The great staying put: Why a record share of homeowners are cashing in without selling

Spring is typically one of the housing market’s busiest seasons. May and June are historically some of the biggest listing months of the year and are when “For Sale” signs and moving trucks dominate the streets.

This year, though, the season didn’t exactly show out. Cotality’s Home Price Index shows U.S. home prices rose just 0.3% year over year in April 2026, the weakest appreciation in years, and as of January about 34% of the 100 largest U.S. markets were posting outright year-over-year declines. Per Zillow’s April 2026 market report, new listings outpaced sales for the first time in 2026. Yet on paper, Americans have never held more housing wealth.

Splitero dug deep into data from the Federal Housing Finance Agency (FHFA), ICE Mortgage Technology, Zillow, and Cotality to show how rate-locks are preventing Americans from capitalizing on their paper wealth.

The rate-lock effect

The mechanics of the rate-lock effect are simple, but brutal. Take, for instance, a homeowner with a sub-6% fixed mortgage. They face an enormous financial penalty for selling and buying at today's rates. Trading a 3% rate for a 6.5% to 7% mortgage can add about $1,000 per month to the payment on a median-priced home. Many homeowners understandably decline this trade-off.

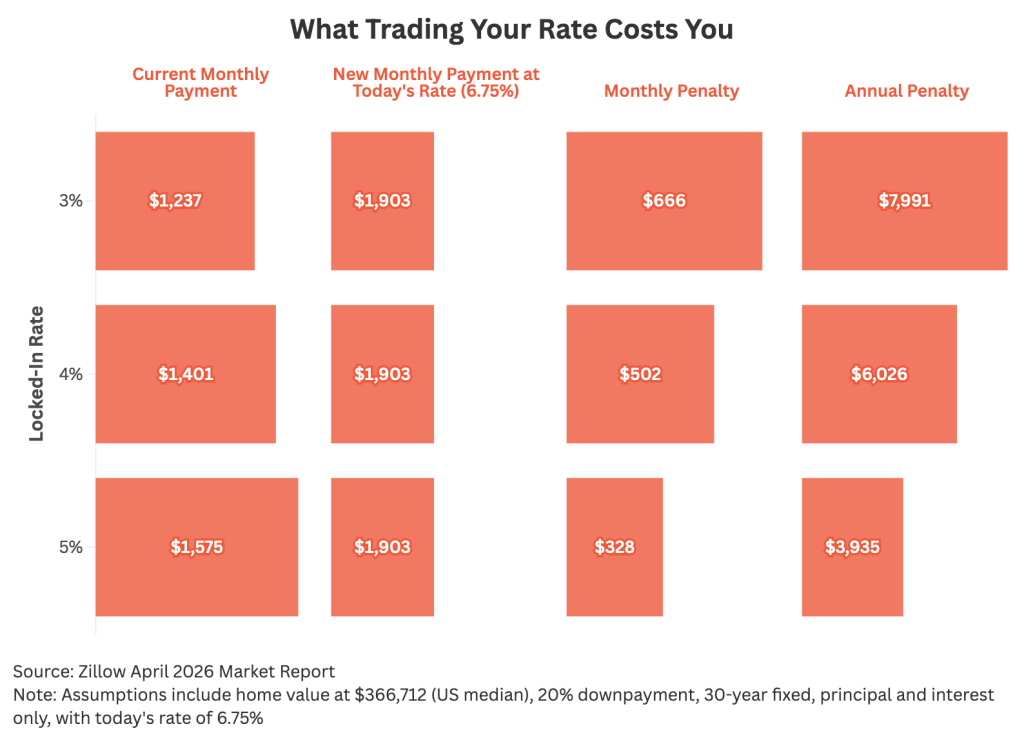

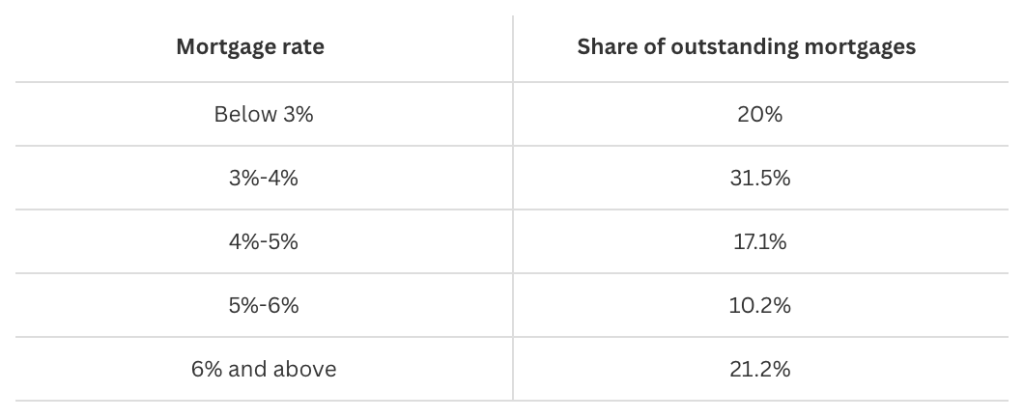

Trading a sub-4% mortgage for today’s 6.75% rate on the same median-priced home means paying anywhere from $3,900 to nearly $8,000 more every year, according to the Zillow April 2026 market report. The deeper the discount you’re giving up, the steeper the hit. Federal Housing Finance Agency data from the third quarter of 2025 shows just how deep that discount runs. More than half of homeowners are locked into a rate below 4%, and just under 80% sit below 6%.

The agency even quantifies the impact of this problem in a 2024 working paper. For every percentage point that market rates exceed the origination rate, the probability of a sale drops by 18.1%, according to their data. In plain terms, the higher today’s rates sit above the rate a homeowner already has, the less likely that homeowner is to sell. With most owners holding rates set well below current ones, the predictable result is a market where 1.72M fewer homes traded hands between Q2 2022 and Q2 2024.

That missing supply has a counterintuitive effect on price. With so few homes for sale, competition for the ones that do list pushed national prices up an estimated 7%, more than cancelling out the roughly 5.6% downward pull that higher rates would have had on their own. So even as demand cools, prices have stayed stubbornly high.

Record equity, and almost no one is touching it

The lock-in effect doesn’t just stop people from selling. It also reshapes how they reach the money tied up in their homes. U.S. owners are sitting on record equity but are disincentivized to access it through sales or cash-out refinancing.

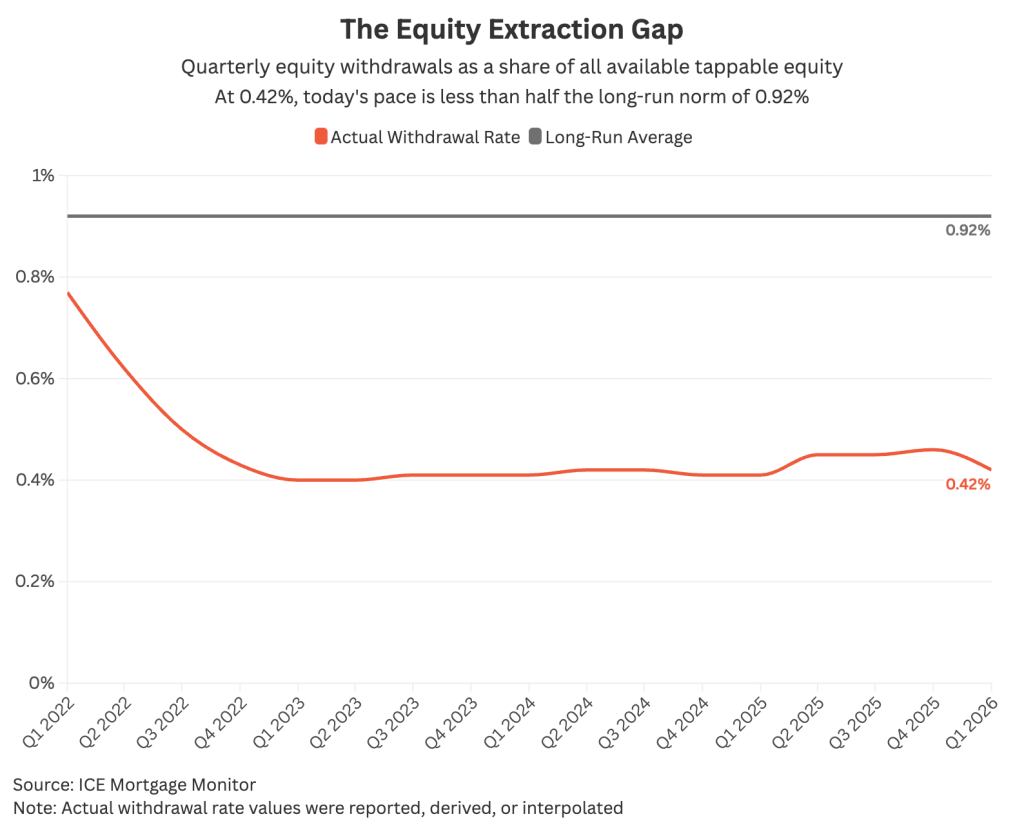

According to ICE Mortgage Monitor data, however, equity withdrawals in the first quarter of 2026 rose 2% year over year and hit their highest first-quarter level since 2021. This is still far below the long-run historical norm.

The preferred method for those accessing equity today without selling is taking out second liens, often home equity lines of credit (HELOCs), which leave the existing first mortgage untouched. Per the same ICE data, in the first quarter 2026, 54% of all equity extraction came through second liens, leading to second-lien lending reaching an 18-year high. This equates to 3.9 million homeowners from 2020 to 2022 who have now added a second lien.

Similarly, average HELOC introductory rates fell to 6.6% in March 2026, which is their most attractive level since late 2022. A $50,000 withdrawal today costs roughly $275 per month, which is down significantly from highs in early 2024. Despite the potential for lower HELOC costs, withdrawal rates for second liens are still below historic norms.

While homeowners are still extracting equity using secondary methods other than selling or refinancing, it’s a barren market compared to past years.

The hard part isn’t having equity. It’s getting to it.

Record equity doesn’t help much if you can’t reach it. Homeowners are sitting on trillions of dollars in equity, much of it gated behind the qualification hurdles that traditional products demand. HELOCs, cash-out refinances, and home equity loans typically require income verification, strong credit, and a debt-to-income check, and a refinance also means giving up the low first-mortgage rate that locked owners are trying to protect.

That gap is part of why home equity investments (HEIs) have grown as an alternative. Instead of a monthly payment, an HEI provides cash today in exchange for a share of the home’s future value, with no income verification and credit-score minimums that can start around 500. For an owner who is equity rich but doesn’t qualify for, or doesn’t want a new monthly payment, it’s one of the few ways to access equity without selling or refinancing.

What would break the lock-in effect?

Breaking the lock-in effect comes down to closing the gap between the rates owners already hold and the rates they’d face if they moved, and a few conditions would have to line up for that to happen.

There are hopeful signs. Inventory is growing, and rates have edged down from 2025 highs. Homebuyers in April 2026 had roughly 3% more purchasing power than a year earlier.

The first factor that could mark a major change is a return to the 6% range on 30-year fixed mortgages. This could trigger a meaningful rebound in buyer demand, according to Zillow.

Additionally, the share of mortgages locked at sub-3% naturally erodes over time. This gradual "aging out" of ultra-low-rate cohorts slowly releases inventory back into the market. HELOCs can also act as a pressure valve. Homeowners who need liquidity are leveraging equity via second liens rather than selling, which preserves inventory tightness.

The future of the housing market

The great “staying put” isn’t caused by stubbornness. Tens of millions of households have a valuable asset they locked in at an affordable rate, but it vanishes the minute they choose to sell. Instead, those homeowners have chosen to stay longer, renovate their properties, and continue to build record-setting equity. Until mortgage rates fall or enough low-rate loans drop out of the system, we’re likely to continue to see more of the same.

This story was produced by Splitero and reviewed and distributed by Stacker.