What is an automated valuation model home appraisal?

Whether you’re considering refinancing, taking out a home equity loan, or curious what your home may be worth, waiting weeks for an appraisal can feel painfully slow. That’s where automated valuation models (AVMs) come in.

An AVM is an algorithm that estimates a property’s value by analyzing large datasets, including comparable sales, property characteristics, tax assessments, and neighborhood trends, to generate a near-instance value estimate.

In this article, Splitero breaks down exactly what AVMs are in the context of real estate, how they work, and when and why they’re used. Additionally, the story will outline what to expect if you’re working with a firm that uses them to estimate your home’s value.

Key Takeaways

- AVMs use algorithms and large data sets to estimate home values in seconds, often with a confidence score.

- There are two types of AVMs: free consumer tools and professional models used by lenders and investors.

- AVMs are much faster and cheaper than appraisals, so they’re widely used for initial valuations, portfolio risk monitoring, and homeowner value tracking, but they struggle with unique homes, recent renovations, and areas with few comparable sales.

- AVMs are a starting point, not a replacement; legal matters, government-backed loans, and complex or recently renovated properties typically still require a hybrid or full traditional appraisal.

What are automated valuation models and how do they work?

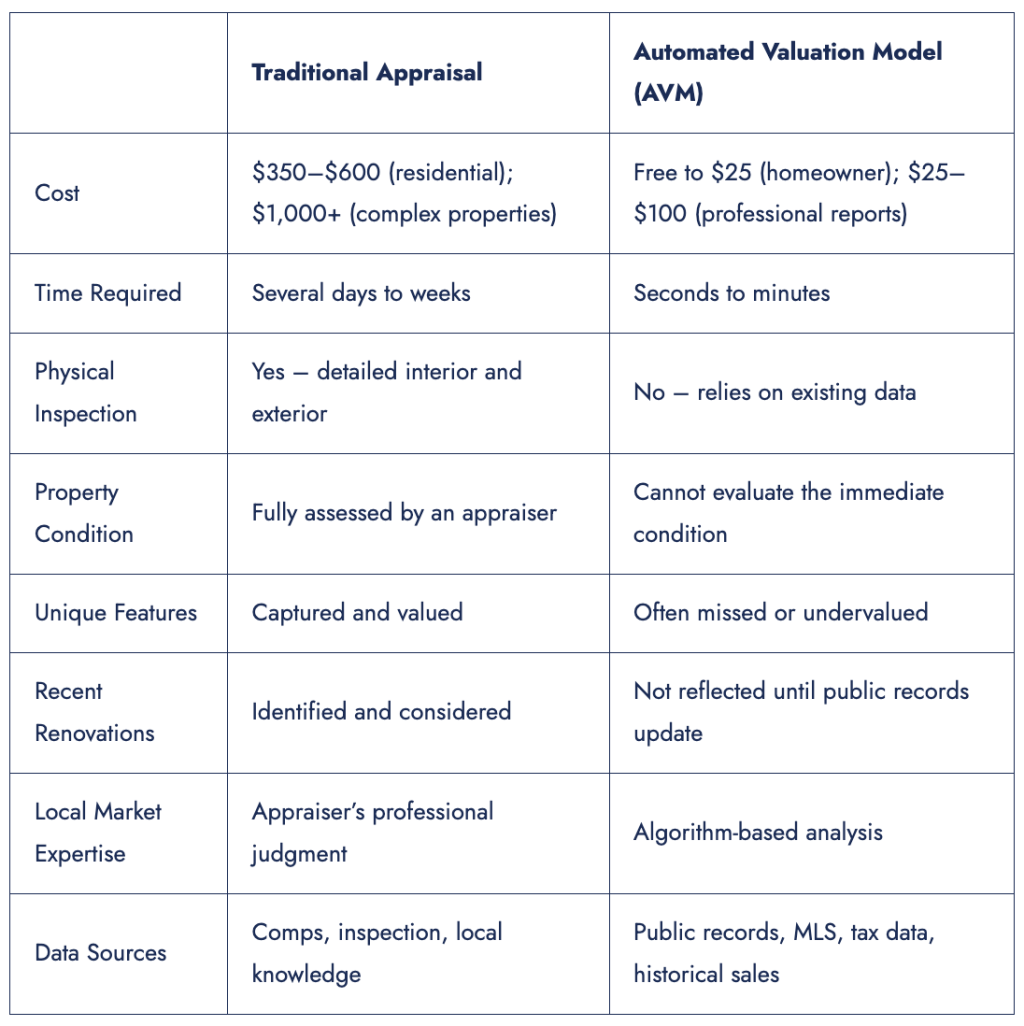

Automated valuation models in real estate are sophisticated computer algorithms that estimate property values using mathematical modeling and statistical analysis. Unlike traditional appraisals that require a physical inspection, AVMs analyze vast amounts of data to generate property valuations almost instantaneously. These systems pull data from multiple sources, including public records, multiple listing services (MLS), tax assessments, and historical transaction databases.

There are two main types of AVMs used today: consumer-facing models and professional-grade systems.

- Public-facing AVMs are the free tools commonly found on real estate websites, designed to give homeowners a quick estimate of value based on publicly available data.

- Professional-grade AVMs are designed for institutional use, enabling informed decisions in lending, investment, and portfolio management. These models are continuously benchmarked and audited across extensive datasets to verify their accuracy, stability, and transparency. Rigorous testing ensures that lenders, investors, and other financial partners understand the reliability of each model before it’s applied in real transactions.

The difference between public-facing AVM models and professional-grade AVMs can often be why you receive different valuations from an online tool compared to your lender or home equity partner.

AVMs typically employ several analytical methodologies working in concert. Hedonic modeling analyzes property characteristics, such as square footage, number of bedrooms, lot size, and age, to determine value. Repeat sales analysis tracks how the same properties have sold over time to identify price trends and patterns. Tax assessment modeling incorporates government valuation data, while comparable sales approaches mirror traditional appraisal methods by comparing your home to the sale of recent similar sales.

The algorithms weigh these various factors, adjust for market conditions and location, and generate an estimated value. Most AVMs also provide a confidence score or forecast standard deviation, indicating the reliability of the estimate based on the quality and quantity of available data. Homes in areas with abundant recent sales data generally receive more accurate valuations than those in markets with limited transaction history.

A brief history of AVMs

The concept of automated property valuation emerged in the 1980s as computing power became more accessible and those managing property databases began to digitize them. Early models were relatively simple, relying primarily on tax assessment data and basic statistical regression analysis.

The 1990s brought significant advancement as companies began aggregating comprehensive property databases and refining their algorithms. The internet revolution of the late 1990s and early 2000s accelerated AVM development, making vast amounts of real estate data available for analysis.

The 2008 financial crisis marked a turning point for AVMs. Regulators and lenders sought more efficient ways to value properties and assess portfolio risk, driving increased adoption and acceptance of AVMs. Companies like Zillow popularized consumer-facing AVMs with products like the “Zestimate,” bringing automated valuations into mainstream awareness and making property value estimates accessible to anyone with internet access.

In 2024, the Mortgage Bankers Association reported that over 75% of home equity loans and HELOC originations in 2023 used AVMs or desktop valuations in some part of the process. The combination of speed, low cost, and accuracy has made AVMs an essential first step in most valuation workflows.

A major regulatory milestone arrived in June 2024, when the Consumer Financial Protection Bureau (CFPB), along with other federal agencies, issued a rule establishing nationwide standards for governance, accuracy, and bias prevention. The rule took effect on Oct. 1, 2025, and requires lenders to maintain quality-control systems to prevent valuation bias.

AVMs vs traditional appraisals: What’s the difference?

The biggest differences between AVMs and traditional appraisals are cost and turnaround time.

According to Angi, appraisals cost an average of $350 to $600 and can take anywhere from a few days to a few weeks, depending on the home. In contrast, AVMs generate results in seconds, typically costing $25 to $100 for professional-grade use or free for public-facing tools.

Traditional appraisals and AVMs also vary in applicability. AVMs are helpful for an initial valuation of any home. However, you may want to consider obtaining a traditional appraisal if your home has unique characteristics that aren’t reflected in public records or if you’ve recently undergone a renovation.

When and why AVMs are used

Automated valuation models are used in varying circumstances depending on who is using them and what their goals are.

- Lenders use AVMs extensively for portfolio risk management, monitoring loan-to-value ratios across thousands of properties without the expense of repeated appraisals. They also employ AVMs for preliminary screening of refinance applications, determining which loans warrant full appraisals, and for evaluating collateral risk on existing mortgage portfolios.

- Real estate professionals rely on AVMs for quick property valuations when counseling clients, preparing comparative market analyses, identifying potential listings in target neighborhoods, and screening investment opportunities before committing to deeper analysis.

- Homeowners increasingly use AVMs to monitor their property’s estimated value between sales transactions, inform decisions about refinancing or home equity lines of credit, and get ballpark figures before deciding to list their property for sale.

- Investors utilize AVMs to screen potential acquisitions quickly across multiple markets, value large portfolios efficiently for performance tracking, and conduct preliminary due diligence before ordering full appraisals on promising properties.

- Tax assessors often employ AVMs to supplement mass appraisal processes, helping ensure property tax assessments remain current and equitable across thousands of properties in their jurisdictions.

When traditional appraisals are required

Despite their utility, AVMs cannot replace traditional appraisals in several critical situations.

Most mortgage lenders require traditional appraisals for purchase transactions, particularly those involving government-backed loans, such as FHA or VA mortgages. According to the U.S. Department of Housing and Urban Development’s guidance, a traditional appraisal is required for most federally related mortgage transactions. Legal matters such as estate settlements, divorce proceedings, or property disputes may also require formal appraisals for court acceptance.

AVMs also fall short for properties with unique characteristics, significant recent renovations not yet reflected in public records, or those located in markets with sparse comparable sales data. Suppose you know you recently did renovations on your home or made significant improvements. In that case, it’s a good idea to ask for a hybrid or traditional appraisal in addition to an AVM.

In rapidly changing markets or for properties that deviate significantly from neighborhood norms, a lender or firm may order a hybrid appraisal or a full traditional appraisal to supplement an AVM’s valuation.

The bottom line

Automated valuation models have transformed real estate by making property valuations faster, cheaper, and more accessible than ever before. While they cannot fully replace the nuanced judgment of licensed appraisers, AVMs serve as powerful tools for preliminary assessments, portfolio management, and market analysis.

For straightforward properties and quick estimates, AVMs shine. For unique homes or detailed valuations, traditional or hybrid appraisals remain essential.

Either way, the evolution of AVMs means homeowners, lenders, and buyers now have more transparency and control than ever before in understanding what a home is truly worth.

Frequently Asked Questions

What is an AVM in real estate?

An automated valuation model is a technology-driven system that estimates a property’s market value using data and statistical modeling, rather than a physical inspection. AVMs analyze sales history, tax records, and market trends to predict a home’s current worth.

How do AVMs pick comparable sales?

AVMs evaluate thousands of comparable sales (“comps”) to find properties most similar to the subject home. Using statistical techniques like hedonic regression and modern machine learning algorithms, they weigh features such as size, age, location, and sale timing to determine which comps carry the most predictive value. This approach lets the model assign more influence to comps that truly reflect market conditions while filtering out irrelevant data.

Are AVMs accurate?

AVMs can be highly accurate, especially in areas with abundant and reliable sales data. Their performance depends on data quality, model design, and how well the algorithm accounts for local market trends. While they can’t account for interior conditions or unique features like recent renovations, their accuracy has improved significantly thanks to expanded datasets and machine-learning advancements.

What’s the difference in cost between AVMs and full appraisals?

Most homeowner-facing AVMs are free, while lender-grade AVMs typically cost between $25 and $100 per valuation. In contrast, a full appraisal by a licensed professional usually costs $300-$600, depending on property type and market. That pricing gap is one reason lenders and investors increasingly use AVMs for initial valuations — they deliver speed and affordability while maintaining oversight through required model validation.

This story was produced by Splitero and reviewed and distributed by Stacker.