Startup cash management: How to keep idle cash earning

After raising a seed or Series A, most founders do the same thing: deposit the capital, set up payroll, and move on. The cash sits in a checking account earning close to nothing while the team focuses on growth.

That's an expensive habit.

For a startup with $2 million in reserves, the difference between 0% and 4% annual earnings is $80,000 per year — the equivalent of months of cloud infrastructure, a meaningful hire, or real runway extension.

This guide from Ramp covers how startups can build a simple cash management framework that keeps money working without disrupting operations.

What is startup cash management?

Cash management for startups is the process of managing liquidity so payroll and vendor payments are covered while excess cash earns short-term returns. It focuses on timing, segmentation, and automation to extend runway without increasing risk.

It's not about speculation or complex financial products. It's about making sure the gap between when money arrives and when it needs to leave is productive, not wasted.

The goal is simple: balance safety, liquidity, and returns to extend runway without adding operational risk.

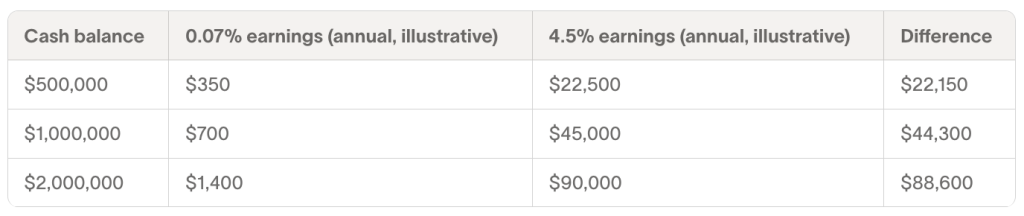

The cost of idle cash

Most of the cash sitting in traditional business checking accounts is barely working. The national average rate on interest checking is 0.07% (national average rate on interest checking accounts published by the FDIC as of Feb. 17, 2026), while government money market funds and short‑term U.S. Treasuries have, in early 2026, offered yields in the 4%–5% range, depending on market conditions. (Yield rates for government money market funds and U.S. Treasuries are variable and subject to change based on market conditions. Past performance is not indicative of future results.)

That spread compounds quickly.

The larger your balance and the longer it sits idle, the more material the opportunity cost becomes. Even $200,000 at 4% generates about $8,000 annually — enough to cover months of a software subscription.

The constraint isn’t opportunity. It’s liquidity. Payroll, SaaS renewals, and vendor invoices require immediate access. Locking funds into long-dated or illiquid vehicles introduces operational risk.

Strong vendor payment optimization solves that tension by keeping funds earning until they’re due, then deploying them precisely.

4 strategies for startup cash management

1. Negotiate longer payment terms

Extending vendor terms from Net 30 to Net 45 or Net 60 increases the window your cash stays invested.

If you pay $100,000 per month in vendor invoices:

- Net 30: Your cash leaves after 30 days

- Net 60: Your cash earns for 30 additional days before leaving your account

At a 4.5% annualized yield, that extra 30 days works out to roughly $370 per month, or more than $4,000 per year.

Best for: Established vendor relationships where you have negotiating leverage.

Watch for: Early-payment discounts like 2/10 Net 30 — paying within 10 days in exchange for a 2% discount. That discount works out to roughly a 36% annualized return, which almost always outweighs the earnings gained by waiting. Run the math before defaulting to longer terms.

2. Pay on the due date — not before

Many startups pay invoices immediately after approval. That's leaving money on the table.

Instead:

- Schedule payments to arrive on the due date

- Use same-day ACH or wires when timing matters

- Batch payments weekly to reduce administrative overhead

If terms are Net 30, pay on day 30 — not day 18.

One detail worth confirming: whether vendors require funds "received by" or "sent on" the due date. Small timing errors can compound across dozens of invoices.

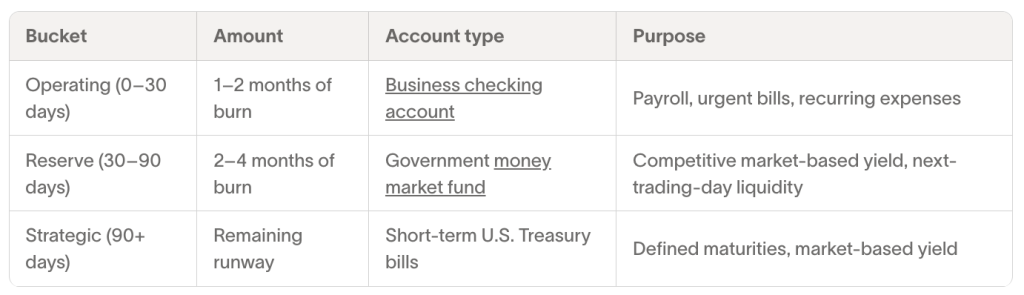

3. Segment cash by time horizon

The simplest way to put cash to work without disrupting operations is to stop treating all of it the same. Segment it into three buckets based on when you'll need it.

Keep enough in your operating bucket to cover at least two months of expenses without touching reserves. That buffer eliminates forced liquidations and rushed transfers.

If you're preprofit or at an earlier stage, lean conservative. Liquidity discipline matters more than incremental earnings.

4. Automate balance targets and transfers

Manual transfers create idle gaps. Automation closes them.

A simple framework:

- Set an operating balance target (e.g., $250,000)

- Excess funds move into a short-term investment vehicle

- When scheduled payments approach, funds are transferred back to cover them

Automation reduces timing errors and protects against overdrafts while keeping idle cash productive.

Best accounts for earning on business cash

The right structure depends on your burn rate, liquidity needs, and risk tolerance. Most startups use a mix of operating accounts and short-term investment vehicles to balance access and returns.

Business cash deposit accounts

Designed for day-to-day operations.

- Liquidity: Immediate access for payroll, vendor payments, and recurring expenses

- Insurance: Often eligible for FDIC insurance through partner banks, subject to applicable limits and program terms

- Earnings: Some providers offer cash rewards or earnings on eligible balances

These accounts are best for operating cash you’ll use within the next 30 days. The priority here is stability and instant access.

When evaluating options, compare earnings structure, insurance coverage limits, payment speed, and integration with your accounting system.

Government money market funds

Short-term investment funds that primarily hold U.S. government securities.

- Yield: Market-based and variable; changes daily with interest rates

- Liquidity: Typically, next-business-day access

- Insurance: Not FDIC-insured

These funds aim to maintain a stable $1.00 net asset value, but that value is not guaranteed and can fluctuate.

Best for reserve cash you may need within 30–90 days. They generally offer higher potential returns than many deposit accounts, with modest interest rate risk.

U.S. Treasury bills

Direct obligations of the U.S. government with fixed maturities.

- Yield: Market-based; depends on maturity and rate environment

- Liquidity: Common maturities range from four to 52 weeks; they can be sold prior to maturity in the secondary market

- Insurance: Not FDIC-insured; backed by the full faith and credit of the U.S. government

Best for cash you don't expect to need for several months. T-bills require more planning than money market funds, but offer predictable outcomes if held to maturity.

How integrated treasury simplifies startup cash management

When cash, cards, and bill payments live in separate systems, liquidity management becomes a spreadsheet exercise that's easy to deprioritize until a problem surfaces.

This story was produced by Ramp and reviewed and distributed by Stacker.