The 10 cities where VA home loans are most common

U.S. veterans are foundational to America’s identity. However, they have long faced unique challenges transitioning back to civilian life. To help, the government has introduced various programs over the decades aimed at supporting veterans with education, employment, and housing. One of the most impactful steps was the GI Bill, passed in 1944, which established the VA home loan program.

VA loans are a low- to no-down payment option available to qualifying veterans, active-duty service members, and their surviving spouses. It’s one of the most powerful tools available to veterans and has helped millions gain access to homeownership. And after dipping in recent years, VA loan use is climbing again.

Nationwide, 7.3% of mortgaged homebuyers used a VA loan in August 2025, up from 6.5% a year earlier and the highest share for that month since 2019. The number of homebuyers using VA loans has also increased, rising 3% year over year, while conventional loan use declined by 9%.

Redfin Real Estate looks at cities where VA loans are most common and what’s behind the upward trend.

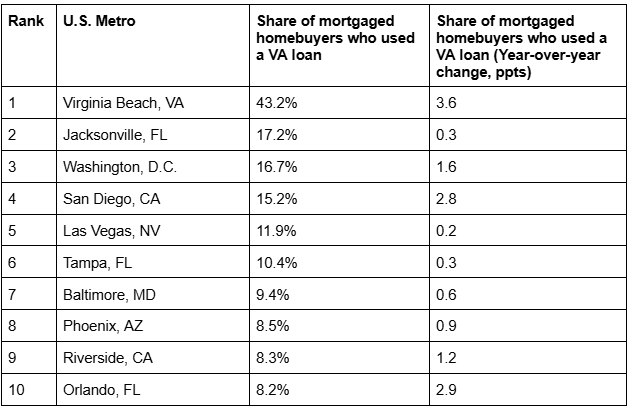

US cities with the highest shares of VA loans, August 2025

VA loans are largely clustered in cities with a major military presence, led by Virginia Beach, Virginia, Jacksonville, Florida, and Washington, D.C. Virginia Beach, which saw the largest increase in VA loan use since last year, also has the largest concentration of active military personnel outside the Pentagon. Nearly 100,000 active-duty military members are stationed in the region across the Air Force, Army, Coast Guard, Marine Corps, Navy, and NATO.

The Jacksonville area is home to several military facilities, including naval stations and a submarine base; Washington, D.C., is home to the Pentagon and a handful of military bases. Rounding out the top five are San Diego for the Navy and Las Vegas for the Air Force.

Around the country, VA loans have become more common because of today’s strong buyer’s market. More sellers are willing to accept offers with low down payments — contrasting with the ultrastrong seller’s market of the pandemic era, when higher down payments were preferred. For example, in late 2020 and early 2021, when mortgage rates were at record lows, less than 6% of mortgaged homebuyers were using VA loans.

Sellers prefer higher down payments in a more competitive market because they want to maximize their profit. But in slower markets, sellers may not receive a lot of offers and may be open to accepting one with a lower down payment.

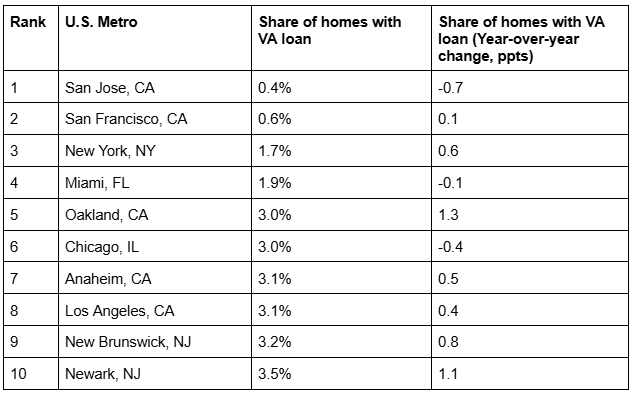

US cities with the lowest shares of VA loans

VA loans are least common in the nation’s most expensive metros, especially those without a major military base. A low concentration of veterans or service members usually means fewer purchases made using VA loans. Three of these metros also saw declines in overall VA loan use year over year.

New Brunswick and Newark, while not particularly pricey, are also less popular among veterans. This could be due to having fewer veterans or service members overall, and the fact that both metros are among the remaining seller’s markets, where sellers are more likely to be choosier.

What is a VA loan?

VA loans are a type of assumable mortgage guaranteed by the U.S. government. They offer one of the lowest-barrier ways to buy a home, usually requiring no down payment and no private mortgage insurance. However, there are important eligibility requirements to keep in mind, like time in service and type of property.

What does the future of VA loans look like?

Although VA loans are becoming more common, only a small share of homebuyers use them. Even when combined with FHA loans — another low-cost, government-backed mortgage — they represented less than a quarter of all buyers in August, compared to the 79% of home loans that were conventional.

VA loan use is relatively low because they’re only available to a small portion of the population. And, even in today’s buyer’s market, some sellers still favor those with larger down payments. The share could still be much higher, though: A recent analysis by Veterans United Home Loans found that qualified veterans underutilized $28 billion worth of VA loans in 2024 alone.

VA loans are a vital tool to help veterans own the American Dream by providing a low- to no-down payment path to homeownership. More awareness, stronger protections, and continued policy support will help ensure veterans can fully access and benefit from the program they’ve sacrificed themselves for.

Methodology

This story is based on an October 2025 Redfin report, which analyzed county records across 40 of the most populous U.S. metropolitan areas. August 2025 is the most recent month for which data is available. Data on loan types is limited to home purchases for which buyers took out a mortgage, and thus excludes all-cash purchases.

This story was produced by Redfin Real Estate and reviewed and distributed by Stacker.