2 in 3 small business owners lose sleep over their finances

Running a small business is one of the most demanding things a person can do. The financial pressure rarely lets up, and for millions of owners across the U.S., it doesn't stay at work. It follows them home and keeps them up at night.

To better understand the pressures of self-employment, Bluevine surveyed over 750 U.S. small business owners about how financial stress affects their sleep, mental health, business decisions, and day-to-day operations. The findings are sobering: 68% of owners lose at least one full night of sleep per month due to financial worries.

In the study below, Bluevine breaks down which financial pressures are driving small business owner burnout, how stress is holding businesses back from growing, and what owners say would actually make a difference.

Key takeaways

- 71% of small business owners report moderate, high, or extremely high financial stress.

- 68% have delayed or avoided a major business decision—such as hiring or expanding—due to financial stress in the past 12 months.

- 62% of SMB owners have reduced or skipped their own pay at least once in the past year to cover business expenses.

- 41% of owners say their biggest source of financial anxiety is the gap between money coming in and bills coming due—ranking above payroll, taxes, and debt.

Financial stress is taking a physical toll on small business owners

More than two-thirds (68%) of small business owners lose at least one full night of sleep per month due to financial worry or cash flow concerns, and for 12% of owners, that means six or more lost nights every single month.

Poor sleep is part of a broader picture. Nearly three-quarters (71%) of owners report moderate to extremely high financial stress and 53% say that stress has left them feeling emotionally drained or burned out in the past year.

Running a small business has always been a difficult job. But today, many owners are trying to keep their operations running against a backdrop of high inflation, new tariffs, and shifting consumer behavior—all forces that are largely outside their control.

Financial stress is stalling business growth

In the past year, 68% of small business owners delayed or avoided a major business decision, such as hiring, purchasing equipment, or expanding, because of financial stress. For some, it only happened once. For others, it's a pattern: 9% say they delayed major decisions repeatedly or on a regular basis.

That hesitation makes more sense when you consider how little breathing room many owners actually have. Recent Bluevine research found that nearly 39% small businesses have less than one month of operating expenses in reserve. As an entrepreneur, you never want to be timid, but when the financial buffer is that thin, pulling back on big decisions is a form of self-preservation.

The consequences reach further than any individual business. Small businesses account for 44% of the U.S. GDP and employ 62.3 million people. When owners delay decisions because of stress, it slows hiring, suppresses local investment, and squeezes other businesses that depend on small business spending. A restaurant that pulls back on ordering local produce becomes one fewer customer for neighboring farmers.

According to the Federal Reserve, small business owners' expectations for future revenue and employment growth declined year-over-year, citing rising input costs and challenges reaching new customers as key contributing factors.

It's not that owners don't want to take risks. It's that the financial pressure makes those risks feel too big to take. And yet, Bluevine’s 2026 BOSS Report found that 78% of small business owners remain optimistic about their profitability outlook for the year ahead, which suggests they're able to grow their business, even though current conditions make it difficult.

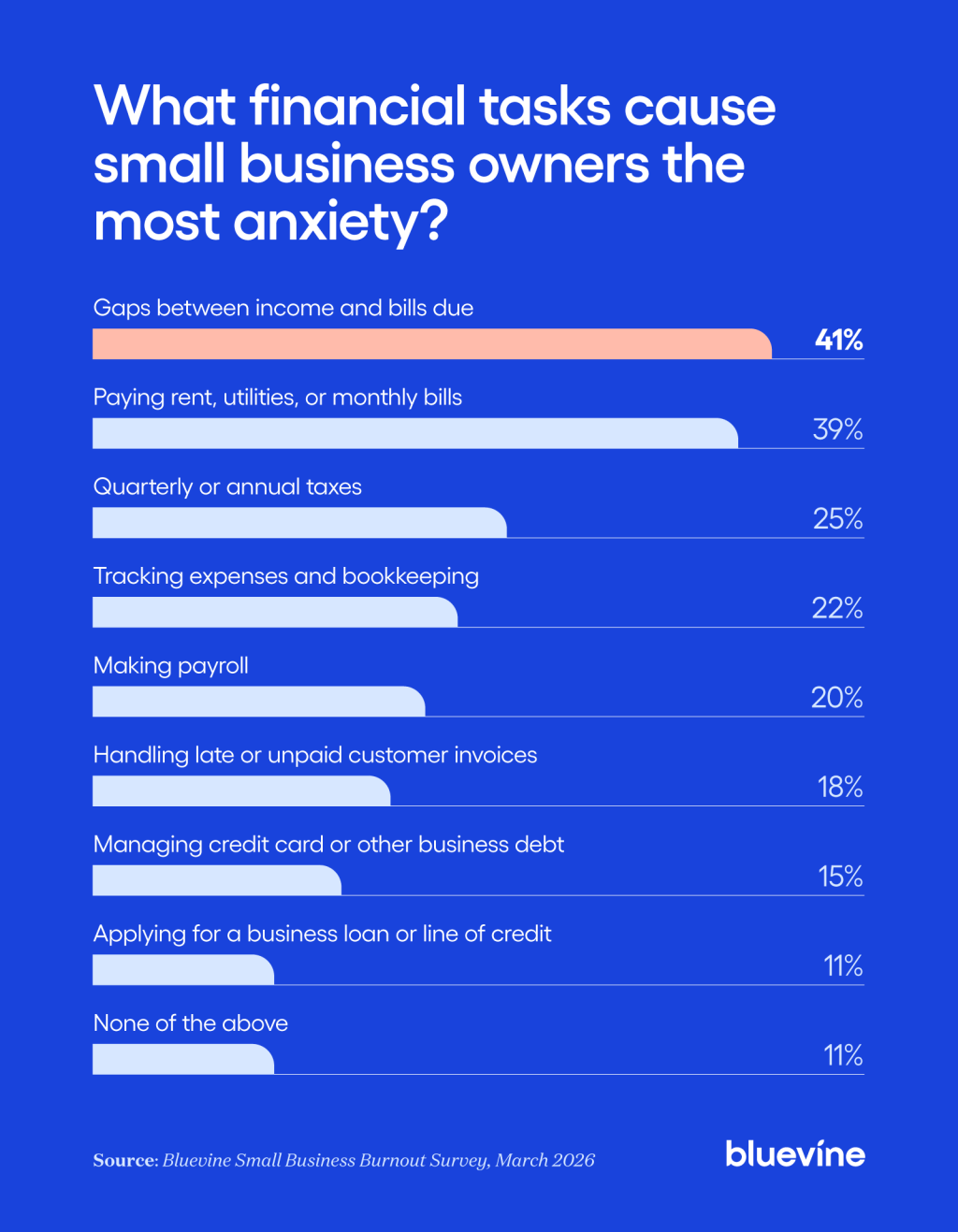

Cash flow timing—not payroll—is owners' biggest source of financial anxiety

The biggest source of financial anxiety for small business owners isn't debt, taxes, or even making payroll. It's timing. Around 2 in 5 (41%) owners say their top stressor is bringing in money in time to pay the bills, outranking other stressors like:

- Paying monthly bills and utilities (39%)

- Quarterly or annual taxes (25%)

- Tracking expenses and bookkeeping (22%)

- Making payroll (20%)

Notably, payroll—which is typically a major expense for a small business owner—ranked fifth among anxiety triggers. Owners who dedicate a separate payroll bank account or sub-account to those funds can have the peace of mind that payroll is accounted for, even if they're struggling to pay the rest of their bills.

Overall uncertainty makes proactive planning nearly impossible and forces owners to be reactive.

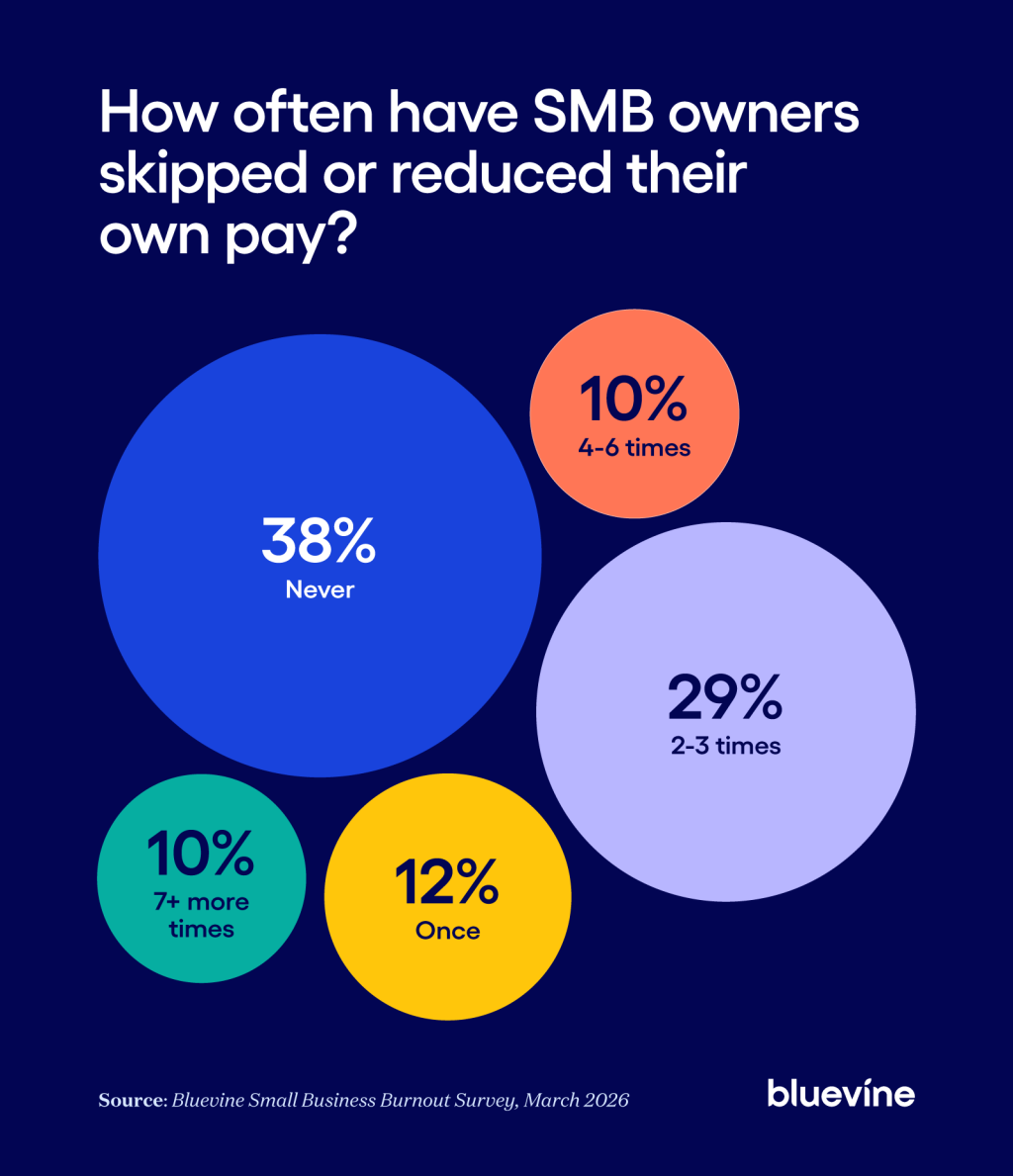

Owners are paying business expenses out of their own pockets

Nearly two-thirds (62%) of small business owners have reduced or skipped their own pay at least once in the past year to cover business costs. For 20%, it happened four or more times over the last 12 months.

Late payments are widespread. Bluevine's research on late customer payments shows 3 in 5 small businesses experience them at least occasionally, and owners are often the ones who absorb the hit.

When customers pay late, owners frequently cover the difference themselves rather than miss a bill or fall behind on obligations. Our research also revealed that nearly 1 in 3 have delayed paying themselves as a direct result—which helps explain why skipping or reducing personal pay has become such a common and recurring issue.

Many people start a business in pursuit of financial freedom, not to take on new personal financial burdens. But when the business needs cash, the owner's paycheck is often the first thing to go.

That creates a compounding problem. It's hard to make clear-headed business decisions when you're also managing personal financial stress, and for many owners, the line between business finances and personal finances is functionally nonexistent.

For owners trying to protect their personal finances, exploring financing options like a business line of credit or term loan is a good first step. These tend to offer more flexibility and lower costs than alternatives like small business factoring, which converts unpaid invoices into immediate cash but works best as a true last resort.

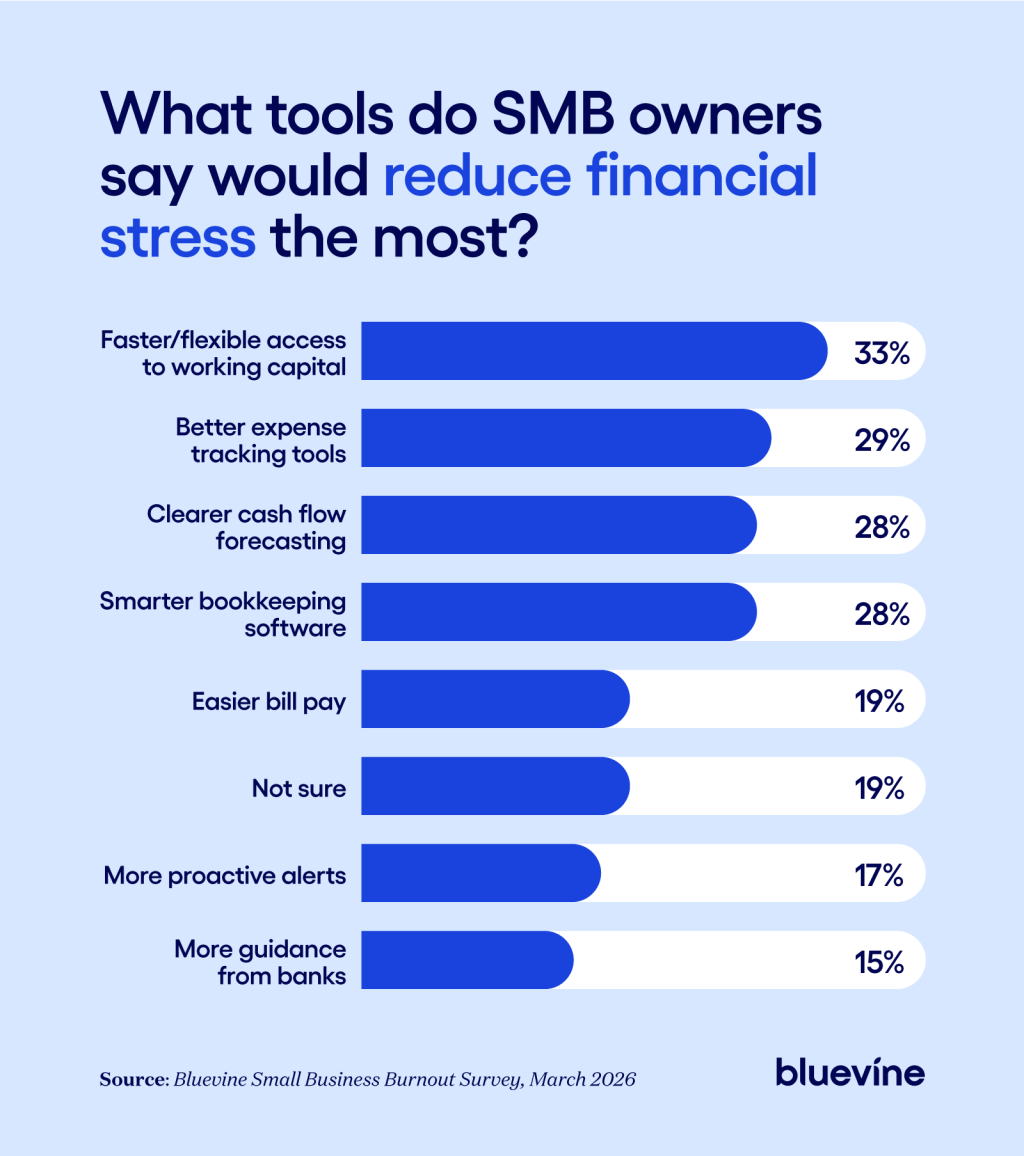

Owners need better tools, not just better habits

When asked what would actually help reduce financial stress, owners pointed to practical solutions for their biggest pain points. One-third (33%) want faster or more flexible access to working capital, 29% want better expense tracking tools, and 28% want clearer cash flow forecasting or smarter bookkeeping software.

The data also reveals something worth recognizing. Most owners aren't shutting down when financial stress hits. Only 12% say they avoid looking at their accounts when things get tough, and 31% actively review their cash flow and budget in detail. That's a group of people doing their best to stay on top of a genuinely difficult situation.

Many small business owners are financially literate but the tools available to them aren't keeping up. More than half (51%) of owners say their current banking setup either makes no difference to their stress or actively adds to it, which means the platforms many owners rely on every day aren't always solving the problems they were built to solve.

Your business finances shouldn't cost you sleep

The picture that emerges from this data is one of owners who are working hard, paying close attention, and still losing sleep, in part because the tools available to owners have not kept up with the financial complexity of running a small business. The stress is real, the personal sacrifices are significant, and the drag on business growth is measurable.

Better tools won't solve everything, but they can take a real weight off. When owners have clearer visibility into their cash flow and aren't drowning in financial admin, they make better decisions and sleep better at night. For owners who need faster access to capital, exploring lines of credit and term loans built for small businesses is a good place to start.

Methodology

The survey was conducted by Centiment for Bluevine. The survey was fielded between February 27, 2026, and March 9, 2026. The results are based on 781 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and own a small business. Data is unweighted, and the margin of error is approximately +/-3% for the overall sample with a 95% confidence level.

This story was produced by Bluevine and reviewed and distributed by Stacker.