Many homeowners feel traditional lenders don't have their best interests at heart. New data explains why.

A new survey of 1,000 U.S. homeowners reveals a striking disconnect between how the financial industry designs home equity products — and how homeowners actually experience them. The gap has real consequences for both sides.

The findings, from an October 2025 survey conducted by Hometap, show that the majority of homeowners approach equity financing through a lens of emotional stress, income uncertainty, and a desire for flexibility. While most lenders lead with rate comparisons and amortization tables, homeowners are actually looking for an empathetic financial partner.

Homeowners Tap Into Equity Because Life Happens — Not Because the Timing Is Right

Homeowners rarely access equity as part of a pre-planned financial strategy. Instead, they’re usually responding to unexpected life events: a job loss, a parent needing care, an upcoming college tuition bill, a failing HVAC system, or a growing family.

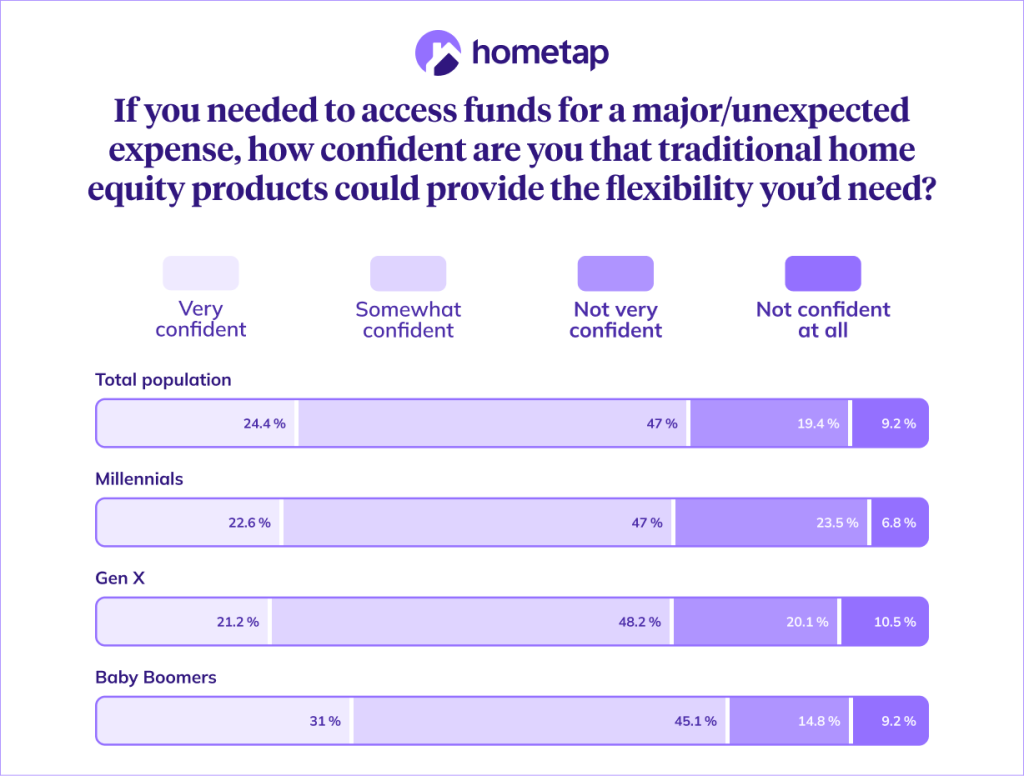

According to the survey, 65% of homeowners said their primary concern when financing home expenses is covering unexpected costs. The implication is significant: The majority of people reaching for home equity products need tools that can adapt to unpredictable circumstances, not ones with rigid structures built for stable, predictable financial situations.

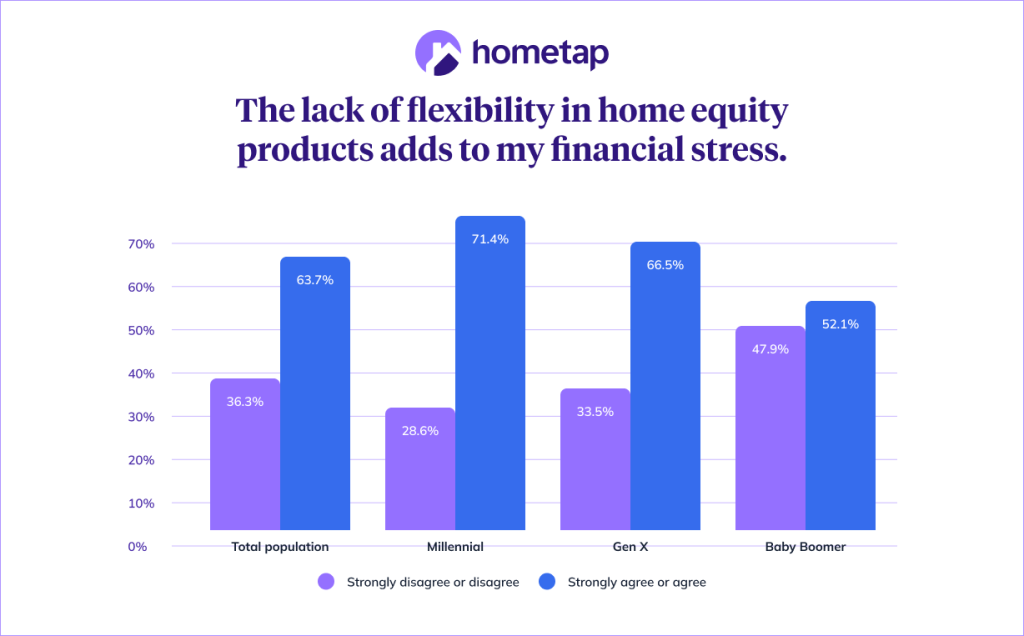

Generational differences are pronounced. Millennials and Gen X reported notably lower confidence in traditional products than baby boomers and expressed stronger demand for flexible alternatives. Among millennials specifically, 71% said that a lack of financing flexibility adds to their financial stress, compared to 52% of baby boomers. That gap is consistent with broader research: The NAR's 2025 Home Buyers and Sellers Generational Trends Report found that younger millennials carry the highest rates of student debt among all homebuying generations, shaping a distinct set of financial priorities centered on cost management and versatility.

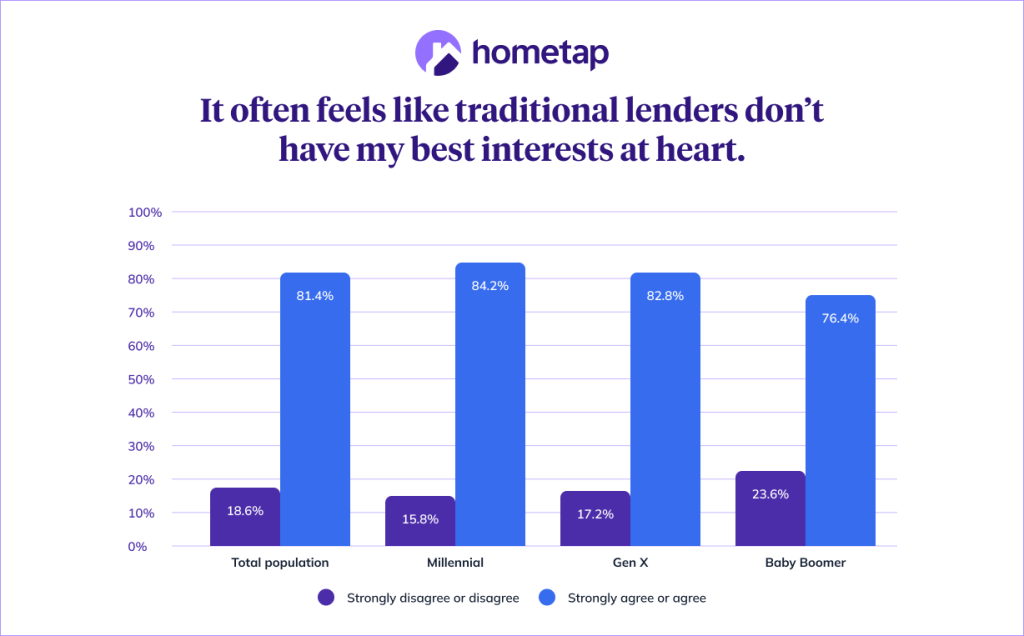

8 in 10 Homeowners Don't Trust Traditional Lenders

The survey's most striking finding: 81% of homeowners agreed that traditional lenders don't have their best interests at heart.

That distrust has direct market consequences. According to the survey data, 20% of homeowners have avoided traditional home equity products entirely due to rising rates and costs, while another 11% have delayed using them. When faced with a major funding need, only 8% said they would choose a home equity line of credit (HELOC) first, and just 5% said they would turn first to a traditional home equity loan.

Financial decisions often coincide with vulnerable moments — a job transition, a family crisis, a home emergency. When homeowners believe the lender across the table is optimizing for its own returns rather than theirs, avoidance becomes a rational response.

What Homeowners Are Actually Asking For

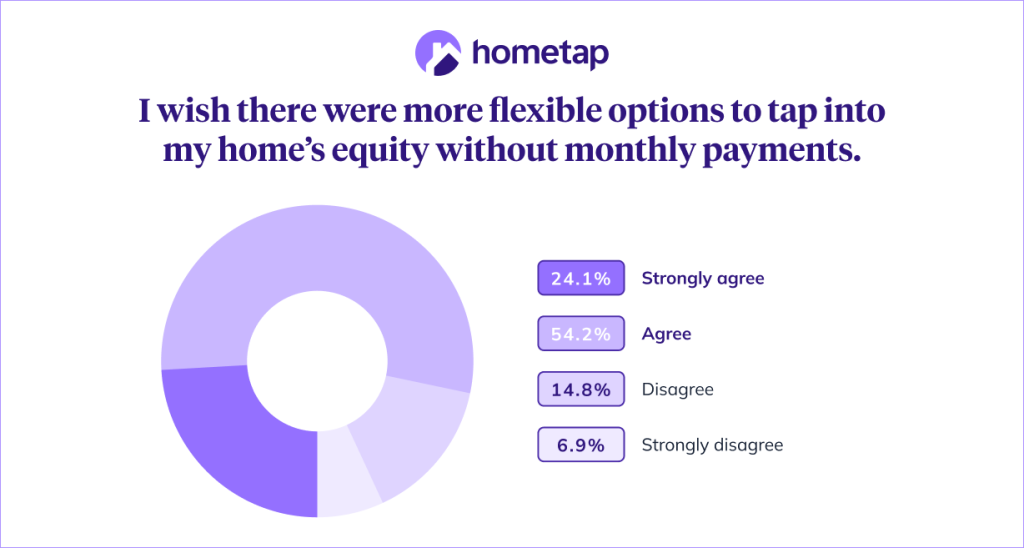

The survey found that 39% of homeowners said lower fees and closing costs were their top priority when choosing a financing product. The majority, 78%, said they wished there were more flexible options for accessing home equity without monthly payments. Among millennials, that figure rose to nearly 4 in 5.

"Flexible" in this context means a range of things: adjustable terms, the ability to pause payments when circumstances change, or alternative structures without a fixed monthly commitment. The survey found that 64% say the lack of flexibility adds to their financial stress.

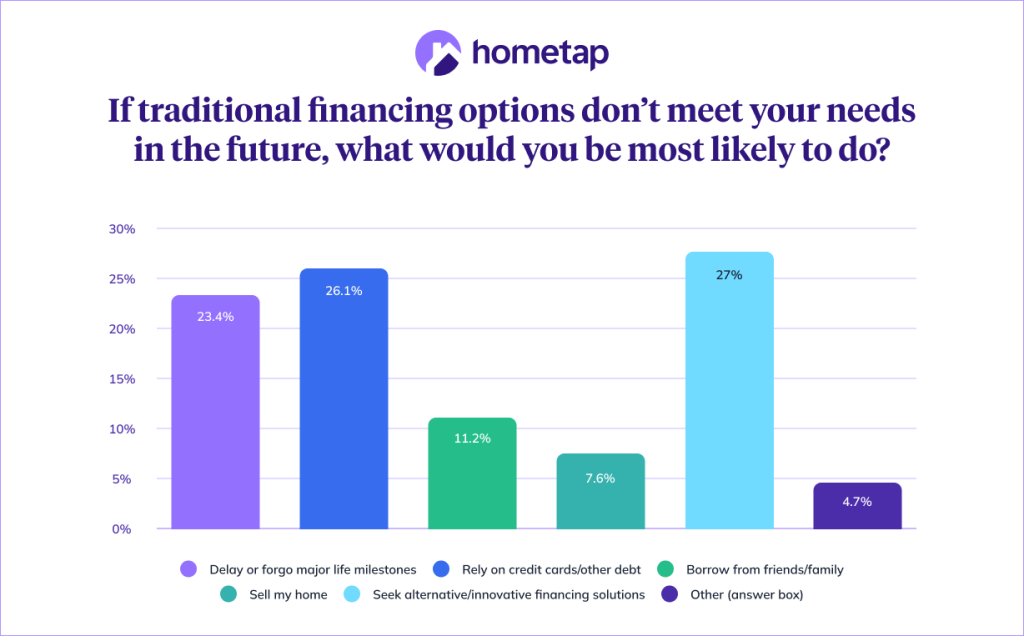

Meanwhile, 72% of respondents described the traditional home equity application process as outdated and difficult. More than a quarter said that if traditional options don't meet their needs, they would seek alternative or innovative financing solutions.

The Trade-offs of Alternative Products

One category drawing growing interest is home equity investments (HEIs), which allow homeowners to receive a lump sum in exchange for a share of the property's future value — with no monthly payments required during the investment term.

The trade-off is real and worth understanding clearly. If home prices appreciate significantly, the homeowner may give up more long-term value than a traditional loan would have cost, so HEIs are not the right fit for every situation.

For homeowners with stable income who can comfortably carry a monthly payment and want to retain full upside on their home's appreciation, traditional products often make sound financial sense. But for homeowners managing income volatility, navigating a job transition, or prioritizing near-term cash flow, trading some future appreciation for financial breathing room can be a rational choice.

The data suggests the industry has too often treated traditional products as a one-size-fits-all solution — a posture that may be accelerating the trust deficit.

A Market Signal Lenders Can't Ignore

The survey data reflects a market in transition. Three-quarters of homeowners said the industry needs new types of financing beyond traditional mortgages, HELOCs, and home equity loans. The generation most critical of current products — millennials — will shape the housing market for the next several decades.

Lenders that design products around how people actually live, rather than how financial models assume they live, may find themselves better positioned to capture a share of a market that is actively looking for alternatives.

Methodology: Hometap surveyed 1,000 homeowners in the U.S. ages 18 and older through AYTM (Ask Your Target Market) in October 2025.

This story was produced by Hometap and reviewed and distributed by Stacker.