What you need to know about a $50,000 personal loan

When you’re ready to make big moves in your life, you may need more resources. A large personal loan could offer the funds you need quickly and affordably, with steady payments that you can plan for in your monthly budget.

It’s wise to learn more about how a large debt works before you apply for something like a $50,000 personal loan. That way, you can assess how likely you are to be approved and how you’ll manage repayment of your loan. Achieve compiled this guide to help consumers understand large personal loan options.

Key takeaways:

- Lenders may have higher requirements to approve a $50,000 unsecured personal loan compared to smaller loans or secured loans.

- Calculate how much you truly need to borrow, so you can match your loan to your goals.

- Comparison shop for loan options to make sure you’re landing the best deal from a lender you trust.

What you need to know about a $50,000 personal loan

Most personal loans are unsecured loans. Unsecured loans are not attached to collateral. Collateral is something of value that you pledge as a guarantee that you’ll repay the loan. Collateral is a safety net for lenders. If you don’t repay the loan, the lender could sell your collateral to recover the money you owe.

Lenders typically charge slightly higher interest rates on unsecured debts because you don’t put up something of value to guarantee the loan.

Even so, there are many advantages to unsecured personal loans. You could receive your money quickly—sometimes as fast as just a few days. Personal loans also generally come with fixed interest rates, so your payment amount stays the same each month until the loan is paid off.

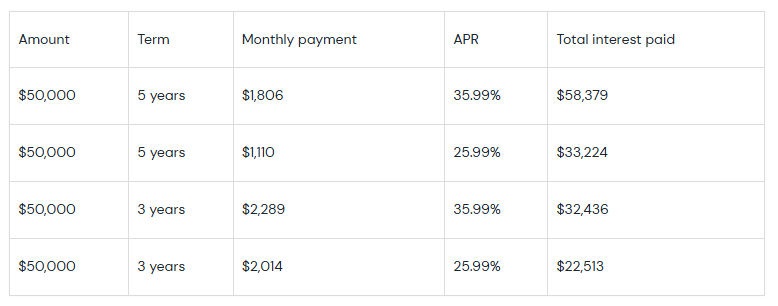

Monthly payment and cost examples

Many people focus on the monthly payment when they take out a personal loan. That’s an important consideration to ensure it fits within your budget, but it’s a smart idea to also look at the fees and total amount of interest you’ll pay over the life of your loan. After all, this is the price tag of the loan itself.

You could use a personal loan calculator to see the total cost of the loan by the time you pay it off. You’ll need the annual percentage rate (APR), which includes the yearly cost of fees and interest, the term length, and the loan amount.

Here’s how the same $50,000 personal loan looks with different interest rates and terms. A lower interest rate means you’ll pay less interest over the life of the loan. A shorter term means your monthly payments will be higher, but you’ll also pay less interest overall compared to the same loan spread out over more years.

This table is for informational purposes only. Interest rate and payments are for illustrative purposes only. Individual results vary.

Common uses for a $50,000 personal loan

A key advantage of personal loans is their flexibility. Everyone’s a bit different, after all, and a personal loan could be used to pay for just about anything. People commonly use personal loans so they can:

- Pay for emergency expenses

- Make major home repairs and upgrades

- Consolidate higher-interest credit card debt

- Cover major medical expenses

- Cover moving expenses

How to qualify for a $50,000 personal loan

Anyone can apply for a large personal loan and could qualify if they meet the requirements, which vary from lender to lender. Here are examples of what the lender might want to see for a $50,000 personal loan:

- Credit score: Expect lenders to look for a minimum credit score. The minimum varies.

- Income: The lender will want to see that your income is sufficient to cover your monthly payments and other living expenses.

- Debt-to-income (DTI) ratio: Your DTI is the percentage of your income that goes to required debt and housing payments. The lender’s requirement may vary.

Many banks and credit unions will show you regular credit score updates for free right on your account dashboard when you log in or on your monthly statement. You could also use other free credit score websites online.

Lenders generally don’t have a minimum income requirement in order to qualify for a loan, even though they’ll consider it to evaluate whether you’re able to make your payments. Only you can decide whether a loan is affordable or not, so it’s helpful to prepare a monthly budget that includes your income and expenses to make sure you can afford the loan payments before you apply.

To check your DTI ratio, first add up all of your minimum monthly debt payments. Include your housing payment as well as child support or alimony you have to pay, but don’t include your utilities or other expenses.

Divide the total by your total before-tax household income.

For example, let’s say you earn $4,000 per month and your rent is $1,200, your car loan is $300, and the minimum payment on your credit card is $125. Your DTI is a little under 41%.

1625 ÷ 4,000 = .406 (or 40.6%)

If your DTI ratio is higher than you want it to be, there are two ways to lower it:

- Lower your monthly debt payments

- Increase your monthly income

Steps to apply for a $50,000 personal loan

- Choose a loan amount: It’s a good idea to borrow only what you need. Try to estimate what you need as precisely as you can, based on how you’ll use the funds.

- Gather financial documents: You’ll need to submit certain financial documents when you’re ready to apply for a loan, and collecting them now could also help you prepare. Scan and save copies of your government-issued ID and recent bank account statements, pay stubs, and tax returns.

- Compare personal loan estimates: It’s always a smart move to shop around to compare lenders and loan terms. Pay close attention to how you’re treated when you research your options, as well as the APRs and monthly payment amounts proposed.

- Submit a full personal loan application: Choose your preferred loan option and proceed with your personal loan application.

- Communicate with your lender: Your lender will begin reviewing your loan application. Keep in touch with them, because it’s not unusual for lenders to request additional information before making a decision.

What to expect after a $50,000 personal loan is approved

Your lender will let you know as soon as they’ve reached a decision about your loan application. If you’re approved, they’ll typically send the funds to you within a few business days, generally by depositing the money into your account.

If your lender charges any application or origination fees, these may be taken out of your loan amount, so you’ll receive slightly less than you applied for. If you apply for a $50,000 loan that charges a 5% origination fee, for example, you’ll receive $47,500 in your bank account after the $2,500 fee is taken out.

You’ll generally begin repaying your personal loan immediately, and your lender will let you know when your payment is due each month. With a fixed-rate loan, your payment will stay the same until you’ve paid off the entire debt. Some lenders will let you make extra payments toward your loan or even pay it off early without charging you any penalty fees. This could be a great way to lower your interest costs and get rid of the debt even sooner.

What's next

- Check your monthly budget to decide whether you can afford the payment on a new $50,000 personal loan. To get an idea of the payment amount, plug different loan terms and interest rates into an online loan calculator.

- Check your credit score, income, and monthly financial obligations against the qualifications lenders look for. If you’re not sure what they look for, chat with a loan officer.

- When you have the loan, sign up for autopay to reduce the chance of missing a payment. Missed payments could lead to credit score damage and late fees.

This story was produced by Achieve and reviewed and distributed by Stacker.