Women are increasingly homeowners, but can experience home insurance coverage gaps

With March being Women’s History Month, it’s a fitting time to celebrate the remarkable achievements women around the world make every day. But it’s also an ideal time for women to think about the future and the best ways to safeguard it, especially if you are single, divorced or the head of your household.

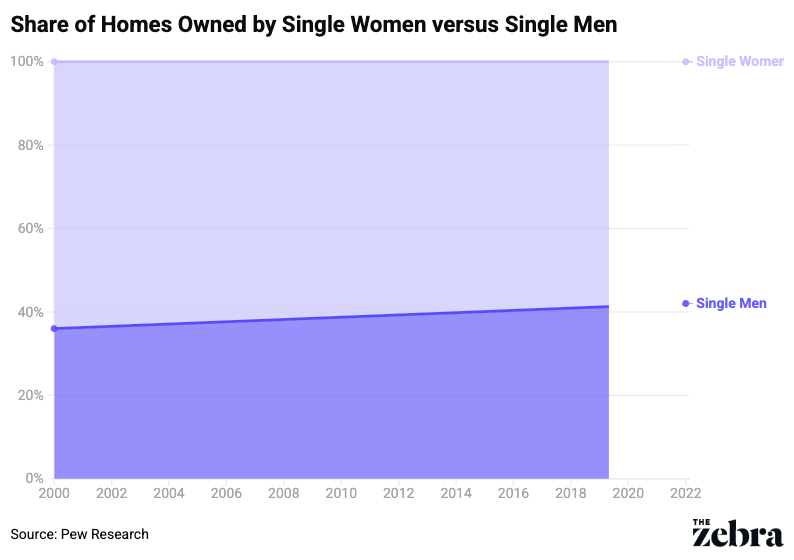

After all, more women today are homeowners, renters, and insurance policyholders than ever before. In fact, single women own 58% of the 35.2 million homes owned by unmarried Americans.

Auto insurance coverage gets plenty of attention, but often home and renters insurance isn’t as closely scrutinized, which can lead to coverage gaps that many may not be aware of. TheZebra provides a closer look at these protection shortfalls, policy language that should be carefully reviewed and life transitions that should prompt an insurance checkup.

More Women Are Becoming Homeowners And Primary Policyholders

Women are increasingly taking the reins of wealth management, with over two-thirds of female consumers surveyed reporting they hold primary responsibility for their household's financial investment decisions, according to 2025 data from the CFP Board. The share of single women purchasing homes has nearly doubled in the past four decades, representing 20% of all home purchasers versus 8% for single men, per the National Association of Realtors.

“What that really means is that more women are not just homeowners, but the sole mortgage holders and the primary decision-makers on their insurance policies,” explains Beth Swanson, insurance analyst for The Zebra. “They’re choosing the coverage limits, reviewing deductibles and making long-term protection decisions independently.”

As financial autonomy increases, so does responsibility for property protection, liability management and asset preservation, which is why ensuring you have the right coverage is crucial.

“Insurance planning is an extension of financial independence for women,” says Dennis Shirshikov, a professor of finance and economics at City University of New York/Queens College. “Ensuring you have the right protection is not about fear; it’s about preserving the progress that you’ve already achieved.”

Common Home Insurance Gaps

People of all genders experience coverage gaps in their home insurance; however, these gaps in coverage can be particularly important for women to be aware of. After all, due to a disparity in earnings, more frequent career interruptions, and longer life expectancies, women tend to have lower financial security than men and 30% less saved for retirement. Thus, for women, protecting their home, which is often their biggest financial asset, can be especially important.

Don’t just assume that current coverage is adequate. The truth is, there may be gaps and blind spots that leave a homeowner vulnerable, which is why they should review their policy closely.

“Underinsurance is a common problem. You need to check with your insurance agent to make sure you have the right types of coverage and enough insurance to rebuild your home and replace your belongings if necessary,” recommends Janet Ruiz, director of Strategic Communication for the Insurance Information Institute.

Indeed, many homeowners often insure a property based on purchase price instead of the cost to rebuild, which can lead to shortfalls after a loss.

“Remember that construction expenses can change, and many people underestimate how much it would cost today to rebuild their house. Yet, going with the market value isn't the answer either, since that takes into account factors beyond the physical structure, like school districts or views,” adds Swanson.

Having adequate liability protection, which provides coverage if someone is injured on your property or sues you for damage, is also important, especially as your assets grow.

Additionally, if you’ve separated or divorced recently, it’s easy to overlook your insurance policy, which doesn’t automatically get updated. Remember that even if your mortgage is refinanced or the deed changes, your policy may still list both former partners. But if you need to file a claim, that can create delays or confusion around how funds are issued.

“Another gap is insufficient personal property coverage, especially for valuable items like jewelry, business equipment used for remote work or specialty collections,” Shirshikov notes.

Ruiz recommends considering a personal liability umbrella policy, as well, to cover all your assets. This provides an extra cushion of coverage for major claims and lawsuits that exceed the limits of your primary insurance policies.

When Renters Insurance Is Still Necessary

If you rent instead of own, ask yourself: If you had to replace everything you possess at today’s prices, could you comfortably afford it?

“Furniture, clothing, electronics, kitchen items, work equipment and personal belongings add up quickly,” Swanson notes “A lot of renters assume major losses are rare or that their landlord’s insurance covers their belongings. It doesn’t.”

That’s why having renters insurance is wise. It safeguards personal property, provides liability protection and handles additional living expenses if your rental becomes uninhabitable. But be sure to choose coverage limits that reflect the full replacement value of your personal items, not their depreciated value. And liability limits should be high enough to preserve your savings and future earnings.

Life Changes That Should Trigger A Home Insurance Review

Another key time to revisit your policy is whenever your household, legal or financial picture evolves.

- Marriage, divorce and other legal considerations: “Marriage, divorce, a name change or retitling your home into or out of a living trust should trigger a check that the named insured and additional insureds match the deed in trust,” advises Jay Yu, an estate planning attorney. “Also, major renovations, adding a new roof or solar, finishing a basement, or building an accessory dwelling unit (ADU) can require higher dwelling limits and new endorsements.”

- Add household members: Your liability needs can also change if you add a child, live-in caregiver, or dog to your household, start a side business, take in a tenant or short-term guests, or acquire significant art or jewelry, Yu continues.

- Moving or refinancing: “Relocating to a new state or refinancing your mortgage can affect coverage requirements, too,” says Shirshikov.

How Home And Auto Insurance Fit Together

The good news is that you may be able to save money on your homeowners or renters insurance if you bundle coverage with your auto insurance using the same carrier—a strategy that can result in discounts and simplify billing and renewals.

“However, bundling isn’t automatically your best financial decision. Compare bundled quotes against separate quotes to see what truly offers the best combination of price and coverage,” Swanson suggests. “The key is making sure both policies reflect your current life circumstances, including who lives in the household and who is listed as a driver or named insured.”

Protecting Independence And Long-Term Stability

Keeping your home fully protected by insurance is important for everyone. But it can be especially important for women.

Make sure your coverage is up to snuff, not piecemeal. Work with your insurance agent to thoroughly review your policies and coverage limits at renewal time or whenever you experience a significant life change.

This story was produced by TheZebra and reviewed and distributed by Stacker.