What happens when you make minimum payments

What happens when you make minimum payments

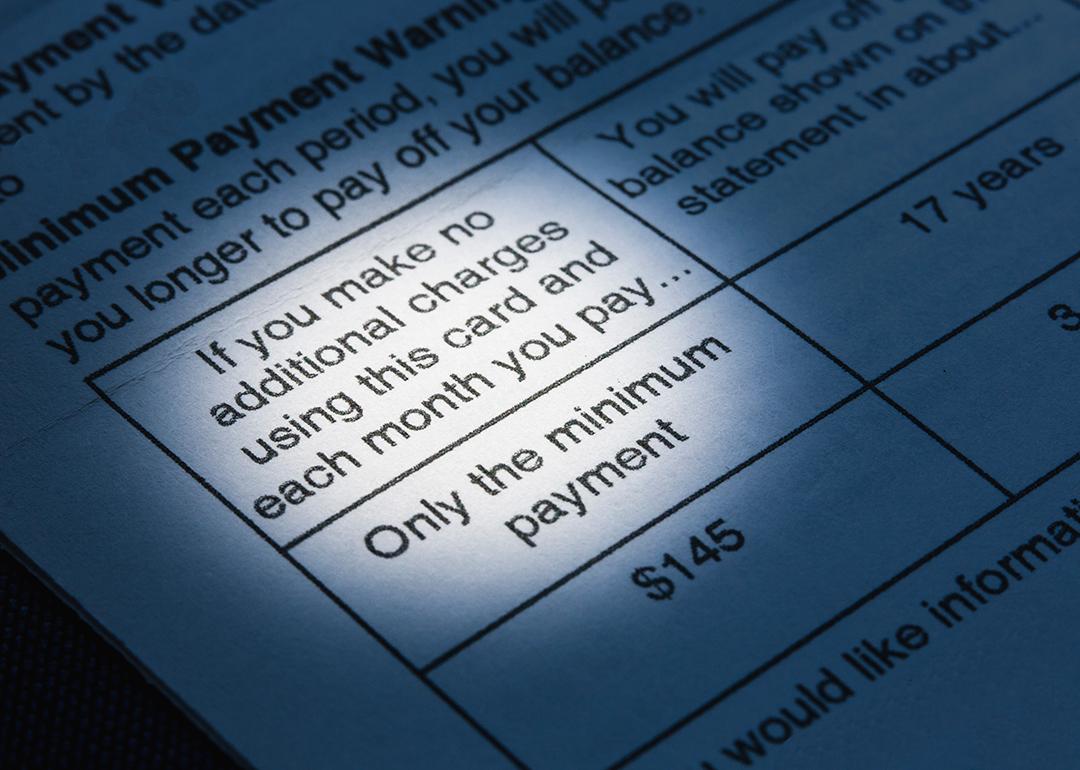

Every credit card bill includes a minimum payment warning — required by law — that shows how long it will take and how much it will cost to pay off your balance if you only make the minimum payment. Most people barely notice it.

More than one in nine credit card holders at the nation’s largest banks made only the minimum payment on their balances, according to the Federal Reserve Bank of Philadelphia. For millions of households facing rising costs, minimum payments can quietly keep debt around for years.

The financial experts at Accredited Debt Relief explain what really happens when you only pay the minimum — and why it’s important to understand the long-term impact.

What are minimum payments?

Minimum payments are the least amount you can pay monthly on your debt without incurring penalties. Every creditor calculates minimum payments differently. Most minimum payments are calculated as a percentage of the principal balance owed.

Typical minimum payments are two to four percent of your principal balance or a fixed floor rate, whichever is greater.

For example, a typical fixed floor amount is around $25 to $35. To remain in good standing, you must pay at least this amount until your principal is less than the floor. Most creditors will ask you to pay off the balance in full when this occurs.

Is making minimum payments a good idea?

Making minimum payments keeps your account in good standing, but it is the slowest and most expensive way to pay back your debt.

Making minimum payments does:

- Prevent late fees

- Prevent derogatory marks on your credit score

- Keep you in good standing with your creditor

Making minimum payments does not:

- Save money on your debt

- Pay off debt faster

- Lower your DTI quickly to improve creditworthiness

Minimum payments are not consumer friendly

At first, minimum payments seem like a good deal. You can borrow large amounts of money or use credit without having to pay a lot up front. Unfortunately, paying a little now means you’ll end up paying much more over time.

Minimum payments can extend your debt repayment timeline to 30 years or more, which benefits the creditor!

What happens if you pay more than the minimum payments?

When you pay more than the minimum payment on your debt, you pay down your principal balance faster.

The principal is the total amount you borrowed.

Interest is what you pay the creditor as a fee for borrowing the money.

With most debts, each payment is applied to interest and fees first. Only what’s left goes toward reducing the principal. When balances and interest rates are high, minimum payments often cover mostly interest, making it slow to shrink what you actually owe.

You can estimate how much of a payment goes toward interest by calculating your monthly interest charge:

(APR ÷ 100 ÷ 12) × current balance

Subtracting that amount from your payment shows how much is applied to the principal. The more you pay above the minimum, the more of your money goes toward reducing the balance itself.

The amount of principal vs. interest paid

For example, on a credit card with a 23% interest rate and a minimum payment of 3%, a $1,000 balance requires a $30 minimum payment. Of that payment, about $19 goes toward interest, while only $11 reduces the principal.

This is how credit card debt keeps people stuck. Even when you make your minimum payment on time, most of your money is going toward interest charges — not toward lowering what you actually owe.

As balances grow, interest takes an even larger share of each payment, slowing progress and extending debt for years. Without paying more than the minimum, it can feel like you’re doing everything right while barely moving forward.

This example is for illustrative purposes. Actual interest charges vary based on your card issuer, billing cycle, and balance calculation method, but they reflect how credit card minimum payments are typically applied.

Will making minimum payments hurt my credit?

Making minimum payments prevents you from delinquency, which is good for your credit score, but because it is a slow and expensive way to pay back debt, it can still affect your creditworthiness.

DTI or Debt-to-Income Ratio compares your total debt to your income. Since your income isn’t listed on your credit report, DTI won’t affect your score. However, lenders will look at your DTI, so it can affect your ability to take on new debt as well as the interest rate you receive.

Is there a better way to get out of debt?

Paying more than the minimum is one of the most effective ways to reduce debt, since it lowers interest costs and speeds up repayment. But not everyone has the flexibility to make larger monthly payments or pay down balances in lump sums.

If that isn’t realistic, borrowers may need to look at other options, such as consolidating multiple debts into a single payment or speaking with a financial or debt professional to review structured repayment or relief options. These approaches can help create a clearer plan for managing balances when minimum payments are the only affordable short-term option.

The best approach depends on your income, total debt, and financial circumstances — but understanding when to explore alternatives can help prevent debt from lingering longer than necessary.

This story was produced by Accredited Debt Relief and reviewed and distributed by Stacker.