The coverage that pays for deer and other animal collisions

Hitting an animal with your vehicle is a stressful, frightening, and unfortunately, common event, particularly during the early morning and evening hours. From a high-speed collision with a deer to an unexpected encounter with a stray dog, the emotional impact is immediate. Once the dust settles, however, the practical question surfaces: Which auto insurance coverage will pay for the significant damage to my car?

For many drivers, this question is a major source of confusion, as the incident involves a ‘collision,’ yet the rules of insurance coverage are counterintuitive. Knowing the correct answer is imperative, as having the wrong coverage could leave you paying thousands of dollars out-of-pocket for repairs. This article by CheapInsurance.com aims to clarify this important insurance question, beginning with a look at the animals most frequently involved in these incidents.

Which Auto Insurance Coverage Pays for Hitting an Animal?

The single most important fact you need to know is this: Comprehensive coverage is the specific insurance category that pays for vehicle damage caused by hitting an animal, such as a deer, elk, or moose.

A collision with an animal is almost universally categorized by insurance companies as an “Other Than Collision” event. It is considered an unexpected event or an “Act of God” that is generally outside of the driver’s control.

If your insurance policy includes comprehensive coverage, your insurer will pay for the repairs to your vehicle, minus your deductible. If you only carry the state minimum liability coverage, which is required in most places, the cost of repairs from the animal strike will fall entirely on you.

Comprehensive vs. Collision: Understanding the Critical Difference

The terminology used by insurance companies often leads to the biggest misunderstanding. Why isn’t hitting an animal covered by collision coverage when it is, by definition, a collision?

The distinction lies in the insurance industry’s definition of the object you collide with.

Comprehensive Coverage (The ‘Other Than Collision’ Coverage)

What it Covers: Damage to your vehicle caused by events that are not a collision with another car or stationary object.

Examples of Covered Incidents:

- Animal strikes (deer, elk, coyote, etc.).

- Theft and vandalism.

- Fire, hail, flood, and other natural disasters.

- Falling objects (like a tree or large branch).

Comprehensive coverage protects you from random, unpredictable events that are largely outside of your driving control.

Collision Coverage

What it Covers: Damage to your vehicle resulting from an accident where your car collides with another vehicle or a stationary object.

Examples of Covered Incidents:

- Hitting another car.

- Hitting a fence, guardrail, mailbox, or building.

- Your car overturns or rolls over.

Collision coverage is designed for traditional traffic accidents where the driver’s actions (even if not at fault) directly resulted in a collision with an object with an owner or a fixed structure.

When you hit a deer, the insurance company views the animal as a random, unowned hazard, classifying the damage under the “other” category, which is comprehensive.

What Happens If I Avoid the Animal and Crash as a Result?

This is the major exception to the rule and a crucial point to understand, both for your safety and your insurance claim.

If a deer or other animal suddenly appears and you swerve to avoid it, thereby missing the animal but crashing into a guardrail, a tree, or another car, the rules change completely.

In this scenario:

- The Claim Becomes a Collision Claim: Because your vehicle collided with a stationary object (the tree or guardrail) or another vehicle, the resulting damage is paid for by your collision coverage, not your comprehensive coverage.

- The Insurance Implication: If you only have comprehensive coverage and no collision coverage, you will be responsible for the entire repair bill.

In the moment, the human instinct is to swerve, but insurance experts often advise drivers that if an impact is unavoidable and swerving carries a risk of a more severe crash (e.g., swerving into oncoming traffic), it is safer and financially wiser to brake firmly and hit the animal directly.

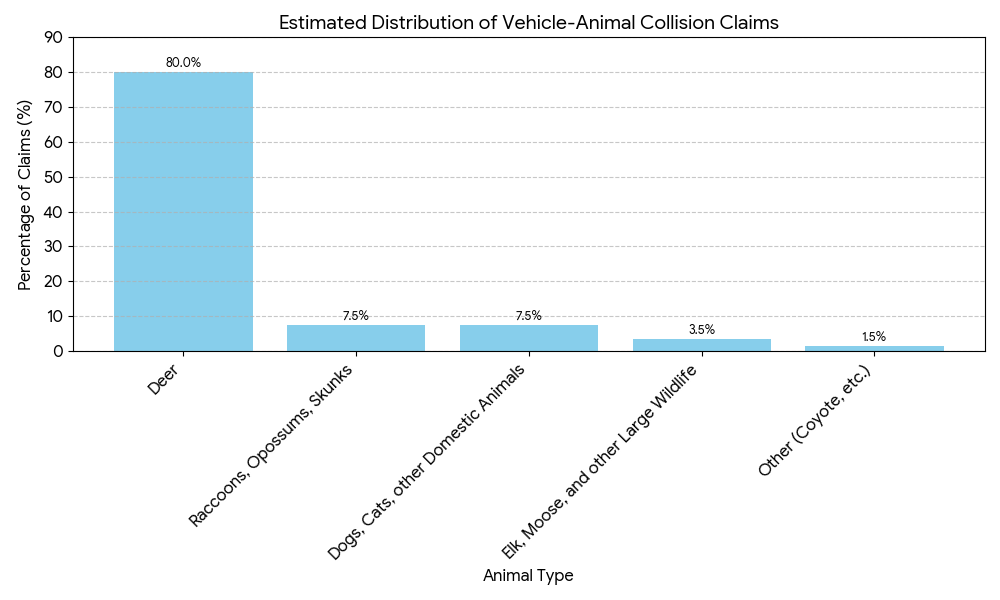

Which Animals Are Hit Most Often?

While any animal can dart into the path of your vehicle, some species are involved in collisions far more frequently than others, primarily due to their population density, habitat, and migratory patterns. Understanding which animals pose the highest risk can help drivers be more vigilant in certain areas and during specific times of the year.

Statistics consistently show that deer are, by an overwhelming margin, the animal most commonly involved in vehicle collisions across North America. This is followed by smaller mammals and, less frequently, larger animals like elk and moose.

To visualize the prevalence of these incidents, consider the breakdown of animal-vehicle collisions based on data and analyses on reported vehicle-animal collision claims and incidents published by the U.S. Federal Highway Administration (FHWA) and major Insurance Industry Research Organizations (e.g., IIHS-HLDI).

As the data illustrates, deer account for the vast majority of animal-related crashes, often exceeding 75% of all reported incidents. This underscores why drivers, particularly in rural and suburban areas, must remain especially attentive during dawn and dusk hours when deer are most active. Other commonly hit animals include raccoons, opossums, and skunks, though these typically cause less severe damage than a deer.

Is Hitting an Animal Considered an At-Fault Accident?

This is one of the biggest fears for drivers in this situation, as an at-fault accident can increase insurance rates for years.

The good news is that for most animal collisions, the answer is no, hitting an animal is generally not considered an at-fault accident.

- Why It’s Not Your Fault: Insurance companies recognize that a deer or elk darting into the road is an unpreventable, unpredictable event. Since there is no “at-fault” party for an animal, the claim is processed as a not-at-fault comprehensive claim.

- Effect on Rates: Because it is not an at-fault accident, filing a comprehensive claim for an animal strike typically has a much lower (or no) impact on your future rate rate compared to an at-fault collision claim. However, filing multiple comprehensive claims in a short period could still flag you as a higher risk.

The Exception: If you are found to be driving recklessly (speeding excessively in a clearly posted “deer crossing” zone) or if your crash resulted from swerving and hitting another car (a collision claim), you could be assigned fault, and your rates will likely increase.

Immediate Steps: What to Do Right After an Animal Collision

If the unfortunate happens, follow these steps to ensure your safety and a smooth insurance claim process.

1. Pull Over to Safety: Engage your hazard lights and move your vehicle to the side of the road immediately. Do not leave the scene of the accident.

2. Call the Police/Authorities: For large animals like deer, elk, or livestock, call the nonemergency police line or the highway patrol. They can file an official report, which is extremely helpful for your insurance claim, and they will know how to safely handle the animal.

3. Do NOT Approach the Animal: Injured animals, especially deer and elk, can be unpredictable, scared, and aggressive. For your safety, stay in your vehicle and wait for the police or animal control to arrive.

4. Document Everything Safely:

- Take photos of the damage to your vehicle.

- Photograph the scene, including skid marks (if any) and the location of the animal.

- Note the time, date, location (mile marker or nearest cross-street), and the type of animal.

- If you hit a pet, look for the owner and exchange information, following local laws regarding hitting a domestic animal.

5. Contact Your Insurance Company: Call your insurance agent or claims department as soon as you are safe. Provide them with the police report number and all of your documentation. The claim will then be initiated under your comprehensive coverage.

Frequently Asked Questions: Animal Collision Coverage

Is hitting a deer covered by comprehensive or collision insurance?

Vehicle damage from hitting a deer or other animal is typically covered by your comprehensive coverage, not collision coverage. Comprehensive insurance is designed for “other than collision” events, which are nonfault, unexpected incidents like theft, fire, or animal strikes.

Will my insurance rate go up if I file a comprehensive claim for hitting a deer?

Since deer accidents are generally classified as a no-fault comprehensive claim, your insurance premium may not increase, unlike an at-fault collision claim. However, premium changes depend on your state, insurer, and specific claim history.

Do I have to pay a deductible if I hit a deer?

Yes, when filing a claim under comprehensive coverage, you must pay your policy’s comprehensive deductible before the insurance covers the remaining costs of the repairs or the vehicle’s actual cash value if totaled. This deductible is the out-of-pocket amount you are responsible for.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.