Freight spot rates plunge on both coasts going into Thanksgiving, Black Friday and Cyber Monday amid weak imports

Last week, the global trade policy landscape saw a mix of slowing down and reactivation. The U.S. administration, while maintaining its broader tariff agenda, indicated a pause or delay in the imposition of large semiconductor import tariffs, reflecting sensitivity to supply-chain disruption, consumer pricing and the U.S.–China trade truce. Meanwhile, Canada and India moved to reset bilateral trade negotiations, signalling a thaw in previously strained relations and a renewed push to expand trade and investment. At the same time, high‐level engagement between the U.S. and China underscored that major trade policy shifts continue to be intertwined with geopolitics and technology-driven supply chain, Freight Right Global Logistics reports..

This Week’s Ocean, Air & Freight Markets

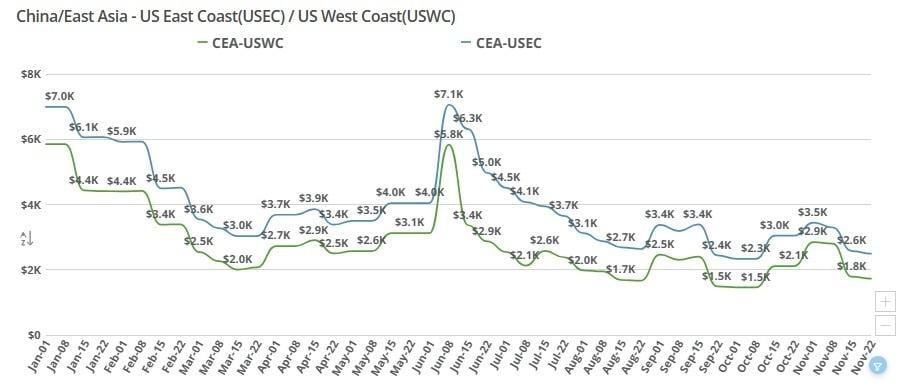

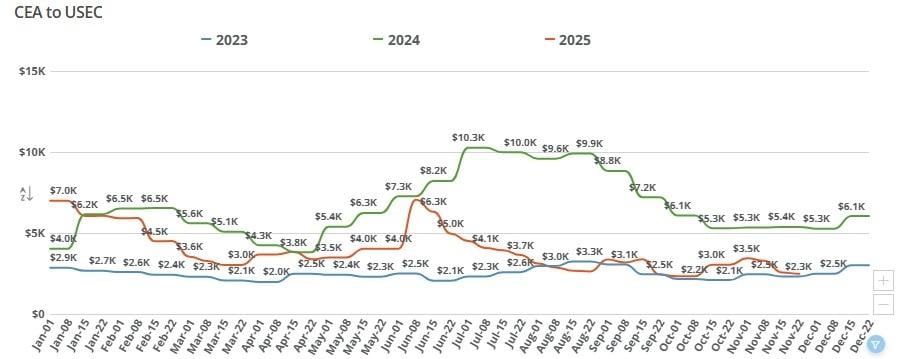

China-US Ocean Freight Market:

CEA to USWC: Spot rates continued their rapid decline this week, now falling to the $1,350-$1,500/FEU range, with some carrier-specific lows touching $1,350. This marks the fifth or sixth consecutive weekly drop in November, driven by slow demand and an extremely short holiday week in the U.S.

CEA to USEC: USEC rates also fell, now averaging ~$1,900/FEU, shrinking the typical spread between West and East Coast from ~$800–$900 to just $600–$700. Both lanes are effectively at or near their “rock-bottom” levels for the year.

Read more about the state of the ocean freight spot market with Freight Right’s TrueFreight Index.

This Week Explained:

- Demand Collapse During Thanksgiving Week: With Thanksgiving and the following Friday holiday, most shippers paused activity, creating one of the slowest weeks of the year. Carriers have little leverage to hold pricing when demand is essentially absent.

- Continuous Rate Reductions From Carriers: Carriers issued back-to-back reductions Monday and Tuesday, marking 5-6 cuts in November alone. Some carriers with traditionally lower pricing pushed offers down to $1,350/FEU, accelerating the downward trend.

- Rates Fell Faster and Earlier Than Expected: The market anticipated declines in late November, but not to this extreme, and not at month-end heading into December. Current levels are now near floor pricing, leaving little room for further decline without carriers taking losses.

- Muted Peak Season & Retail Inventory Overhang: BFCM-related imports largely occurred in September–October and at lower volumes than normal. Retailers still carry excess inventory and initiated aggressive discounting early, reducing inbound demand.

- Blank Sailings Not Tight Enough to Boost Rates: Carriers have eased blank sailings rather than increasing them, expecting Chinese New Year demand to improve. Space remains widely available, even 1–2 days before sailing, eliminating rate pressure.

Looking Ahead:

December is likely to stay at rock-bottom levels. Rates are expected to remain flat or soften slightly heading into December. With multiple public holidays and business closures, carriers have no incentive to introduce GRI/PSS mid-month.

A January rate increase is expected ahead of Chinese New Year. Carriers are almost certain to push through GRIs or PSS by early or mid-January to capitalize on pre-CNY cargo. Current levels are unsustainably low, and carriers will not want to move CNY volumes at $1,300–$1,900.

The Post-CNY slowdown will return. Once CNY passes (Feb. 18 window), carriers expect a deep lull for several months. Any rate strength in January-February will likely be short-lived.

No market surprises are expected: The near-term outlook is stable, predictable, and soft. Rates will close the year at or near current levels unless an unexpected shock emerges.

China-U.S. Air Freight Market:

CEA to USWC (China to U.S. West Coast): Rates continued to climb week-over-week as carriers push peak-season pricing ahead of December demand. Although the increases are moderate, capacity tightening and steady booking momentum are sustaining upward pressure.

CEA to USEC (China to U.S. East Coast): East Coast rates also moved higher this week, with all-water services seeing firmer pricing due to stronger demand, longer transit times, and continued blank-sailing strategies. The week-over-week uptick is in line with broader peak-season behavior.

This Week Explained:

- December peak season is fully underway, prompting carriers to raise FAK levels and tighten space allocation.

- Consistent increase in booking activity from China shippers preparing for year-end retail replenishment.

- Blank sailings and capacity management from carriers continue to restrict available space, pushing rates higher.

- Ongoing equipment imbalances, especially in key China export hubs, are adding upward pressure on short-term rates.

- Importers front-loading shipments due to uncertainty around January market conditions and potential schedule disruptions.

Looking Ahead:

Rate strength is expected to persist through the end of December, with carriers signaling additional GRIs if demand remains firm.

Capacity constraints will likely remain tight, particularly on USEC services, as vessels sail fuller approaching the holiday cutoff period.

A short-term stabilization or slight softening may emerge in early January once holiday-driven demand tapers, though much will depend on carrier discipline with blank sailings.

Shippers should plan for elevated rates and limited premium space availability for the remainder of the month and secure bookings as early as possible.

This story was produced by Freight Right Global Logistics and reviewed and distributed by Stacker.