Auto insurance shocker: Simple bumper dings now require expensive sensor recalibration

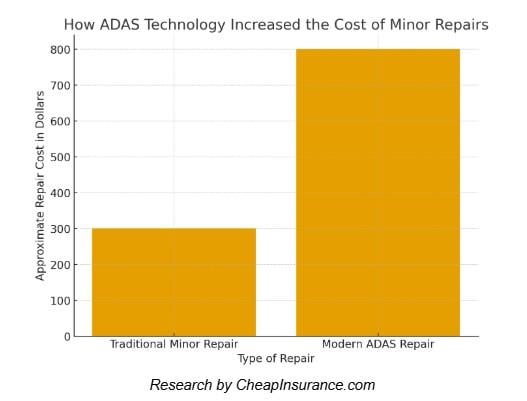

The automotive past is often recalled fondly. A fender bender was a nuisance, certainly, but the required repair was relatively predictable. The fix generally involved a new bumper cover, some paint work, and perhaps a headlight replacement. The car insurance payout or out-of-pocket expense amounted to a few hundred dollars, and the vehicle was quickly returned to service.

That financial predictability has become a relic of the past.

Today, even a minor bumper ding, the kind that barely scratches the paint, can trigger a massive, four-figure repair bill. This cost shock is due to a hidden expense lurking just behind the plastic: advanced driver assistance systems (ADAS).

This is no longer a simple body shop fix; it is a calibration crisis. Car insurance companies, body shops, and vehicle owners are grappling with the reality of mandatory sensor recalibration. Understanding why a vehicle demands a $500 computer adjustment after a $200 body repair is now central to surviving the modern automotive landscape and navigating rising vehicle insurance premiums. Cheap Insurance is focused on informing customers about the true cost of modern repairs.

The Brains Behind the Bumper: Welcome to the ADAS Era

The fundamental reason modern vehicle repairs have become so complex is due to a single factor: safety technology. This complexity directly affects the cost of repair and, consequently, car insurance rates.

A modern vehicle is not simply a mechanical conveyance; it is a rolling supercomputer. Advanced driver assistance systems (ADAS) features like adaptive cruise control (ACC), lane keep assist (LKA), automatic emergency braking (AEB), and blind spot monitoring (BSM) rely entirely on a sophisticated suite of sensors, cameras, and radar units strategically placed throughout the vehicle structure.

- Radar sensors: These are often located directly behind the front bumper cover or in the grille area. They emit radio waves to measure distance and speed, forming the critical backbone for ACC and AEB systems. Any damage to the mounting area of the bumper can misalign these sensors.

- Cameras: A forward-facing camera, typically mounted high on the windshield behind the rearview mirror, is crucial for LKA, traffic sign recognition, and the initial detection required for pedestrian detection. Windshield replacement, a common insurance claim, always requires recalibration of this camera.

- Ultrasonic sensors: These are small, circular sensors embedded in the front and rear bumpers that primarily aid in parking and low-speed object detection.

These sensors act as the vehicle’s eyes and ears. They constantly scan the road, communicating data in milliseconds to support the systems designed to maintain occupant safety. The integrity of this electronic network is now the primary concern for both repair facilities and car insurance adjusters following any collision.

Utah, for example, has enacted legislation that requires repair facilities to inform the consumer in writing if recalibration of the advanced driver assistance feature is required or will be performed. This trend toward mandatory disclosure and documentation is a direct response to the safety risks and high costs associated with these advanced systems.

The Physics of Precision: Why Calibration is Nonnegotiable

This is where the crisis is most evident. Advanced Driver Assistance Systems (ADAS) are designed with zero tolerance for error. The complexity of these systems forces car insurance providers to reconsider standard repair protocols and to mandate expensive diagnostic procedures.

When a vehicle’s radar unit is peering down the road, it is not merely looking ahead; it is looking at a specific, mathematically defined angle relative to the car’s axle and the road surface. This angle is often measured in fractions of a degree.

The Ding and the Disruption

Even a minor collision can have catastrophic effects on this precision.

- The impact: A light tap that only pushes the bumper cover slightly inward or twists a mounting bracket can move the radar sensor by a mere millimeter.

- The deviation: A 1-millimeter shift is enough to throw off that crucial angle. Over a 100-foot distance, that tiny shift means the radar is now looking several feet away from the center of the travel lane.

- The disaster: If the sensor’s gaze is misaligned, the system can misinterpret the environment. Adaptive cruise control might track a vehicle in an adjacent lane. More critically, automatic emergency braking might fail to detect a pedestrian or, conversely, apply the brakes for an object that poses no threat.

A simple replacement of the new bumper cover is never enough. Any replacement of an ADAS-equipped part, including a bumper, windshield, grille, or suspension components, mandates a complete recalibration.

The Car Insurance Response by State

The necessity of this complex recalibration is driving legislative action and insurance policy changes across the country.

- In Florida, recent legislation was enacted to prohibit a policyholder from entering into an assignment agreement for post-loss benefits related to glass repair or ADAS recalibration. This aims to limit repair shop incentives and ensure insurance companies retain control over the complex, costly ADAS claim process.

- California is experiencing significant variance in how insurance policies cover ADAS calibration following repairs. While comprehensive policies generally cover calibration after an accident, the burden often remains on the repair shop to ensure the procedure is completed and documented to prevent claims denial by the insurer.

- In Arizona, the state senate has considered legislation requiring auto glass repair companies to inform customers about calibration requirements and provide an itemized description of the work. This focus on transparency is directly linked to the high cost of ADAS recalibration, forcing insurance companies to clearly outline their coverage for these technical repairs.

The legal and financial pressure from these state trends ensures that car insurance companies treat ADAS recalibration as a mandatory safety requirement, not a negotiable option.

Static vs. Dynamic: The High-Tech Shop Visit

Recalibration is not a quick software update; it is a specialized, time-consuming procedure that requires expensive tools and highly trained technicians. This specialization is a key reason why auto insurance claims for minor collisions now feature unexpectedly high labor costs. There are two primary types of calibration processes that repair facilities must employ.

1. Static Calibration

This is the most precise and least forgiving type. The vehicle must be stationary (static) in a perfectly level, climate-controlled shop environment.

- The setup: Technicians use specialized tools, often large geometric targets and high definition alignment mats, which are placed at precise distances and angles from the vehicle.

- The procedure: The vehicle’s computer then communicates with the sensors, using these real-world targets to confirm that the sensors are viewing precisely what they should be viewing. This process requires the vehicle to be perfectly centered and measured relative to its axle centerline, a highly technical setup.

2. Dynamic Calibration

This process requires a road test to complete the sensor adjustment.

- The procedure: The technician drives the vehicle on the road, often for 20 to 60 minutes, at specific speeds while monitoring the computer. The vehicle’s ADAS systems use natural landmarks like lane markers, traffic signs, and other vehicles to self-adjust and learn their correct orientation.

- The requirement: This still usually requires initial setup in the shop and may have strict environmental requirements, such as the absence of rain and clear, good lane markings.

The Bottom Line on Cost

These specialized procedures require original equipment manufacturer (OEM) diagnostic tools. These are the same tools used by dealerships, which cost thousands of dollars. The required labor rate is higher because the repair stakes are higher; this is not simply a body repair, it is a life saving system check. Car insurance adjusters must now account for this increased cost. A collision repair facility must charge for the necessary expertise and equipment, resulting in a scenario where a simple bumper job suddenly includes a $300 to $800 calibration fee, causing the overall claim cost to skyrocket for the car insurance provider.

The Insurance and Liability Tightrope

The stakes of the calibration crisis extend far beyond the immediate repair expense; they reach deeply into the complex world of car insurance and legal liability. The risk of an accident where the automatic emergency braking (AEB) system fails to stop a vehicle is significant.

If a post accident investigation reveals that the radar sensor was misaligned due to a previous, uncalibrated bumper repair, the question of fault becomes multifaceted:

- Does the liability fall on the vehicle owner for driving a vehicle with compromised safety systems?

- Is the repair shop responsible for failing to perform the required calibration according to Original Equipment Manufacturer (OEM) standards?

- What is the responsibility of the car insurance company for initially denying or underpaying for the specialized calibration procedure?

Car insurance providers are increasingly aware of this compounding risk. Many major carriers now mandate ADAS calibration as a nonnegotiable part of any covered repair involving sensor-equipped components. Failure to calibrate properly provides a potential defense for the insurer to argue that the vehicle was improperly repaired, an action that could jeopardize the coverage related to a subsequent claim or accident. Denied claims related to uncalibrated systems are becoming more frequent, leading to disputes and out-of-pocket costs for the owner.

For the repair facility, the liability is immense. An improperly calibrated ADAS system could expose the facility to direct legal action in a negligence claim should an accident occur due to system failure. This necessity to cover their own liability is a primary reason repair shops are insistent, and justifiably so, on performing and charging for the expensive, specialized calibration process. The financial integrity of the vehicle insurance claim process hinges on this step being completed and thoroughly documented.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.