Survey: Flexibility, low fees, and no monthly payments top homeowners’ wish list for equity financing

For millions of American homeowners, their home equity represents their largest financial asset. Yet, a growing share say the products designed to help them access that wealth feel outdated, rigid, and misaligned with how they actually manage their finances.

Hometap surveyed 1,000 U.S. homeowners to examine their sentiments toward traditional home equity products — including home equity loans, HELOCs, cash-out refinances, and reverse mortgages — and the features they wish those products offered. The October 2025 survey builds on a prior one from June 2025 that explored the broader financial pressures of homeownership.

The survey reveals a consistent mismatch between what traditional lenders offer and what homeowners across generations say they need. Their top priorities: lower costs, more flexibility, and the ability to tap equity without adding a new monthly payment.

Lower Fees Top the Wish List — But Flexibility Isn't Far Behind

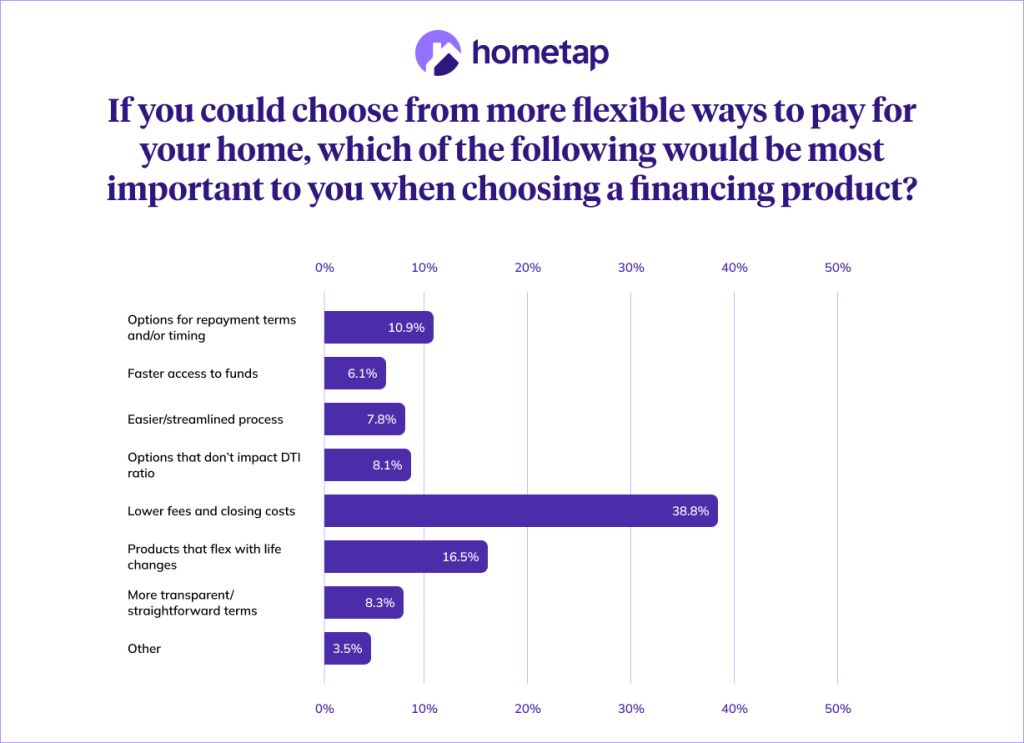

When asked to name the most important characteristic in a home financing product, nearly 39% of respondents cited lower fees and closing costs, making it the clear top priority. About 17% said they want products they can flex with life changes — such as the ability to pause or adjust payments — and roughly 10% prioritized additional repayment terms and timing options.

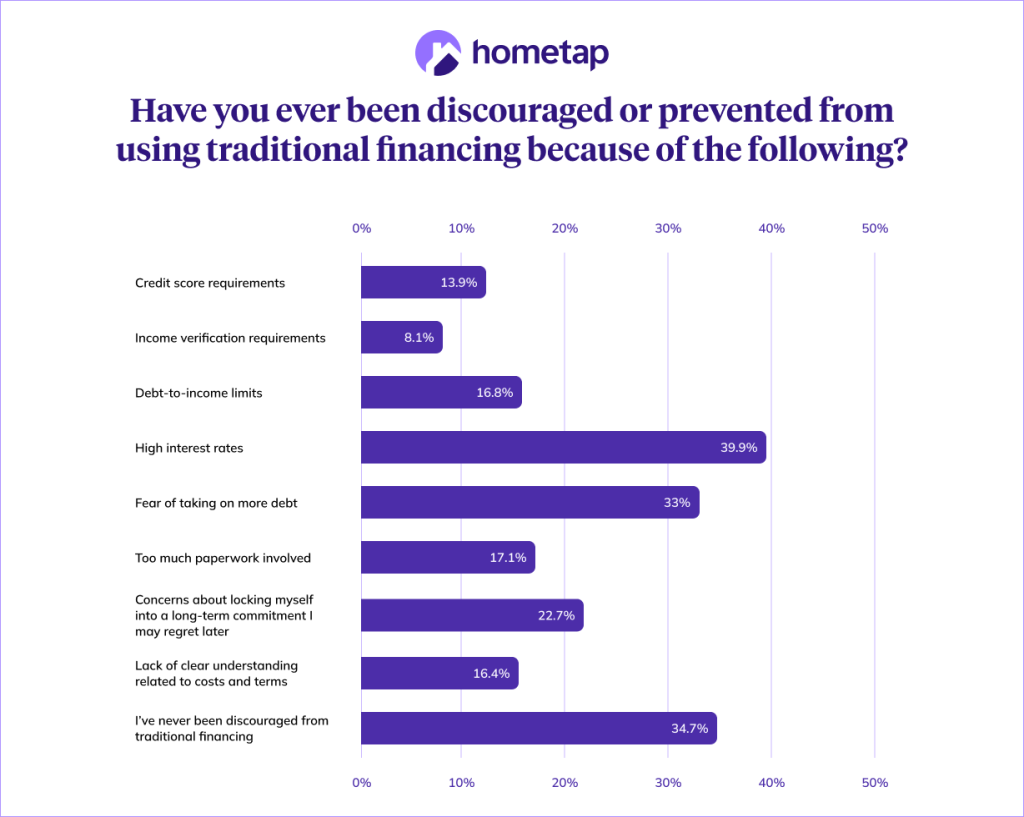

Those wishes directly contrast what homeowners say they encounter in practice. More than a third of respondents (36%) said traditional financial products don’t adequately fit the needs of today’s homeowners. High interest rates were the most commonly-cited deterrent to using traditional equity products (nearly 40%), followed by fear of taking on more debt (33%) and concerns about locking into long-term commitments (23%).

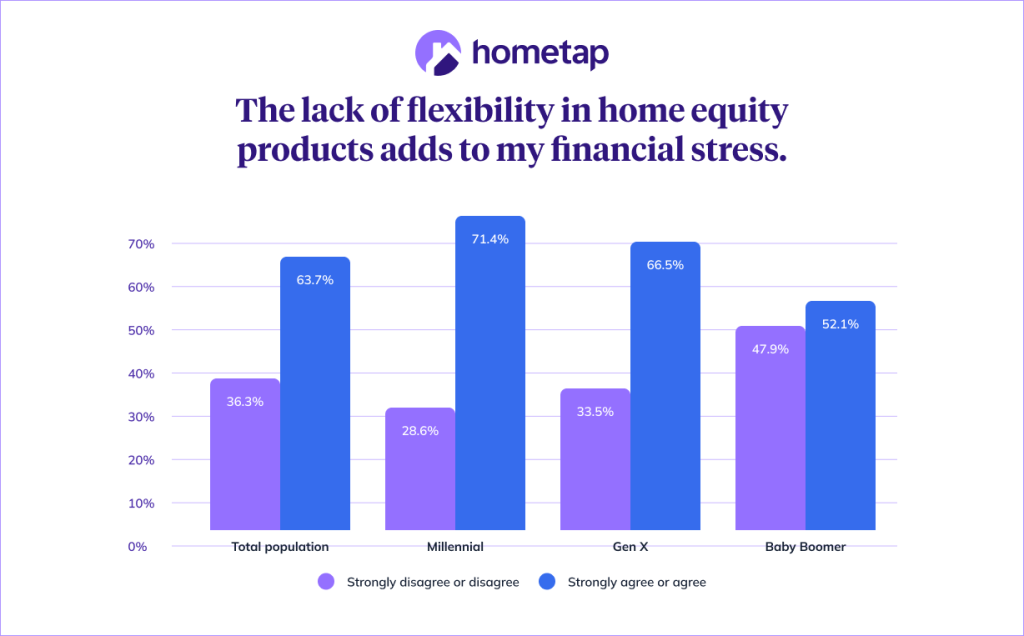

While the frustration spans generations, younger homeowners feel it most acutely. When asked whether the lack of flexibility in home equity products adds to their financial stress, 71% of millennials agreed or strongly agreed, compared to 66.5% of Generation X respondents and 52% of baby boomers.

Trust in Traditional Lenders Is Eroding

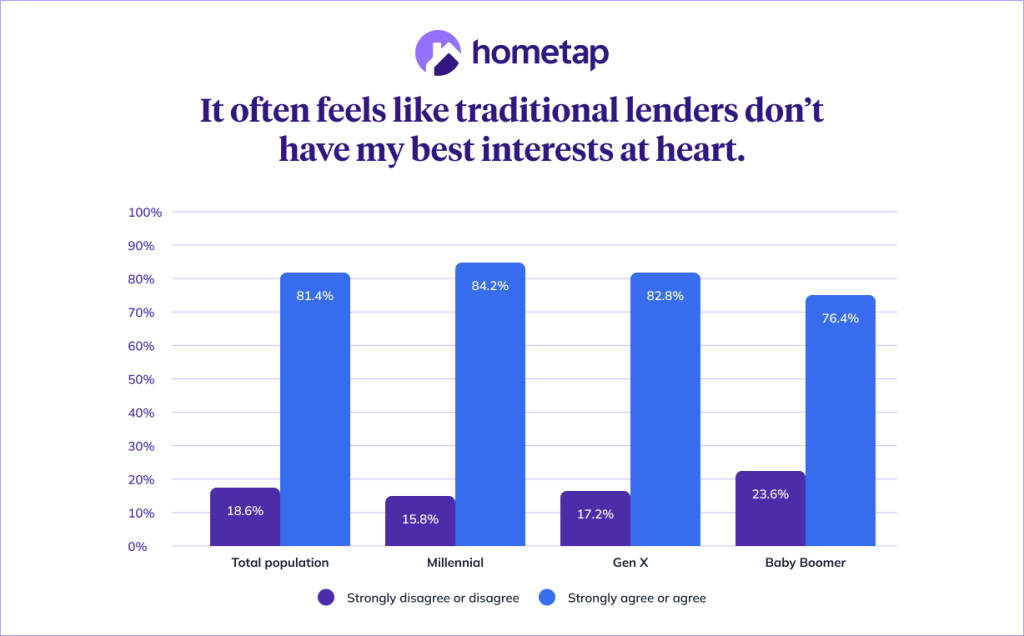

The survey also surfaces a significant trust gap between homeowners and the institutions that serve them. Across all age groups, the majority said it often feels like traditional lenders don’t have their best interests at heart: 84% of millennials, 83% of Generation X respondents, and 76% of baby boomers shared this view.

That skepticism may be reinforced by financial strain. The companion June 2025 Hometap survey found that 37.6% of homeowners said housing costs were preventing them from achieving other financial goals, with many delaying home repairs, cutting retirement contributions, or deferring healthcare spending.

The Application Process Itself Is a Barrier

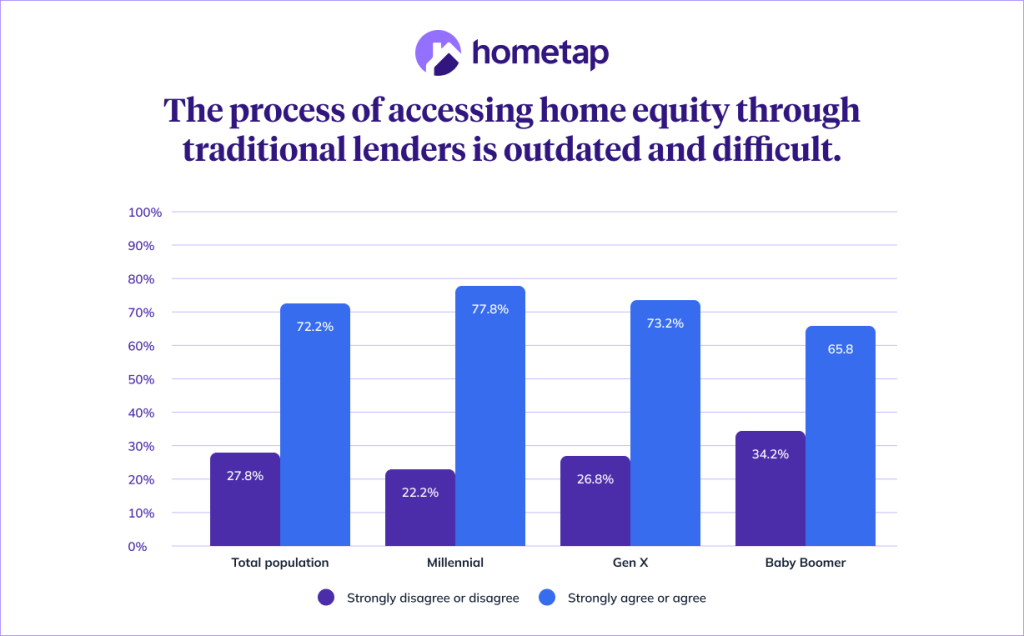

Beyond product terms, homeowners also take issue with the process of accessing home equity. Roughly 78% of millennial respondents, 73% of Generation X respondents, and 66% of baby boomers agreed or strongly agreed that the process of accessing equity through traditional lenders is outdated and difficult. Separately, 17% flagged excessive paperwork and 16% cited a lack of clear understanding of costs and terms as factors that make traditional products unattractive.

This friction appears to be suppressing home equity access. The June 2025 survey found that only 6.2% of financially stressed homeowners had explored it as a financing option in the prior year.

No New Monthly Payment: A Near-Universal Wish

Perhaps the sharpest signal in the data involves monthly payment obligations. Across all respondents, 80% of millennials, 82% of Generation X respondents, and 70% of baby boomers said they wish there were more flexible ways to tap home equity without taking on new monthly payments.

That preference reflects the budget pressures documented in the earlier survey: 43.2% of respondents said they are spending a higher share of income on housing than ever before, 49.4% have already cut nonessential spending, and 38.7% have delayed home repairs or maintenance. In that environment, adding a new monthly obligation feels untenable for many.

Three in four respondents (74.5%) said today’s homeowners need new types of financing options beyond the traditional mortgage, HELOC, or home equity loan.

Younger Homeowners Are the Most Dissatisfied — But the Gap Is Generational, Not Universal

While younger homeowners register the most dissatisfaction with traditional equity products, the survey finds the disconnect is not confined to any single demographic. Older homeowners report that traditional products don’t fit their stage of life; younger homeowners say those products don’t fit their financial realities. Both groups arrive at the same conclusion: The current system works for fewer and fewer people.

When asked what they would do if traditional products failed to meet their needs in the future, the most common response across all generations was to seek out alternative financial solutions.

Methodology: The survey was conducted by AYTM on behalf of Hometap from October 23-24, 2025, among 1,000 U.S. homeowners representing a mix of ages, demographics, and regions. Respondents were recruited through AYTM’s online panel and screened to confirm current homeownership. The 12-question survey was administered online with randomized multiple-choice options; “Not applicable” and “Other” responses were available for all questions. Results reflect a 95% confidence level with a margin of error of plus or minus 3%. Generations were defined as follows: millennials, ages 25-44; Generation X, ages 45-64; baby boomers, ages 64-79.

This story was produced by Hometap and reviewed and distributed by Stacker.