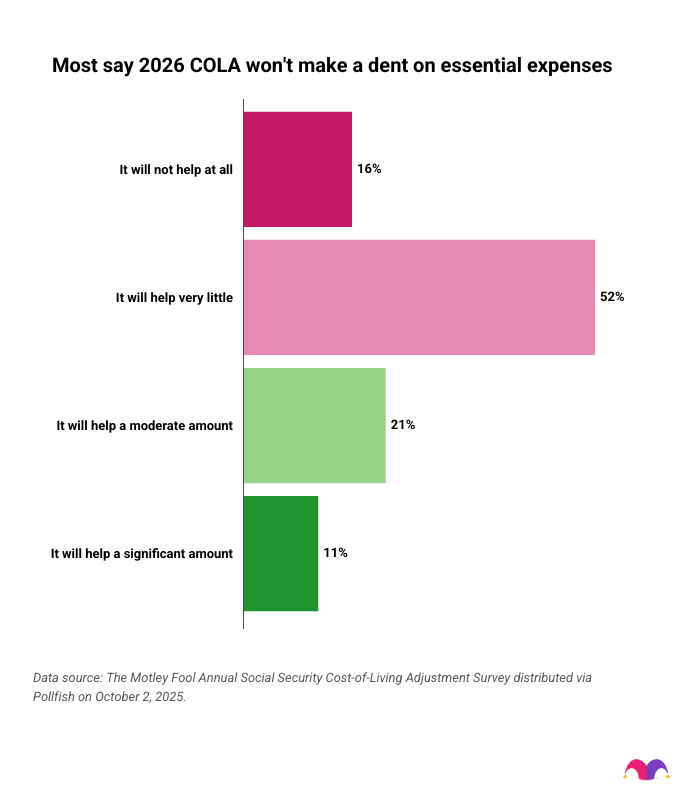

Most beneficiaries say the 2.8% increase won’t meaningfully cover essential expenses

The Social Security COLA is tied to the rate of inflation, but most respondents say it won’t meaningfully help their ability to pay for essential living expenses.

Sixty-eight percent of respondents say the COLA will offer little to no help —16% say it won’t help them at all and 52% say it will help very little. Just 11% say it will help significantly and the remaining 21% say the adjustment will help moderately.

This may be a reflection of inflation remaining elevated for multiple years in a row while retirement income and spending hasn’t kept pace. Americans aged 65 and older spent $5,007 per month, on average, in 2023, according to the Bureau of Labor Statistics Consumer Expenditure Survey, which is more than $3,000 more than the average Social Security check.

An additional factor is that the Consumer Price Index is based on a set of goods and services that may not reflect what retirees are spending their money on, Brokamp said.

“An individual’s experience of inflation will depend on that individual’s unique budget — which may be quite different from the items in the CPI,” Brokamp said. “For example, based on the August inflation report, the cost of food at home rose 2.7%, year over year, while the price of dining out increased 3.9%. So those who spend more time at restaurants may be more likely to feel that the Social Security COLA is not keeping up.”

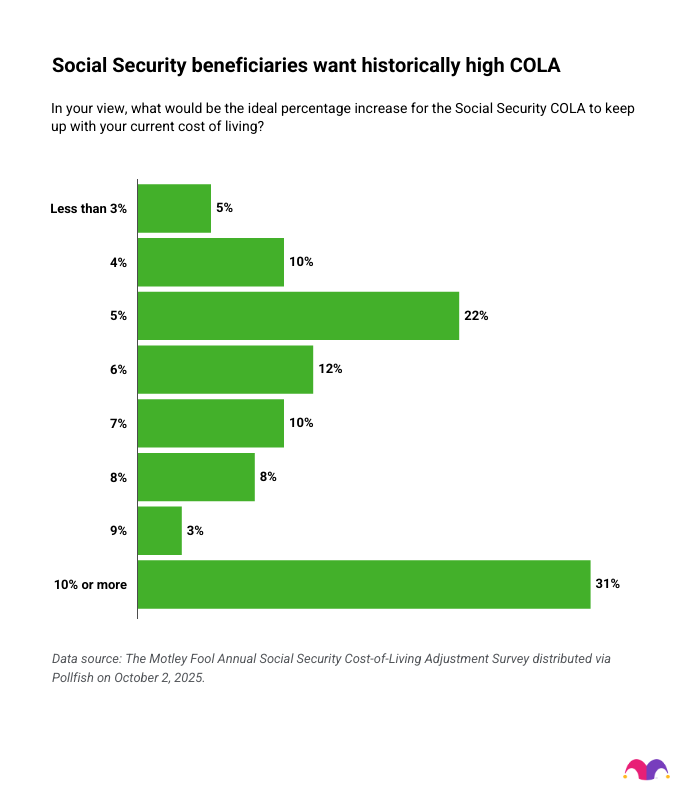

64% want COLA of 6% or more; 31% call for 10%+

Sixty-four percent of Social Security beneficiaries surveyed by The Motley Fool believe that in order to keep up with the cost of living, the Social Security COLA should be between 6% or more. 31% think the COLA should be 10% or more.

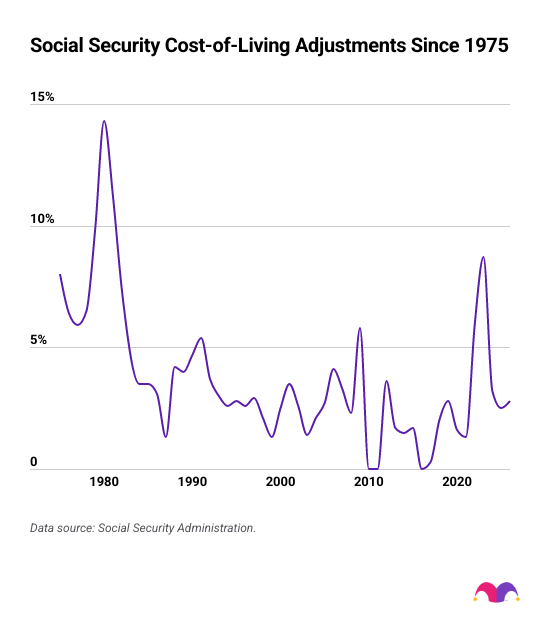

If beneficiaries' wishes were to come true, the COLA would be historically high. The Social Security COLA has only exceeded 6% once since 1984. That was in 2023, when beneficiaries received an 8.7% bump.

Historic Social Security Cost-of-Living Adjustments

The chart below shows the Social Security COLA since 1975.

Over half of beneficiaries may return to work due to low Social Security benefits

Fifty-four percent of Social Security beneficiaries surveyed by The Motley Fool have returned to work or are considering doing so because Social Security does not provide enough income to support their lifestyle.

The average monthly Social Security payment as of August 2025 is $1,864, according to the Social Security Administration. That does not cover even half of what Americans age 65 and older spent per month in 2023: $5,007, according to the Bureau of Labor Statistics. Considering only 54% of American households had a retirement account in 2022, according to the Federal Reserve, it’s not surprising that a significant percentage of retirees surveyed feel as though they need another source of income.

Social Security is only supposed to cover 40% of the average worker’s salary. In reality, however, retirees depend more heavily on Social Security than that.

Here’s how much respondents to The Motley Fool’s Annual Social Security Cost-of-Living Adjustment Survey rely on Social Security for their monthly retirement income:

- 29% rely exclusively on Social Security Benefits.

- 29% rely heavily on Social Security benefits.

- 24% rely moderately on Social Security benefits.

- 14% rely slightly on Social Security benefits.

- 5% don’t rely on Social Security benefits at all.

Retirees may want to return to work for a variety of reasons: for a sense of purpose, to provide daily structure, to support a charity or other cause, and more. But the survey results suggest that financial stability and maintaining their current lifestyle are driving factors for retirees thinking about finding a new job.

That said, there is a drawback for retirees going back to work prior to their full retirement age. Returning to work prior to full retirement age can result in some Social Security benefits being clawed back, Brokamp said.

“In 2025, seniors who wouldn't hit their full retirement age at any point during the year would begin losing $1 in benefits for each $2 in earnings above $23,400,” Brokamp said. “Those who are reaching FRA at some time during the year will be allowed to earn $62,160 per year in 2025 before losing $1 in Social Security income for every $3 extra they make.”

Inflation raises the need for strategic retirement planning

Retirees are feeling the bite of inflation. 54% of respondents to The Motley Fool’s Annual Social Security Cost-of-Living Adjustment Survey find the COLA insufficient, and 54% have gone back to work or are thinking about doing so.

Tracking spending and altering budgets to account for product-specific inflation are two strategies retirees can use to make their Social Security payments go further, Brokamp said. “Start by tracking your spending to find opportunities for cost-cutting that won’t significantly lower your day-to-day enjoyment of retirement,” he said.

“Also look for ways to replace items that have gone up in price with others that have seen less inflation. For example, the price of beef has gone up 16.6%, whereas seafood is up 6.7% and chicken 4.2%,” Brokamp said.

While retirees grapple with current conditions, younger Americans may be asking how much they need for retirement. That question gets to the heart of retirement planning. The data suggests that absent a plan, retirees may have to compromise on their lifestyle or return to work.

Methodology

The Motley Fool surveyed 2,000 Americans who receive Social Security benefits via Pollfish on October 2, 2025. Results were post-stratified to generate nationally representative data based on age and gender. Pollfish employs organic random device engagement sampling, a method that recruits respondents through a randomized invitation process across various digital platforms. This technique helps to minimize selection bias and ensure a diverse participant pool.

This story was produced by The Motley Fool and reviewed and distributed by Stacker.