Auto insurance rates are stabilizing in 2025: Here’s how to save

After years of steep premium increases, 2025 is shaping up to be a turning point; rate hikes are finally slowing, and drivers are responding. Shopping and policy switching hit record levels in 2024 and remained elevated into 2025, per LexisNexis’ industry tracking, another sign consumers are actively seeking savings.

CheapInsurance.com discusses where rates are leveling off, what’s behind the shift, and how smart drivers can take advantage. Whether you're hunting for a better deal or trying to trim your current costs, knowing the trends and regional differences could help you save big this year.

Rate hikes cool in 2025, finally

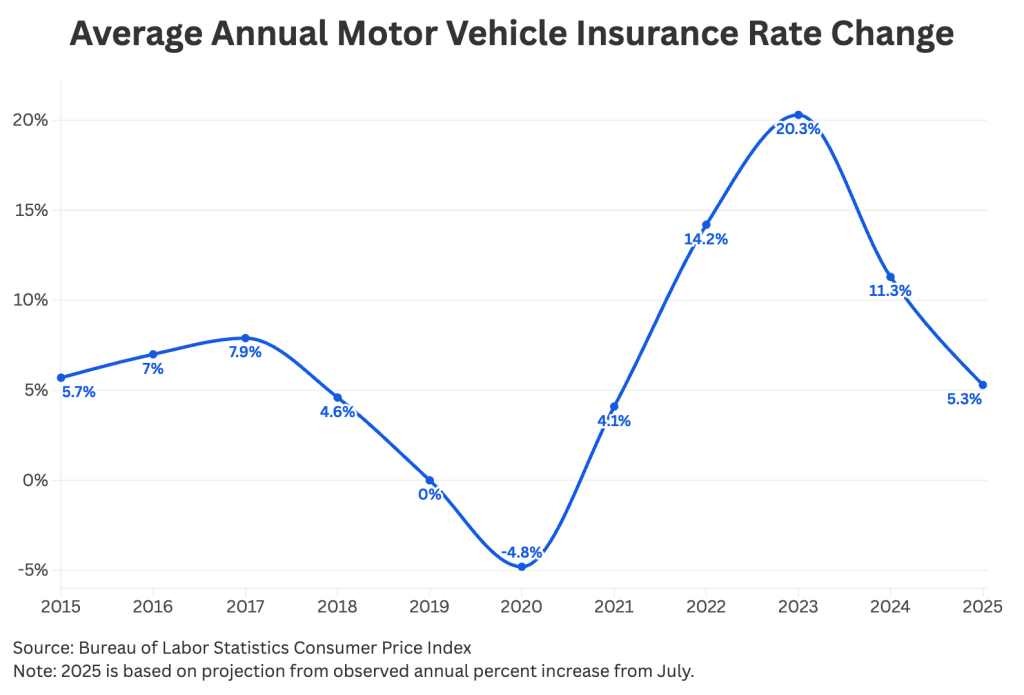

After years of steep increases, auto insurance premiums are finally starting to level off. Between 2022 and 2023, the Bureau of Labor Statistics reported that motor vehicle insurance costs jumped 20.3%, the biggest hike in over a decade. But from the end of July 2024 to the end of July 2025, the increase was 5.3%. That’s less than half of 2024’s overall 11.3% spike.

This analysis is based on Bureau of Labor Statistics data from major U.S. cities, and the slowdown reflects shifts in real-world consumer spending patterns.

Why rates are slowing: Factors behind the change

After years of back-to-back hikes, insurers are finally easing off the gas. With profitability improving, the focus has shifted from raising rates to keeping customers from jumping ship. Fewer claims, steadier repair costs, and smoother supply chains are also helping slow premium growth in 2025.

Accident rates have leveled out in many areas, and crash risk indicators have eased; the National Highway Traffic Safety Administration estimates traffic deaths declined in 2023 and continued to trend lower in early 2024. That said, proposed tariffs on auto parts and inflation could still disrupt trends later in the year. But for now, drivers are getting a break, especially those who take the time to shop around.

Americans are shopping around like never before

After years of rate hikes, drivers are fed up, and they’re taking action. LexisNexis industry tracking shows record‑high shopping and elevated switching into 2025, and digital channels continue to capture more of the customer journey, according to EY’s annual Global Insurance Outlook.

Regional rate reality: State-by-state trends

State costs vary widely due to laws, claim trends, litigation and weather. The National Association of Insurance Commissioners’ Auto Insurance Database shows clear state‑to‑state dispersion in average expenditures based on 2022, and 2025 rate filings suggest those relative differences persist.

Premium trends differ by state due to rate‑approval regimes, legal environment, traffic density and severe‑weather exposure; some states will see slower growth while others see continued upward pressure.

Repair‑cost drivers like labor rates, parts prices and Advanced Driver-Assistance Systems calibration are key reasons dense, higher‑value markets often see stronger upward pressure on premiums.

Why some states get hit harder or get a break

Insurance rates aren’t one-size-fits-all. State laws, accident trends, and local conditions all shape how much drivers pay.

No-fault states and storm-prone areas usually see higher premiums, especially where claims are severe. Scripps News reports that urban states packed with new, high-value cars also tend to face bigger increases.

On the flip side, places with milder weather, fewer accidents, and tighter insurance regulations often see slower rate growth — or even slight drops.

What this means for you, the consumer

With rate hikes slowing, 2025 is shaping up to be a solid time to shop around for car insurance. If you haven’t checked your policy in a while, now’s the moment to see if you can score a better deal.

Start with online tools and insurer apps. They’re faster and easier than ever, but features vary, so check a few. Also, reassess your coverage after big life changes. Bundling policies, raising your deductible, or using a telematics program could save you serious cash.

Smart shopping tips for 2025

- Set a reminder. Review your rates at every renewal.

- Shop around. Use apps and quote tools to compare.

- Find hidden discounts. Look for savings on bundling, low mileage, or safe driving.

The road ahead: Will relief last?

2025 may offer a breather from rising premiums, but it’s unlikely to last forever. Most experts expect rate increases to stay moderate, but surprises like new tariffs, extreme weather, or rising repair costs could send prices climbing again.

With shopping and switching still elevated, carriers are actively marketing competitive rates; consumers may see better deals, loyalty perks, or even sign-up bonuses. The best move now: Stay informed, compare regularly, and be ready to act if the market shifts again.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.