Cash-out refinance vs. HEI

Accessing the equity in your home can help you move forward on your financial goals, whether you’re planning major renovations, consolidating high-interest debt, or building long-term stability. Cash-out refinances have long been a familiar option, but rising mortgage rates have prompted many homeowners to explore alternatives, including home equity investments (HEIs).

In this guide, Splitero explains how each option works, what makes them different, and how to decide which one may be the right fit for your financial situation.

Key Takeaways

- A cash-out refinance replaces your existing mortgage with a new, larger one and gives you the difference as cash. This typically results in a new interest rate, a new loan term, and a new monthly payment.

- A home equity investment (HEI) provides a lump-sum payment in exchange for a share of the home’s future value, with no monthly payments or interest. An HEI does not replace your existing mortgage.

- Cash-out refinances function like traditional loans, with repayment based on interest rates and a fixed term, while HEIs operate as investments, which are repurchased later based on your home’s value.

- Both options help you access your home’s value but differ in cost structure, qualification requirements, and how repayment or repurchase is handled.

What is a cash-out refinance, and how does it work?

A cash-out refinance allows you to replace your current mortgage with a new, larger one and receive the difference in cash. Unlike a rate-and-term refinance (which simply changes your interest rate or loan term), a cash-out refinance increases your loan balance.

At closing, the lender pays off your existing mortgage and issues a new loan for a higher amount. You will receive the extra funds, and your monthly payment, interest rate, or loan term changes based on current market rates, your credit score, and other qualification requirements your lender may have.

According to the Intercontinental Exchange’s August 2025 Mortgage Monitor report, this strategy has been increasingly popular. Cash-out refinances accounted for 59% of all refinance transactions in Q2 2025, and those borrowers withdrew an average of $94,000 in home equity. However, those borrowers also increased their monthly mortgage payment by about $590 on average.

Pros

- Potentially lower rate: For homeowners whose existing rate is above today’s market rate, a cash-out refinance can lower borrowing costs while also providing access to equity.

- Familiar repayment structure: A cash-out refinance keeps your financing consolidated into one predictable mortgage payment over a set term, which some homeowners find easier to manage than juggling multiple payments or alternative structures.

- Opportunity to restructure your mortgage term: A refinance allows you to select a new term length. Some homeowners choose a longer term to reduce their monthly payment, even when taking additional cash, while others use a shorter term to pay off their home faster.

Cons

- Higher monthly payments: Even if you’re refinancing at a lower rate than your current mortgage, a cash-out refinance could still result in higher monthly payments because your total principal balance will be higher than your original term. Additionally, if you have a qualifying credit score, but it’s not relatively high, you may not receive favorable loan terms, which can result in a higher interest rate.

- Longer repayment timeline: Refinancing resets your amortization schedule. Even if the monthly payment feels manageable, restarting a 30-year clock can increase total interest paid over time.

- Strict qualification requirements: Cash-out refinances rely heavily on credit score, income documentation, and debt-to-income ratios, which may limit eligibility for homeowners with nontraditional income or lower credit scores.

What is a home equity investment (HEI)?

A home equity investment, or HEI, provides a lump-sum cash payment in exchange for a share of your home’s future value. Your home may appreciate or depreciate during your term, and the investor shares in that change when you repurchase your investment option.

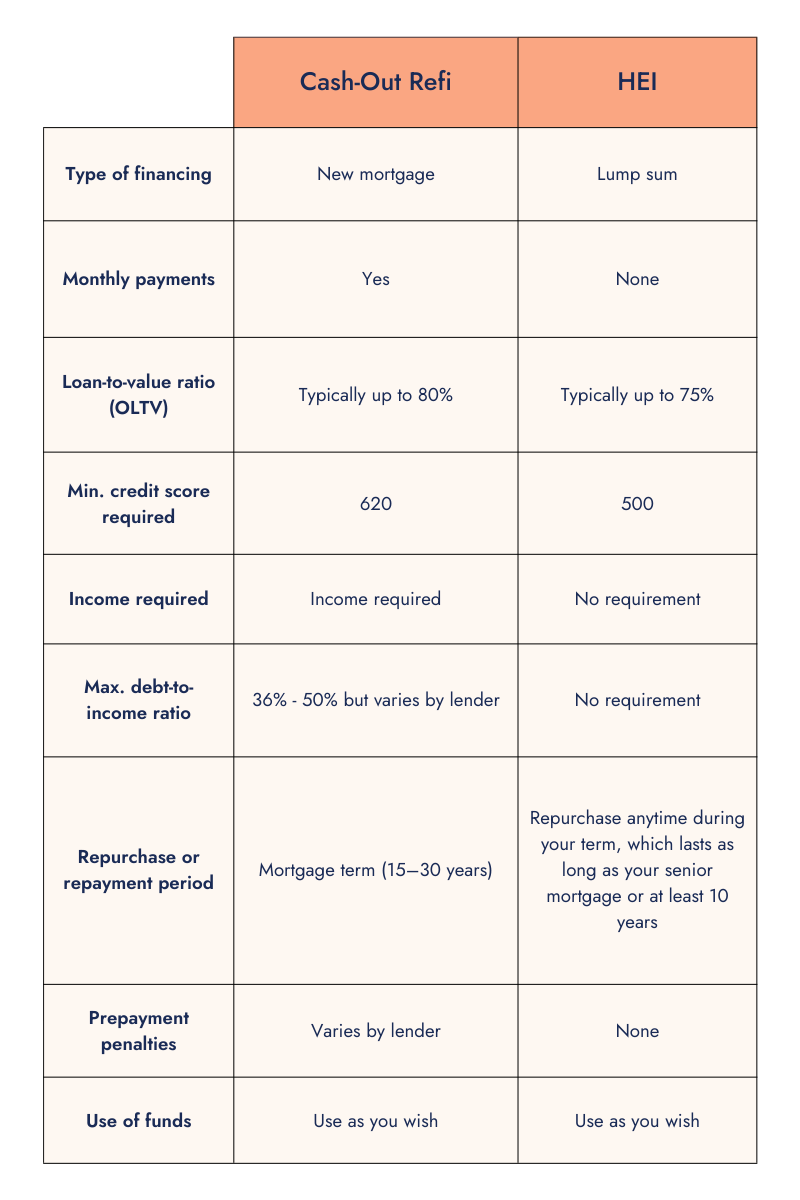

Your HEI term generally lasts at least 10 years. At the end of your term, you settle the investment by repurchasing your share at the home’s then-current value.

There are several ways to repurchase your investment, including a cash settlement, refinancing, or using proceeds from a home sale. There are no monthly payments, and you can repurchase your investment option at any time during your term.

Pros

- No monthly payments: HEIs don’t require monthly payments. Instead, you can repurchase your investment at any time during your term.

- Low qualification requirements: HEIs typically have a much lower minimum credit score requirement than traditional financing options and do not require income verification.

- Shared downside protection: If your home depreciates over the course of your investment term, the investor shares in that loss with you, as your repurchase amount is not a fixed dollar amount.

Cons

- Limited availability: HEIs are a relatively new financing option and aren’t yet available in every U.S. state.

- Limited refinancing flexibility: Some lenders may require you to settle your HEI before refinancing or taking out additional home loans.

- Repurchase cost varies with home value: Your repurchase amount is impacted by your home’s future value. While an agreed-upon percentage at closing typically dictates your repurchase amount, if your home appreciates rapidly over the course of your investment term, the final repurchase amount may come as a surprise. However, some HEI companies include safety caps that prevent your repurchase amount from exceeding a certain threshold.

What’s the difference between a cash-out refinance and an HEI?

Cash-out refinances and HEIs differ in several key aspects, including structure, monthly payment obligations, and how costs are calculated:

- Mortgage vs. investment: A cash-out refinance is a new mortgage on your home that provides you with cash. You make monthly payments like any other mortgage. An HEI, on the other hand, provides you with a lump sum of cash without monthly payments. You repurchase the investment at any time before or at the end of your term.

- Monthly payments: Once your cash-out refinance is finalized, you make monthly payments like any other mortgage until both the principal and interest are both paid down. Home equity investments do not require any monthly payments.

- Qualification: Like other mortgage products, cash-out refinances require verifiable income and decent credit to qualify. Most lenders require a credit score of at least 620, and you typically need a higher score to secure better loan terms. Alternatively, HEIs do not require income verification and have lower credit score requirements, usually around 500.

- Risk sharing: With a home equity investment, the investor shares the risk of the home’s value decreasing but also has the potential for a greater return if the home’s value increases. With a cash-out refinance, your payments do not decrease if your home’s value decreases.

Comparison table: Cash-out refinance vs. HEI

Cash-out refinance vs. HEI: Which is best for you?

If you’re trying to decide between a cash-out refinance and an HEI to access your home equity, the best option will depend heavily on your specific financial situation. However, here are a few initial considerations that may help you begin narrowing down your options:

- Your current mortgage status: If you do not have a current mortgage or have a mortgage with a favorable rate, pursuing a cash-out refinance may result in an increased interest rate and new or higher monthly payments. Even if the interest rate is lower, a higher loan balance may still increase your monthly payments. If you know you can secure a better rate than your current mortgage and are comfortable with a new monthly payment, a cash-out refinance can be a great option. In contrast, if you would prefer a financing option that does not impact your current mortgage, an HEI may be the best option for you.

- Your credit score: If you have a strong credit score, either option may work for you. If your credit score is below typical lender requirements, you may struggle to qualify for a cash-out refinance or secure favorable loan terms, making an HEI more accessible.

- Your employment status: If you are retired, unemployed, or self-employed, an HEI may be easier to qualify for because cash-out refinances typically require income documentation.

- Your financial goals: If you plan to use the funds for a major purchase or long-term financial objective and do not want to adjust your current mortgage to accommodate this, an HEI may be a better option because it avoids monthly payments and does not impact your current mortgage status.

- Monthly payments: If you’re not comfortable taking on monthly payments, an HEI may be a better option. If you would like to adjust or change your current monthly mortgage payment, a cash-out refinance may be the ideal option.

Considering these variables, here are a handful of circumstances in which one option may be better than the other:

Additionally, it's always important to weigh the risks and benefits of each option and consult a financial advisor or expert to help determine which is best for you.

Frequently Asked Questions

What is a home equity investment (HEI)?

A home equity investment gives you a lump-sum payment today in exchange for a share of your home’s future value. There are no monthly payments or interest, and you keep your existing mortgage. Your agreement term lasts as long as your senior mortgage or at least 10 years.

What is a cash-out refinance?

A cash-out refinance replaces your current mortgage with a new, larger mortgage and gives you the difference as cash. You receive a new rate, a new loan term, and a new monthly payment based on the updated balance.

What’s the difference between a cash-out refinance and an HEI?

An HEI and a cash-out refinance both provide you with a lump sum of cash, but only a cash-out refinance comes with monthly payments. A cash-out refinance replaces your existing mortgage (or provides you with a new mortgage if you don’t currently have one), and includes a new mortgage rate and loan term. In contrast, an HEI provides a lump sum of cash with no monthly payments or interest, and you repurchase your investment option later based on your home’s value.

This story was produced by Splitero and reviewed and distributed by Stacker.