Driving less? Usage‑based insurance explained and how to save

CheapInsurance.com explores how driving fewer miles or changing driving habits can influence an insurance policy’s cost. If vehicle usage has dropped due to remote work, car sharing, or lifestyle changes, understanding how car insurance companies offer usage-based insurance (UBI) is key. This information helps drivers evaluate whether they are paying too much or could benefit from a different approach to auto insurance.

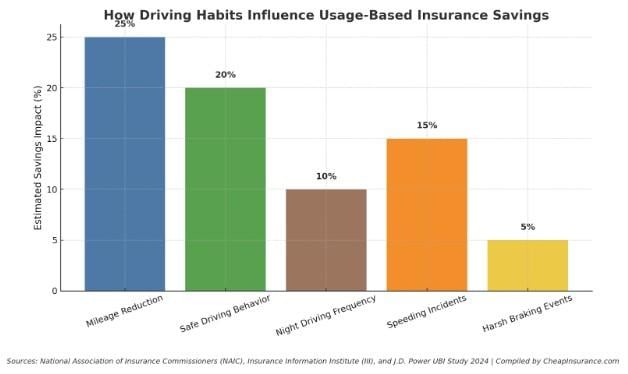

Usage‑Based Insurance and How It Works

Usage-based insurance, often called UBI or telematics insurance, leverages driving data to adjust premiums based on how, when, and how much a vehicle is driven. The National Association of Insurance Commissioners (NAIC) explains that UBI uses devices or smartphone apps to monitor key metrics such as miles driven, time of day, braking behavior, and acceleration.

Here are the key elements of how UBI operates.

- Monitoring Mileage: Driving fewer miles generally equates to a lower risk of filing a claim.

- Behavior Tracking: Metrics like hard braking, rapid acceleration, late-night driving, and high-speed driving often indicate increased risk and may affect the premium.

- Data Consent and Technology: Drivers must typically opt in to participate; the specifics of data collection vary by insurer and the technology used.

When Driving Less Makes a Real Difference in Premiums

If a driver’s patterns have shifted, there may be a chance to benefit from updated usage-based insurance (UBI). Consider these common scenarios.

- A driver’s job moves to remote work, or they now commute less frequently.

- The vehicle is used only for errands or leisure rather than daily commuting.

- A person switches to car sharing, ride hailing, or alternative transport for part of the year.

- Driving occurs primarily in low-risk environments (e.g., fewer miles, less night driving, no heavy traffic routes).

Because UBI programs more accurately align cost with actual risk, reducing vehicle usage and adopting safer driving habits can lead to meaningful premium savings.

What to Ask Your Insurer Before Opting Into a UBI Program

Before enrollment in a usage-based program, clarity on specific details is essential. Important questions to ask include:

- Data Collection: What exact data will be collected, such as mileage, speed, time of day, and location?

- Premium Adjustment: How will the premium be adjusted? Will the rate only decrease, or is there a possibility it could increase?

- Program Status: Is the program a mandatory requirement or an optional feature for the policy?

- Malfunction Protocol: What happens if the device or application malfunctions, or if the driver disconnects the tracking?

- Data Security: How is the driver’s privacy protected, and what are the specific data handling protocols?

- Thresholds and Guarantees: Is there a minimum driving threshold or a guaranteed discount clause associated with participation?

Potential Advantages and Trade‑Offs of Usage‑Based Insurance

Advantages:

- Drivers with genuinely lower mileage or lower-risk driving behavior may pay significantly less than standard pricing.

- The system helps match the insurance premium more closely to actual usage and individual risk rather than broad assumptions.

- It may encourage safer driving habits and result in fewer claims overall, benefiting both drivers and insurers.

Tradeoffs:

- Some drivers may see minimal benefit if their usage patterns do not change significantly.

- The constant collection of driving data raises privacy concerns, requiring comfort with sharing behavioral information.

- If driving frequency or distance increases unexpectedly (for example, due to a longer commute or a road trip), the rate may increase.

- Not all insurers or states treat usage-based insurance data equivalently, as regulatory frameworks differ.

How to Use Your Low‑Mileage Lifestyle to Your Advantage

For drivers whose annual mileage has decreased and is likely to remain low, specific actions can be taken to adjust car insurance.

- Review Current Policy: Examine whether the existing policy includes a “low mileage” discount or a usage-based insurance program.

- Compare Driving History: Compare the actual annual miles driven to the mileage estimated when the policy was quoted; a significant reduction may justify requesting a new automobile insurance quote.

- Inquire About Features: Ask the insurer how turning off nonessential features (for instance, telematics tracking for short-term drivers) or switching to a usage-based option would affect the car insurance premium.

- Check Renewal Terms: Review the policy carefully upon renewal and ask for a usage-based evaluation if such an option is available.

- Maintain Safe Habits: Keep driving habits aligned with program incentives, which typically means avoiding late-night driving, reducing high-speed use, and braking gently.

Regulatory and State‑Level Considerations for Usage‑Based Pricing

Insurance regulation occurs at the state level, meaning eligibility and program terms for usage-based insurance may vary significantly by location. For instance, the Washington State insurance regulator describes usage-based insurance as a method where an insurer uses technology to monitor driving behavior to determine premium assessment. Legislative action continues to emerge; a proposed bill in New York (S7129) would establish a consent-based framework for insurer use of telematics. Reviewing a state insurance department’s guidance is essential before committing to any program.

When driving activity has dropped substantially, seeking smarter ways to align insurance cost with actual usage, a usage-based insurance program may offer meaningful savings and reflect a lower risk profile. Informed drivers review all components of coverage, including how and how much driving occurs, to ensure the car insurance policy fits both lifestyle and budget.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.