How to switch business bank accounts (without breaking your finance stack)

Most finance leaders consider switching business bank accounts at some point. The triggers are usually the same: fees that outpace your revenue, integrations that stop working, a service tier you've outgrown. It's a growth move, not a chore. But it can feel like one.

Moving from one bank to another typically means rerouting everything connected to your account: payroll, vendor payments, accounting feeds, card statement debits. Being intentional protects you during the switch. It's what separates a clean migration from a messy one.

The short version: How to switch business bank accounts

- Open the new account: Have your EIN, formation documents, and ownership information ready. KYB approval ranges from same-day to several business days.

- Fund it: Move a starter deposit from the old account. Don't move everything yet.

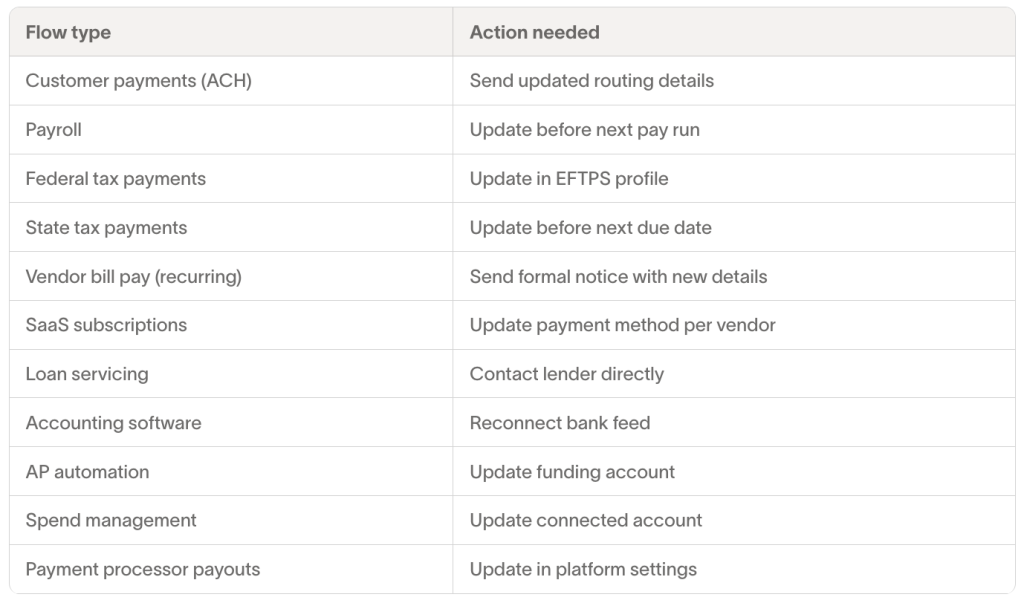

- Reroute inbound: Update routing details with customers on ACH auto-pay, payment processors, and anyone sending funds to you.

- Reroute outbound: Update payroll, tax authorities, vendors, and subscriptions with the new account details.

- Close the old account: Only after monitoring both accounts for at least 30 days and confirming every recurring flow has moved.

The rest of this guide by Ramp covers each step in detail, including what to inventory before you start, common failure points, and how to sequence the reroute without disrupting payroll or vendors.

When to switch business bank accounts

It’s time to switch business bank accounts when your current setup is actively costing you. That usually means fees that scale faster than your revenue, integrations that drop weekly, a service tier you've outgrown, or an inability to get a working line of credit.

Small businesses are increasingly looking beyond their primary bank for credit: Among applicants, the share seeking financing from online fintech lenders grew from 17% to 29% between 2020 and 2025, according to the Federal Reserve's 2026 Report on Employer Firms. When your bank can't underwrite your growth, the relationship starts to cost you even more than the fees do.

The triggers

- Fees outgrew you. Monthly minimums, transaction caps, and wire fees that add up to thousands per quarter.

- Integrations broke. Your bank's API doesn't connect cleanly to your accounting software, your spend platform, or your accounts payable tool.

- You can't get a line of credit. Your bank doesn't underwrite businesses like yours, or your relationship banker left and nothing replaced them.

- You outgrew the service tier. You're a Series A company on a sole-proprietor product, or a small business on an enterprise tier that costs more than the value it delivers.

How to time the switch

A switch is one moving part. Avoid layering it on top of another. Skip these windows:

- Mid-fundraise. Investors will ask for clean bank statements. A switch mid-process creates fragmented records.

- Mid-audit. Don't introduce a new account during a 10-K or seed-stage audit.

- Mid-payroll quarter-close. The payroll rails fund the people who keep the lights on. Don't reroute them in a quarter you're closing.

- During year-end. Closing the books across two banks is its own audit problem.

Before you switch: Inventory your money flows

Before you open the new account, write down everywhere your money currently moves. The audit is your single most useful pre-switch artifact. Once you have a complete picture of where money moves, the reroute is mechanical.

What's coming in

- Customer payments (ACH, wire, check, payment-processor payouts)

- Investor capital calls or tranche disbursements

- Loan disbursements

- Refunds and reimbursements from third parties

What's going out

- Payroll (the highest-stakes line item)

- Tax payments (federal, state, sales tax, payroll tax)

- Vendor bill pay (every recurring vendor)

- Subscriptions (SaaS, utilities, services)

- Card statement payments

- Loan servicing

What's connected

- Accounting software (the bank feed connection)

- Payment processors (Stripe, Square, and similar)

- Payroll provider

- AP automation tool

- Spend management platform

- Expense reimbursement system

That list is usually longer than teams expect. Write it down before you do anything else.

The 12-step bank-to-bank migration

A bank-to-bank switch is roughly 12 sequenced steps. Each one looks small in isolation. Most of the work is sequencing them right: Don't close the old account before recurring payments reroute, and don't move payroll before the new account is fully funded.

- Open the new business bank account. Apply through whichever channel the bank supports. Have your Employer Identification Number (EIN), formation documents, and beneficial-ownership info ready. Know Your Business (KYB) approval can take from same-day to several business days.

- Submit KYB documentation. Banks ask for entity documents, ID for owners over 25% ownership, and proof of address. Have these scanned and ready before you start.

- Fund the new account. Move a starter deposit over from the old account. Don't move everything yet: the goal is enough liquidity to test, not enough to strand you if something goes wrong.

- Update payroll routing. Push the new account info to your payroll provider. Most providers need several days' lead time before the next payroll run.

- Update tax payment routing. Federal, state, sales tax, and payroll tax all pull from a designated account. Update each one separately.

- Update vendor ACH details. For every recurring vendor, send a formal notice with the new routing and account number. Vendors keep your old information in their AP system until you proactively replace it.

- Update customer-facing ACH instructions. If you invoice with bank details, update your invoice templates and notify customers on auto-pay. Send the new wire instructions to anyone who pays you by wire.

- Reconnect accounting software. Bank feeds are tied to credentials, not just account numbers. Reconnect the new account inside your accounting platform. Run a test sync.

- Reconnect spend management and AP tools. Your card program and bill-pay tool need to know which account to fund. Update the connection inside each tool.

- Monitor both accounts. For at least 30 days, watch the old account for stray transactions: a vendor that wasn't updated, a customer who didn't switch, a recurring debit you forgot.

- Confirm all flows have moved. After a full month of running on the new account, look at the prior month's transaction list and confirm every recurring flow has switched.

- Close the old account. Only after step 11 is clean. Most banks require a written closure request and will return any remaining balance by check.

Common gotchas

These are the connections to double-check during a traditional bank-to-bank switch. They're predictable, so they're easy to plan around.

- Payroll routing drops. Your payroll provider holds onto old account numbers in its routing tables. Even after you update the primary, individual employees or tax payments can keep routing to the old account if the provider's batch hasn't refreshed. Verify on the first payroll run after the switch.

- Vendor payments to the old account number. Vendors keep your old bank info on file in their AP systems. Any vendor you don't proactively notify will keep pulling from the old account. Until you close it, those payments succeed silently and your reconciliation goes sideways.

- Accounting-software reconnection. Bank feed connections are tied to credentials. When you close the old account, the feed breaks. Reconnect the new feed during the overlap window so historical transactions keep flowing into your accounting system.

- Customer ACH details. Customers on auto-pay using your old account info will keep paying the wrong place. Send an update notice to every customer with the new routing and account numbers. Expect a few stragglers to need a manual reminder.

- Reconciliation during the overlap. With two accounts running for 30 days or more, your books need to track transactions across both. Make sure your accounting feed syncs both accounts during the overlap, and reconcile each against statements weekly. A stray vendor pull or customer payment hitting the old account is easy to miss if you're only watching the new one.

How to switch business bank accounts faster

Most of what makes a bank-to-bank switch take six weeks isn't the new account. It's reconnecting your card program, your AP tool, your accounting feed, your spend platform, and your expense reimbursement system to the new account.

When your operating account is part of a platform that already includes those tools, the connections come built in. There's nothing to rebuild during a switch. Fewer connections mean fewer places the switch can break, and fewer weeks spent on cleanup.

The switch is yours to control

The discipline that matters in switching business bank accounts isn't picking a new bank. It's keeping the money moving while you do. Write down every flow, sequence the reroute, and monitor both accounts before you close the old one. Whether you go bank-to-bank or move to an integrated platform, that discipline is what separates a clean switch from a messy one.

This story was produced by Ramp and reviewed and distributed by Stacker.