How to pay an invoice: Types of payment methods with examples

Paying invoices sounds simple enough. A vendor creates an invoice and sends a bill, your team approves it, and the money goes out. In practice, though, invoice payments are where a lot of finance teams lose time they didn’t realize they were spending. Between matching purchase orders, chasing approvals, and figuring out whether to send a wire or schedule an ACH, what should take minutes can stretch into days. And when you multiply that by dozens or hundreds of invoices per month, the inefficiency compounds fast.

The payment method you choose for each invoice matters more than most teams give it credit for. Sending a wire transfer for a $500 software subscription doesn’’t make sense when ACH costs a fraction of the fee. Paying a $75,000 international supplier by check isn’t just slow, it introduces unnecessary risk. Yet many finance teams default to the same one or two methods for everything because nobody has taken the time to match the method to the situation. That’s money and time left on the table every single month.

This article from finance technology company Brex is built for finance professionals who want to stop treating invoice payments as an afterthought. It walks through what invoice payments actually involve, how the process works step by step, the most common payment methods and when each one makes the most sense, and how automation can take your AP workflow from a manual grind to something that practically runs itself. Whether you’re processing 50 invoices a month or 5,000, the goal is the same. Pay the right amount, to the right vendor, using the right method, on time, and without burning hours of your team’s week to make it happen.

The basics of invoice payments

An invoice payment is the transfer of funds from a buyer to a seller to settle an outstanding bill for goods or services. It’s the final step in the accounts payable cycle, following invoice receipt, verification, and approval. While that sounds straightforward, the way your team handles this step has a direct impact on vendor relationships, corporate cash management, and how much time your finance team spends on manual work each week.

What makes invoice payments different from other types of transactions is the process around them. You’re not swiping a card at a register. These payments happen after goods or services have already been delivered, which means there’s a verification step, an approval step, and a reconciliation step built in. Each payment creates documentation that feeds into financial reporting, tax filings, and audit trails. For most B2B companies, invoice payments are the primary way money moves out the door, so getting the process right isn’t optional.

How to make an invoice payment in 5 steps

The invoice payment process follows a predictable path from invoice to reconciliation. Understanding each step helps finance teams spot where delays happen and where automation can save the most time.

Step 1: Capture invoice data

When an invoice arrives by email, vendor portal, or mail, the first job is logging the key details into your accounting software. That includes vendor name, invoice number, line items, total amount, and payment terms. This step is where a lot of errors start. Manual data entry is slow and prone to mistakes, especially when your team is processing high volumes. Getting the data right here saves you from chasing problems downstream.

Step 2: Verify the invoice and match against the purchase order

Perform invoice matching by comparing the invoice against the original purchase order and delivery receipt. This two-way or three-way matching is a key part of invoice reconciliation in catching pricing errors, duplicate invoices, and discrepancies before payment goes out.

Step 3: Route for approval

Send the invoice to the right approver based on amount, department, or vendor. Following accounts payable best practices, many companies set threshold rules. For example, invoices under $5,000 get department-head approval, while anything above routes to a finance manager. The key is making sure every invoice has a clear path to approval so nothing sits in someone’s inbox waiting for attention.

Step 4: Schedule to send payment

Once the invoice is approved, schedule the payment based on the agreed terms. Select the payment method, whether ACH, wire, card, or check, and initiate the transfer. Timing matters here. If timing is critical, same-day ACH can compress that window further, though cutoff times and eligibility vary by bank.

Step 5: Reconcile the payment

After payment clears, match the transaction to the original invoice in your accounting software. Mark the invoice as paid, update the accounts payable balance, and archive the record for audit and compliance purposes.

The entire cycle can take anywhere from a few days to several weeks depending on how much of the process is manual. If you’re processing hundreds of invoices per month, you need a clear system for keeping track of invoices and payments as approval bottlenecks and manual data entry are the biggest sources of delay.

A real-world invoice payment process walkthrough

Say a software company receives a $15,000 invoice from a cloud infrastructure vendor on March 1. The invoice specifies Net 30 payment terms, which means payment is due by March 31. The accounts payable team pulls up the original purchase order to verify the charges match what was agreed on, confirms the services were actually delivered, and routes the invoice to the engineering director for approval.

Once approved, the AP team schedules an ACH payment for March 28, giving a few days of buffer before the due date while also accounting for the one to three business days ACH transfers typically take to settle. The payment clears on March 30, both sides mark the invoice as paid, and the transaction is recorded in the general ledger.

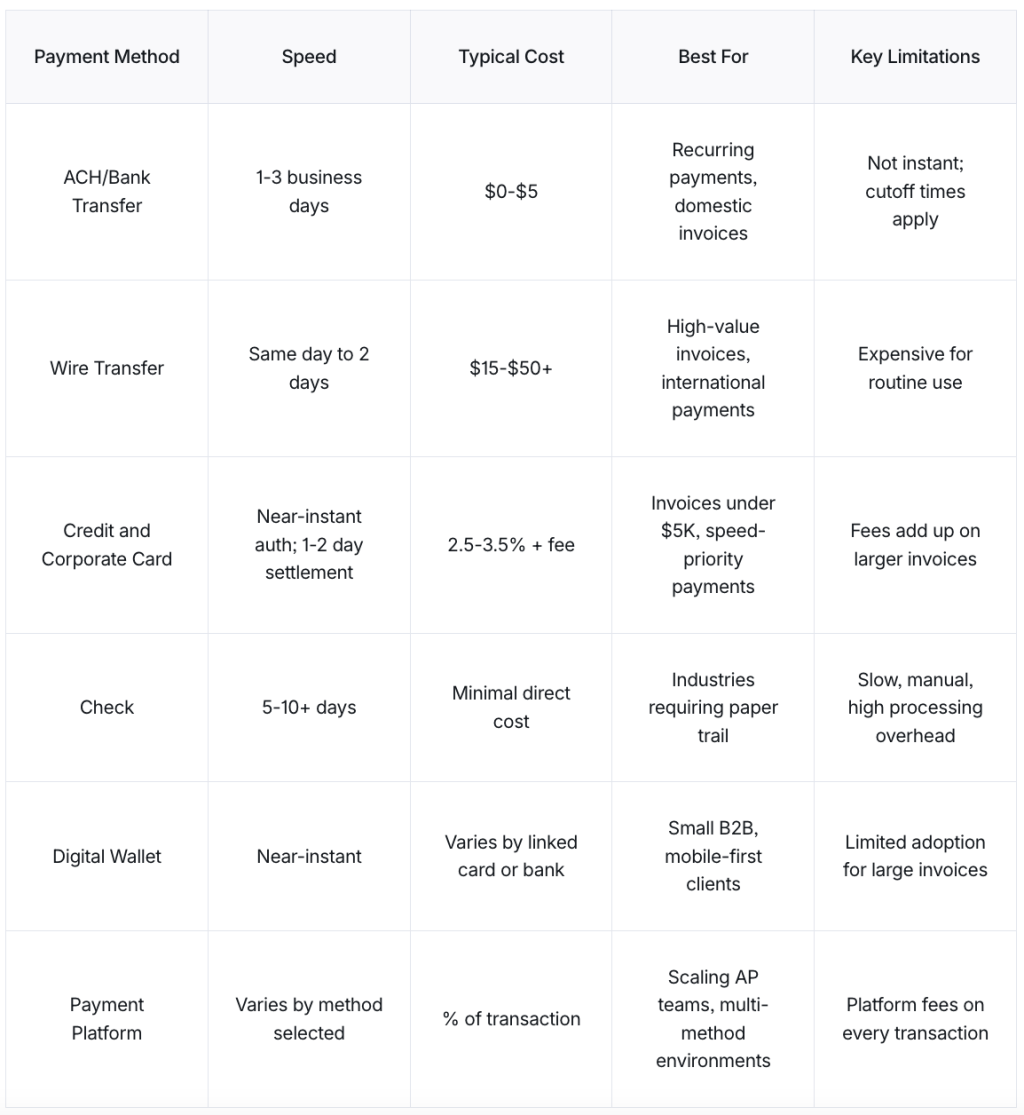

Comparing common invoice payment methods

Not every payment method fits every situation. Every invoice is different. The amount, how quickly you need to move funds, where your vendor is located, and what your AP workflow can support all shape which method makes sense.

Here’s how the most common invoice payment methods stack up.

ACH transfers

Automated Clearing House (ACH) transfers move funds directly between bank accounts through the US banking network. SEPA serves a similar function in Europe. These are the workhorse of B2B invoice payments for a reason: they’re low-cost, easy to automate, and reliable for recurring payments.

ACH transfers work best for domestic invoices, recurring vendor payments, and transactions where keeping fees low matters more than same-day settlement. The main limitation is speed. ACH isn’t instant. How long ACH payments take to process depends on your bank's cutoff times and whether same-day settlement is available. For time-sensitive payments or international vendors, you’ll need a different method.

To see how this plays out in practice, consider a company pays a $12,000 monthly software license via ACH. The payment is scheduled to run automatically three days before the due date, arrives in one to three business days, and costs under $5 per transfer. Over the course of a year, that’s 12 payments processed with almost no manual effort and minimal fees.

Wire transfers

Wire transfers send funds through banking networks like Fedwire for domestic payments or SWIFT for international ones. They’re faster than ACH and provide guaranteed finality, meaning the payment can’t be reversed once it settles. That combination of speed and certainty makes wires the go-to method for high value invoices and cross border payments where other options aren’t available.

The tradeoff is cost. Wire fees typically range from $15 to $50 per transfer, and both the sender and recipient may get charged. That fee structure makes wires impractical for routine, smaller payments. If you’re sending wires for invoices under $5,000, you’re likely overpaying for a level of speed and security you don’t actually need.

That math becomes clear with a real scenario. A U.S. company receives a $75,000 invoice from an overseas supplier. They pay via SWIFT wire, and funds arrive within one to two business days with finality guaranteed. The $40 wire fee is a rounding error on a payment that size, but sending that same wire for an $800 invoice would be a different calculation entirely.

Business credit cards and corporate cards

Card payments offer speed and convenience. Authorization is near-instant, funds settle in one to two days, and many vendors already accept them. For companies that issue corporate cards to team members, card payments can also simplify accounts payable by letting authorized employees pay approved invoices directly.

Cards may carry chargeback risk, which some vendors factor into their pricing. For companies that issue corporate cards to team members, card payments can simplify accounts payable by letting authorized employees pay approved invoices directly. Without spend controls, you lose visibility into what’s been paid.

The fee math is worth understanding. A $5,000 invoice paid by credit card at 2.9% costs $145 in processing fees. The same payment via ACH would cost $1 to $5. For smaller invoices, the speed of card payment can outweigh the fee difference. For larger ones, the math gets harder to justify.

Checks

Checks are the slowest and most manual payment method still in regular use. They require printing, signing, mailing, and manual reconciliation on both sides. A vendor mails an $8,500 invoice. The buyer writes and mails a check back. From issuance to clearing, five to ten days pass, and that’s assuming nothing gets lost in transit.

The 2025 AFP Digital Payments Survey reports that checks account for 26% of B2B payments, down from 33% in 2022. The trend is clearly moving away from paper, but checks haven’t disappeared yet.

Some industries still default to checks, including construction, legal services, and government contracting. If your vendors require them, you’ll need to account for the longer timeline in your payment scheduling. For everyone else, moving away from checks is one of the fastest ways to reduce AP processing time.

Digital wallets

Digital wallets like Apple Pay and Google Pay add a layer of convenience on top of existing card or bank account connections. Payments complete with a tap or biometric confirmation, and tokenized security means actual card numbers aren’t transmitted.

Wallets are most useful for smaller B2B transactions where mobile accessibility matters. A freelance consultant sends a $900 invoice with a payment link. The client opens it on their phone, taps Apple Pay, confirms with Face ID, and the payment processes in seconds. They’re less common for large corporate invoices, but adoption is growing as more payment platforms integrate wallet options into their checkout flows.

Payment platforms

Payment platforms bundle multiple methods into a single interface. Instead of managing ACH, cards, and wires separately, your team and your vendors work through one system that handles method selection, processing, reconciliation, and reminders.

The main advantage is operational. Payment platforms reduce the manual work of tracking which invoice was paid by which method, automate status updates, and give finance teams real-time visibility into outstanding payables. The cost is typically a percentage of each transaction, but the time savings and reduced error rates often justify it.

For example, a growing company processes 200 invoices per month across domestic and international vendors. Instead of managing ACH through their bank, wires through a separate portal, and card payments on individual vendor sites, they route everything through one platform. Each invoice is captured, approved, paid, and reconciled in one place.

Most growing companies use ACH as their primary method for domestic vendors and wire transfers for international payments. Corporate cards for business charges are becoming increasingly popular for their speed, built-in spend controls, and rewards, making them a strong option for recurring subscriptions, mid-size invoices, and any payment where real-time visibility matters.

What to consider when choosing a payment method

Listing payment methods is easy. Knowing which ones to prioritize for your business takes more thought.

Invoice size and frequency

Match the invoice payment method to the transaction. High-volume, lower-value invoices favor ACH or cards for speed and automation. Large, one-off payments may warrant wire transfers despite the higher fees.

Fees

Transaction fees are only part of the picture. A check costs nothing to send, but it can take 15 to 20 minutes of staff time to print, mail, and reconcile. That labor cost often exceeds the processing fee on a card payment for smaller invoices. On the other end, a $5,000 invoice paid by credit card at 2.9% costs $145 in processing fees, while ACH runs $1 to $5 for the same payment.

Factor in both the direct cost and the time your team spends on each method. A slightly higher fee that eliminates manual work and gets you paid faster can be the cheaper option overall.

Vendor location

Domestic payments have more low-cost options like ACH, checks, and cards. International invoices are a different story. They often require wires or a payment platform with multi-currency support, and if you’re paying vendors in multiple countries, you’ll want a platform that handles foreign exchange (FX) conversion and local payment rails. Without one, your team ends up managing exchange rates, tracking international wire fees, and reconciling payments across currencies manually.

Team approval structure

A two-person finance team processing 50 invoices a month has different needs than a 10-person AP department handling 500. As volume grows, the manual overhead of managing multiple payment methods separately becomes unsustainable. This is where payment platforms and automation start paying for themselves.

Automation goals

Prioritize electronic methods that integrate with your accounting software. ACH and card payments are easy to automate. Checks and cash are not. The more you invest in automated invoice processing, the less time your team spends on repetitive work after approval.

Supplier preferences

The vendor needs to accept your chosen method, but this cuts both ways. If a supplier insists on wire transfers and the fees are significant, it’s reasonable to negotiate. Offering early payment in exchange for a lower-cost method is a common and fair approach. Some vendors will also agree to ACH if you can guarantee payment within a shorter window, which saves both sides money.

Scalability

Choose payment infrastructure that won’t need replacing as you grow. If your business doubled its invoice volume next year, would your current system keep up? Think about multi-currency support, the ability to onboard new vendors quickly, and whether your platform can handle higher transaction volumes without adding headcount to your AP team.

Invoice payment problems and how to prevent them

Late payments, incorrect details, and manual processes create cash-flow uncertainty and extra admin work. Each of these issues can delay invoice payments by days or weeks. Prevention is far easier than resolution.

Missing purchase order numbers

The invoice lacks the purchase order reference, so it sits in an approval queue for weeks. Without a purchase order (PO) to match against, approvers can’t verify the charge and the invoice stalls. This is especially common with new vendors who aren’t familiar with your internal processes, or in companies where PO requirements vary by department. The longer an invoice sits unmatched, the more likely it triggers late payment penalties or strains the vendor relationship.

Always request PO numbers from vendors upfront and make them a required field on every invoice. Building this into your vendor payment automation workflow ensures it’s standard from the first transaction.

Incorrect bank details

A typo in the account number causes a failed or misdirected payment. In some cases, funds sent to the wrong account are difficult or impossible to recover. This problem is more common than most AP teams realize. Even a single transposed digit can route a payment to a completely different account, and recovering those funds often involves lengthy bank investigations with no guaranteed outcome. International payments carry even more risk because they involve additional fields like SWIFT codes and IBAN numbers. Copy and paste from verified records rather than manual entry. Better yet, use a payment platform that eliminates the need for vendors to share bank details over email.

Approval bottlenecks

Invoices sit in someone’s inbox because they’re traveling, overwhelmed, or didn’t realize the approval was waiting on them. This is one of the most common reasons invoices go past due. In many organizations, a single approver going on vacation can freeze an entire batch of payments. The problem compounds when approval chains are too long or when low-value invoices require the same sign-off as high-value ones.

To avoid approval bottlenecks, implement approval workflows with auto-escalation. If an approver doesn’t act within a set number of days, the bill pay software routes the invoice to a backup approver automatically. Set tiered approval thresholds so smaller invoices move through faster, and make sure every approver has a designated backup.

Lost invoices

Paper invoices get misplaced. Email invoices get buried under other messages. Either way, the invoice never enters your AP workflow and the payment deadline passes without anyone noticing. This is particularly problematic for companies that receive invoices through multiple channels.

Reduce the likelihood of lost invoices by sending and receiving digital invoices through a centralized system with read receipts and automatic follow-ups. If an invoice hasn’t been opened or logged within a few days, the system flags it.

Duplicate payments

The same invoice gets paid twice due to manual data entry errors, usually when the invoice is entered into the system by two different people or processed through two different channels. Duplicate payments are surprisingly common in fast-growing companies where AP processes haven’t scaled with transaction volume. They tend to go undetected for weeks or months which makes recovery even more difficult.

Require invoice verification and three-way matching before scheduling any payment. Automated systems can flag duplicate invoice numbers or matching amounts from the same vendor.

Disputed amounts

The vendor’s pricing doesn’t match what was agreed upon, and the invoice gets held up while both sides sort out the discrepancy. Disputes often arise from outdated pricing, unapplied discounts, or charges for work that wasn’t included in the original scope. This can delay payment for weeks while teams go back and forth trying to locate the original agreement.

Reference contracts or quotes directly on invoices and use consistent pricing throughout the vendor relationship. When both parties can point to the same documentation, disputes resolve faster. Keep a centralized record of all vendor contracts with version tracking, and flag invoices automatically when line items deviate from contracted rates by more than a set threshold.

Payment to the wrong entity

Fraudulent invoices or compromised vendor details lead to misdirected funds. ACH fraud and Invoice fraud are increasingly common, especially when attackers impersonate existing vendors with slightly altered bank details. These schemes often target AP teams during high-volume periods when scrutiny is lower. A fraudster only needs one successful redirect to cause significant financial damage, and the funds are often unrecoverable once the transfer clears.

Prevent payments to the wrong entities by verifying any changes to vendor bank details via phone using known contacts. Never update payment information based solely on an email request, even if it appears to come from a trusted vendor. For check payments specifically, positive pay adds another layer of protection by flagging any issued check that doesn't match your authorized list before it clears. Train your AP team to recognize common red flags like urgent language, slight email address variations, and requests to change banking details right before a large payment is due.

What high-performing AP teams do differently

Faster, more accurate invoice payments don’t require a full AP overhaul. They require clear ownership, smart thresholds, and automation in the right places.

Document payment ownership with approval thresholds

Every invoice payment workflow needs clear ownership. Write down who handles each step from invoice receipt to payment execution. When roles are unclear, invoices stall because everyone assumes someone else is handling it.

Approval thresholds keep things moving. Not every invoice needs C-suite sign-off. Route low-risk invoices to department leads and escalate larger amounts to finance leadership. Pair this with standardized payment terms across vendors, ideally Net 30 or Net 15, so your team can batch payments on a regular cadence instead of chasing different due dates every week.

Automate invoice capture, routing, and scheduling

AP automation is where the real time savings come in. Optical character recognition technology (OCR) can capture vendor details, amounts, and line items automatically, eliminating manual data entry. Rules-based workflows can route invoices to the right approver and escalate if no one acts within a set timeframe. For vendors you pay regularly, scheduled payments can execute automatically once approval is complete, so monthly software licenses, office leases, and retainer agreements run without anyone clicking “send.”

Reconcile in real time

Reconciliation is where automation pays off. Integrated systems match payments to invoices as funds clear, update your accounts payable ledger, and flag discrepancies. Month-end close goes from a multi-day marathon to a quick review. And with a single dashboard showing every invoice’s status from received to paid, finance leaders get the real-time visibility they need to manage cash flow and catch problems early.

Track what matters

Track days payable outstanding (DPO), on-time payment rate, and average processing time per invoice. These metrics tell you whether your AP operation is actually getting faster or just feels like it is.

The case for automating your invoice payments

Invoice payments aren't glamorous, but they're one of the clearest signals of how well a finance operation actually runs. When the process works, vendors get paid on time, your team isn't buried in manual work, and cash flow forecasting stays predictable. When it doesn't, the consequences show up everywhere. Strained vendor relationships, missed early payment discounts, and hours spent tracking down invoices that should have been closed weeks ago.

The fix isn't complicated. Match the payment method to the transaction. Build clear approval ownership into your workflow. Automate the steps that don't require human judgment. Reconcile in real time instead of waiting until month-end to find out what went wrong. B2B bill payment automation doesn't replace good AP judgment. It removes the manual overhead that gets in the way of it. When your team isn't chasing approvals and re-entering data, they can focus on the decisions that actually move the business forward.

This story was produced by Brex and reviewed and distributed by Stacker.