Roth IRA vs. traditional IRA: Which is right for you?

Individual retirement accounts, or IRAs, can be an important part of your financial strategy when preparing for retirement. The most common types of IRAs are traditional and Roth.

How do they differ, and which one is right for you? Below, Ally Financial walks through both choices, so you can make the best decision for your financial future.

What is a traditional IRA?

A traditional IRA is an investment account in which your taxes are deferred until withdrawal.

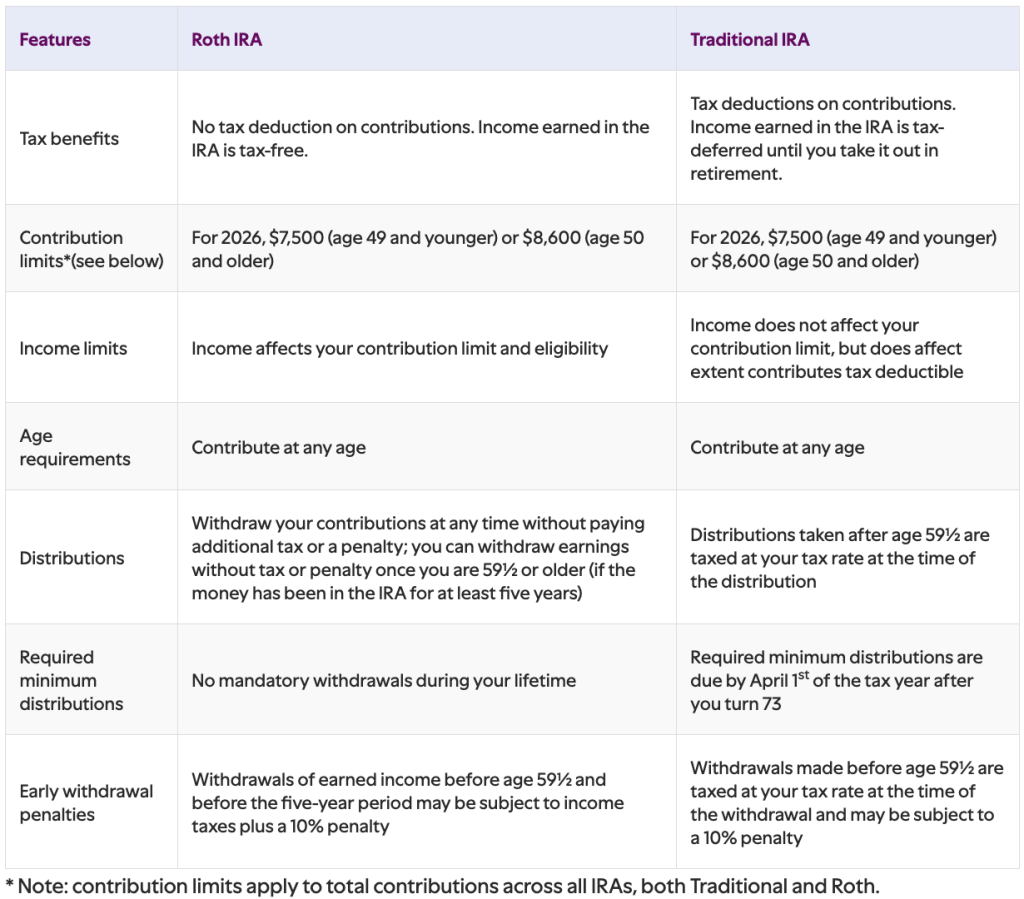

Key features of traditional IRAs

- Tax-deductible contributions: The amount of your contributions that can be deducted from your taxes depends on your income, tax filing status, and age.

- Tax-deferred growth: Once money is in a traditional IRA, you won’t pay taxes on dividends or capital gains until you withdraw the money.

- Required minimum distributions (RMDs): You must take the RMDs by April 1 of the year after you turn 73. If you don’t take the RMD, you’ll pay the original taxes owed, plus a 25% excise tax (or 10%, if you correct the error within two years).

Benefits of traditional IRAs

- Immediate tax benefits: You’ll receive a perk on your taxes every year when paying into a traditional IRA because your contributions are tax deductible.

- Potentially lower taxable income: Contributions to a traditional IRA during your working years reduce your taxable income, and could even move you into a lower tax bracket.

What is a Roth IRA?

With a Roth IRA, your contributions are taxed immediately, and no tax is owed when eligible money is withdrawn.

Key features of Roth IRAs

- Contributions made with after-tax dollars: You pay taxes upfront when contributing to a Roth IRA.

- Tax-free growth and withdrawals: You don’t pay taxes when you withdraw the money, as long as you are 59 1/2 and have held your Roth IRA for at least five years.

- No RMDs during the account holder's lifetime: Withdrawals from Roth IRAs are not required until after the death of the account owner. (Beneficiaries are subject to separate RMD rules.)

Benefits of Roth IRAs

- Tax-free income in retirement: Once you’re of retirement age, your eligible withdrawals will be tax-free.

- No mandatory withdrawals: Roth IRAs offer more flexibility because there are no rules determining when and how much you must withdraw.

Comparing traditional and Roth IRAs

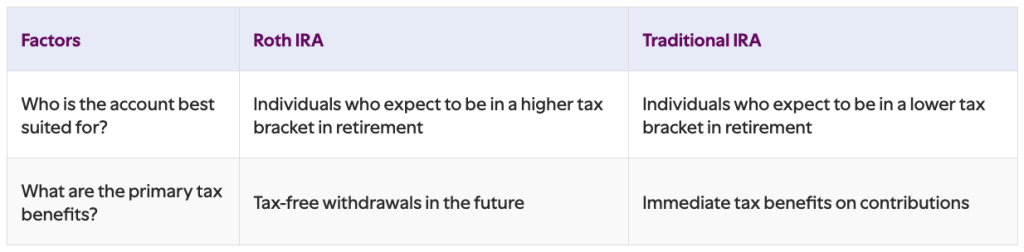

Making the right choice for you

Consider these factors when choosing which retirement account works best for you:

- Tax rate: If your current tax rate is higher than your expected tax rate in retirement, you may save more in taxes over time with a traditional IRA. But if you expect your tax rate to increase in retirement, a Roth IRA allows any potential earnings on your contributions to grow tax free.

- Retirement timeline and income needs: A traditional IRA might align better with a shorter timeline because you get a tax deduction on your contributions right away, but pay taxes later on your withdrawals. With a Roth IRA, you could potentially benefit from years of tax-free growth if your timeline to retirement is longer.

- Estate planning goals: When beneficiaries inherit a traditional IRA, they must pay income taxes on the distributions they take. On the other hand, Roth IRAs can be passed on tax free to beneficiaries as long as certain requirements are met (like the five-year rule).

- Income: If your modified adjusted gross income (MAGI) goes over a certain level, you might not be able to invest in a Roth IRA.

Invest in your future

Once you have an understanding of the differences between a Roth and traditional IRA, consider speaking with a financial advisor to explore which IRA solution aligns best with your long-term financial strategy. Your advisor can help you find the path toward retirement depending on your situation, life expenses and future goals.

This story was produced by Ally Financial and reviewed and distributed by Stacker.