Should I ditch my credit card for BNPL?

Buy now, pay later (BNPL) is popping up everywhere. An April 2025 LendingTree survey found that around half of Americans have used BNPL, and around 1 in 3 have used it more than once. Buyers aren’t just using it for essentials either, with a Billboard report finding that nearly 2 in 3 attendees at this year’s Coachella festival used BNPL to buy their tickets.

Credit cards, the grandfather of deferred payment solutions, have been around since the 1950s, and more than 4 in 5 US adults have one, according to the Federal Reserve.

Is it worth ditching high-interest plastic in favor of zero-interest cardless loans? Finder.com shares how BNPL and credit cards compare and when you might want to use one over the other.

Which is cheaper?

TLDR: BNPL can be cheaper for controlled spenders with a short-term repayment horizon, but it can be a dangerous financial trap for shopaholics who don’t have a financial plan.

BNPL is famously touted as a zero-interest alternative to other forms of debt financing like credit cards, which, for some people, can be a symbol of reckless spending. Here’s how the costs actually break down between popular BNPL plans and a typical credit card in the U.S. as of July 4, 2025:

Klarna

- Term: 6 weeks (4 payments, every 2 weeks)

- Rate: 0% (up to 35.99% APR for longer terms)

- Fees: none

- Penalties: late payment fee up to $7 (max 25% of purchase)

Afterpay

- Term: 6 weeks (4 payments, every 2 weeks)

- Rate: 0% (up to 35.99% APR for longer terms)

- Fees: none

- Penalties: late payment up to $8 (max 25% of purchase)

Affirm

- Term: 6 weeks (4 payments, every 2 weeks)

- Rate: 0% (up to 36% APR for longer terms)

- Fees: none

- Penalties: no late fee

Typical credit card

- Term: Open term

- Rate: 21.37%* (21-day interest-free grace period)

- Fees:

- Annual fee: $0 to hundreds of dollars

- Cash advance: 3%-5% (min $10)

- Foreign transaction: 1%-3%

- Balance transfer: 3%-5% (min $5)

- Penalties:

- Late payment: $32

- Over-the-limit: up to $35+

- Returned payment: $25-$40

*Average credit card interest rate as of February 2025 based on data from the Federal Reserve Bank of St. Louis.

So, is BNPL cheaper than a credit card? In the short run, yes.

Major BNPL companies like Klarna, Affirm and Afterpay will let you pay some of your purchase upfront and split the rest into three more payments with no interest or fees.

But there’s a catch. BNPL is attractive to carefree shoppers who don’t take repayments seriously and end up rolling over debt into longer-term BNPL loans with interest rates that can make credit cards look cheap.

Credit card interest rates are predictable, remaining fixed unless you miss payments and trigger the penalty rate. But there’s a host of other costs to consider with credit cards, such as annual fees—which reach hundreds of dollars for some premium cards—foreign transaction fees, over-the-limit fees and other charges that BNPL plans largely or entirely steer clear of.

If an unavoidable purchase arises, you don’t have enough savings and you’re confident you can pay off the bill in six weeks or less, BNPL could be worth considering.

But a credit card might be cheaper if you need more time to repay. That’s assuming you don’t carry a balance indefinitely, which would quickly wipe out the advantage of having a lower interest rate.

Which is safer?

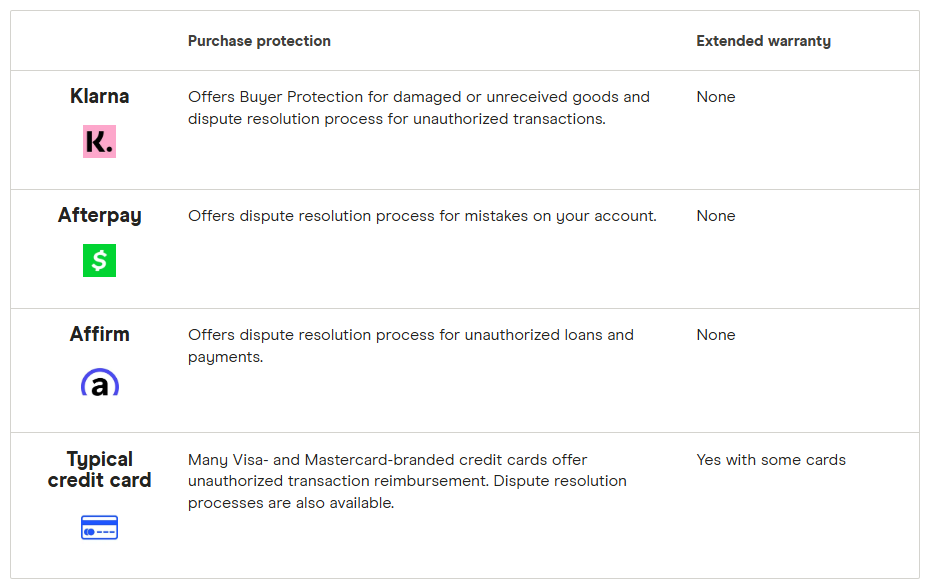

TLDR: Currently, credit cards come with greater consumer protections than BNPL loans.

Choosing BNPL over credit cards might lower the cost of borrowing in the short run, but credit cards win out when it comes to consumer protection—for now, at least. Not all credit cards offer the same features, but many come with consumer safeguards like purchase protection and extended warranty coverage.

This product information is accurate as of July 4, 2025.

Is BNPL regulated in the US?

Where U.S. regulation is concerned, BNPL currently operates in the Wild West. There’s very little regulation, although this is beginning to change.

New York recently enacted legislation requiring BNPL companies operating in the state to be licensed and follow rules regarding interest rate caps and fee limits. Others may follow the Empire State’s lead, filling in the gap left by the Consumer Financial Protection Bureau’s (CFPB) recent abandonment of efforts to bring BNPL under the regulatory framework of credit cards.

Back in May 2024, the CFPB ruled that buy now, pay later lenders are “card issuers” and should be subject to Regulation Z (also known as the Truth in Lending Act), which outlines rules that prohibit predatory lending among credit card issuers, installment loan providers and other lenders.

In light of President Donald Trump’s Executive Order 13891, aimed at deregulating and avoiding bureaucratic redundancy, the CFPB withdrew over 60 guidance materials in May 2025, reducing its powers of enforcement “to only those areas statutorily required.”

The BNPL loan ruling was among those axed, and its elimination has fueled the urgency to find a way to limit the risks of this fast-growing industry. It looks like state governments may be stepping up to the challenge.

Which comes with more perks?

TLDR: BNPL apps may offer some ways to save or earn rewards, but credit cards generally offer a greater range of complimentary benefits.

Cost and safety aside, which payment option offers more benefits and freebies? Backed by a much longer history of fine-tuning features to meet consumers’ needs and wants, credit cards come out ahead.

While some basic cards minimize perks to keep fees low, many others add on a slew of complimentary goodies to encourage card signups and spending. Welcome bonuses, travel insurance, car rental discounts, concierge services and special retail offers are just a few examples.

Many credit cards also let you earn rewards points, cashback or travel miles on your purchases. Accumulated bonuses can offset the cost of seasonal getaways or help you pay for everyday expenses—a top financial concern for many these days.

BNPL doesn’t offer as much by comparison.

- Klarna advertises up to 10% cash back at partner retailers when you make in-app purchases with the Klarna credit card.

- Afterpay has a loyalty program through which buyers can earn exclusive offers and access financing with no upfront payment required.

- Affirm has ventured even further into the money management sphere with the Affirm Card and Affirm Money Account for spending and saving. But there are few benefits aside from the ability to earn interest.

The gap between BNPL loans and credit cards may close over time as the buy now, pay later industry continues to evolve and offer more ways to make money and earn rewards.

On the other hand, BNPL lenders know their most profitable strength is remaining accessible to borrowers who have poor or no credit, so they might plan to intentionally fly below credit card programs and target subprime consumer spending.

Bottom line

So, which comes out on top: BNPL or credit cards? BNPL loans cost less if you pay off your purchase entirely within the zero-interest financing term (usually six weeks), and you don’t roll over your debt into long-term plans with high interest.

But the credit card industry is backed by greater consumer protections and has more to offer if you’re looking for ways to leverage your recurring or long-term spending to earn rewards.

It may not be worth ditching your credit card for BNPL loans right now—but that doesn’t mean “Pay in 4” lenders won’t start giving credit card companies a run for their money in the future.

This story was produced by Finder.com and reviewed and distributed by Stacker.