Here's how the global economy impacts your car insurance rate

This story originally appeared on CheapInsurance.com and was produced and distributed in partnership with Stacker Studio.

Here's how the global economy impacts your car insurance rate

As of December 2024, car insurance rates had jumped 11.3% over the year prior, and tracking the reasons behind the spike in premiums isn't easy. Car insurance rates are affected by a global ripple—things like changes in U.S. trade relations or rising costs at local auto body shops may impact the cost of insurance. That may leave consumers wondering how these changes impact their bottom line.

CheapInsurance.com used data from the Bureau of Labor Statistics and the Census Bureau to explore the domestic and international factors that can directly affect car insurance rates.

Generally, American car insurers base rates on factors including driver's age, gender, driving history, location, type of vehicle, credit score, and even marital status. But supply chain issues, labor shortages and costs, and a spike in the prices of new cars all contribute to high premiums.

Insurance companies are raising rates partly because vehicle technology has made it more difficult to repair cars, sport utility vehicles, vans, and trucks. As the demand for repairs increases, so does the cost, which had already climbed after parts shortages and other global issues precipitated by the COVID-19 pandemic. For example, a global shortage of chips all but halted new vehicle production in early 2021—and made it harder for insurance companies to offer replacement vehicles after cars were totaled.

Increased vehicle prices are also partly to blame for higher premiums. Higher sticker prices tend to push consumers to fix cars they already own rather than buy new ones, ABC News reported. According to CNBC, heavier, more powerful vehicles that require more complex and expensive repairs, coupled with increased rates of speeding and crashes, could be pushing repair prices higher as well.

A mechanic shortage is also a factor. Many skilled technicians are retiring, while younger people are less inclined to make up the shortfall. And during the pandemic, fewer drivers on the road led to decreased maintenance needs. Now that people are back behind the wheel, cars need repairing, and mechanics are in short supply. A 2023 TechForce Foundation report suggested the U.S. shortfall for technicians could reach 471,000 from 2024 to 2028.

Even problems at critical supply chain choke points around the world are raising the cost of doing business. So, insurers are trying to compensate—and all that puts a dent in consumers' pocketbooks.

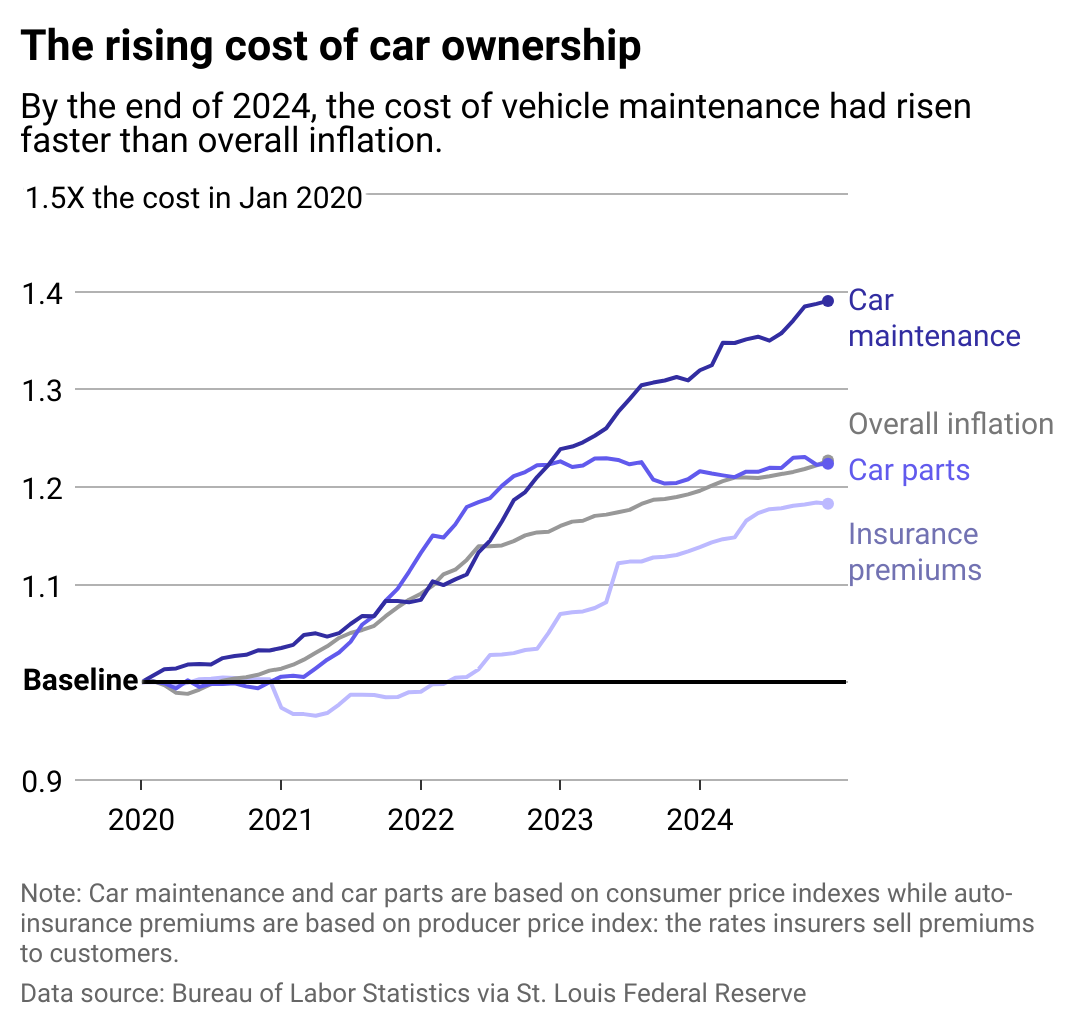

Cost of insurance and maintenance are increasing

BLS data shows that although maintenance and repair costs have climbed steadily since the 1960s, they've skyrocketed over the last few years. This is the "main reason" for higher insurance rates, The New York Times reported.

Other factors complicating the cost of repairs are more luxury models on the road and more severe crashes, which means insurers have to cover higher costs. When newer, safer vehicles and their cameras, radars, sensors, and other features are damaged, the repair work can quickly get complicated and, of course, more expensive.

In other words, as liabilities rise, so do premiums.

How global changes influence domestic auto insurance

There are some bright spots on the horizon for auto owners. Global shifts in manufacturing could help reduce car insurance rates in the United States, which are so high they're near a breaking point, the Times reported.

Since consumers absorb production costs, a shift from globalization to regionalization may bring down costs. With supply chain risks and bottlenecks still hindering the movement of goods through the Red Sea, Suez Canal, and Panama Canal, U.S. manufacturers who move production closer to home may decrease their overhead. Some prices—and yes, that may include rates—should go down.

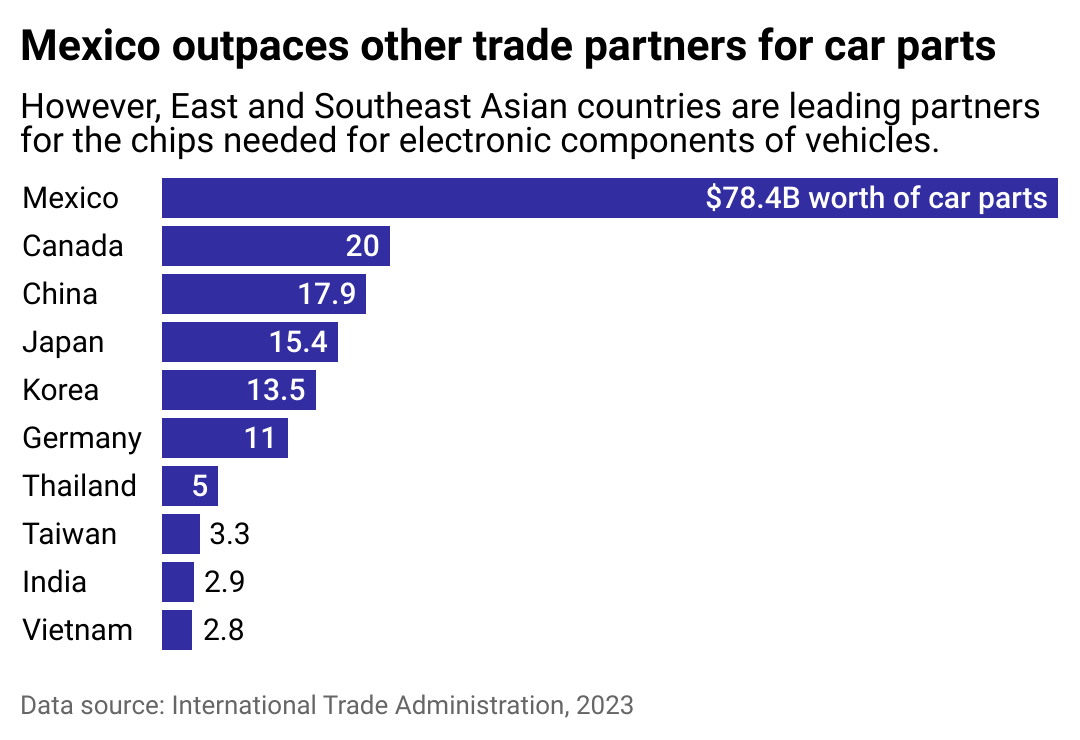

What's more, with new levels of transparency around fair pay, regulatory compliance, labor rights, and social and environmental issues, many companies are moving production closer to home, where regulation is less expensive. For example, car and car parts manufacturers that have long been in China and other Asian countries are investing heavily in Mexico, in part to reduce expenses associated with regulatory compliance, as Al Jazeera reported in early 2024. Political considerations, with caution about what information the U.S. discloses to China, also played a role.

This change, known as "nearshoring," in which companies get closer to their preferred markets, has an outsized impact on the automotive industry.

From 2019 to 2023, industrial park space in Mexico more than doubled, from 21.5 to 46 million square feet—and most of the $13 billion in industrial funding the country has secured over the last couple of years is to back auto or auto parts manufacturers, which have nearly a century of history in Mexico. The nation now far outpaces other U.S. trade partners for parts, in part due to increased supply and a more convenient, tighter supply chain.

But there is a fine line between reasonable increases and extra padding for profit margins. Between production shifts, frustrated consumers, and a 2024 win by Consumer Watchdog that challenged requests for inflated insurance rate increases among major providers, auto owners might want to monitor their rates closely. There are many things drivers can control, but geopolitics isn't one of them.

Story editing by Alizah Salario and Carren Jao. Additional editing by Kelly Glass and Elisa Huang. Copy editing by Kristen Wegrzyn.